Answered step by step

Verified Expert Solution

Question

1 Approved Answer

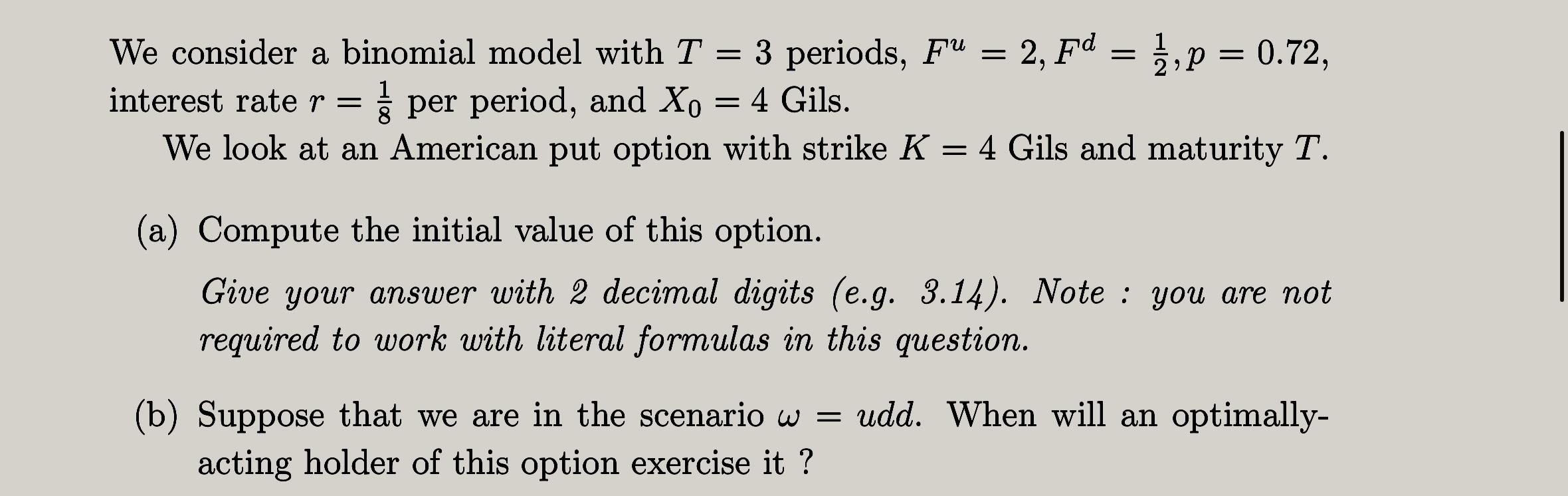

Fu We consider a binomial model with T = 3 periods, F = 2, Fd = , p = 0.72, per period, and Xo

Fu We consider a binomial model with T = 3 periods, F = 2, Fd = , p = 0.72, per period, and Xo = 4 Gils. interest rate r = We look at an American put option with strike K = 4 Gils and maturity T. (a) Compute the initial value of this option. Give your answer with 2 decimal digits (e.g. 3.14). Note: you are not required to work with literal formulas in this question. (b) Suppose that we are in the scenario w = udd. When will an optimally- acting holder of this option exercise it?

Step by Step Solution

★★★★★

3.46 Rating (156 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516