Answered step by step

Verified Expert Solution

Question

1 Approved Answer

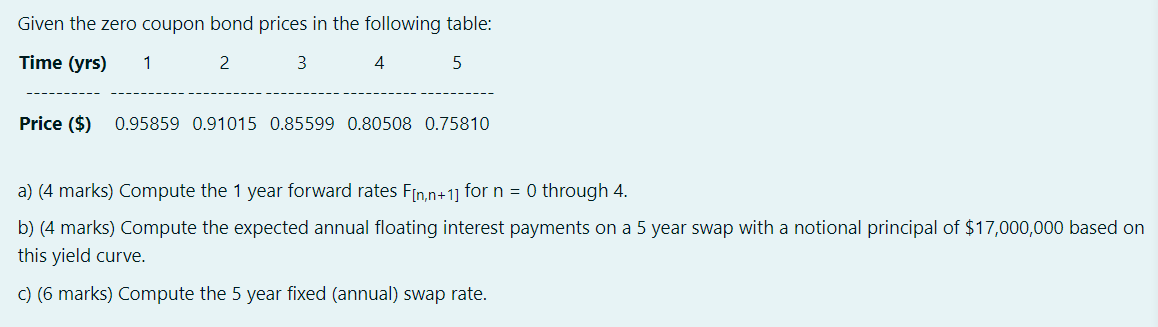

full answer plz 1 Given the zero coupon bond prices in the following table: Time (yrs) 1 2 3 4 5 Price ($) 0.95859 0.91015

full answer plz

full answer plz

1

Given the zero coupon bond prices in the following table: Time (yrs) 1 2 3 4 5 Price ($) 0.95859 0.91015 0.85599 0.80508 0.75810 a) (4 marks) Compute the 1 year forward rates F[n,n+1] for n = 0 through 4. b) (4 marks) Compute the expected annual floating interest payments on a 5 year swap with a notional principal of $17,000,000 based on this yield curve. c) (6 marks) Compute the 5 year fixed (annual) swap rate Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management

Authors: Geoffrey Knott

4th Edition

1403903824, 9781403903822