Answered step by step

Verified Expert Solution

Question

1 Approved Answer

GARCH model is ( sigma_t)^2 = omega +alpha* (u_(t-1)^2 +beta*(sigma_(t-1))^2 omega=0.00000005 not 0.00005 A risk manager estimates daily variance of using a GARCH model on

GARCH model is ( sigma_t)^2 = omega +alpha* (u_(t-1)^2 +beta*(sigma_(t-1))^2

omega=0.00000005 not 0.00005

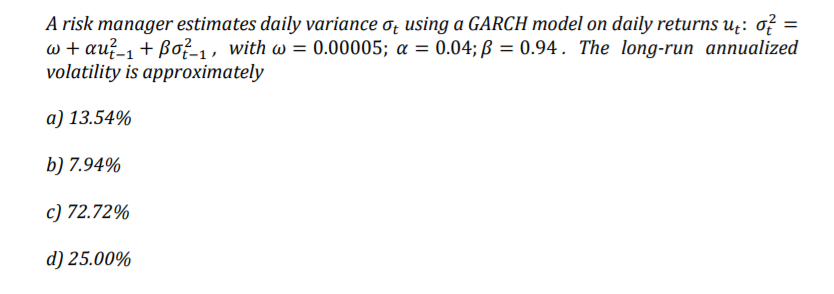

A risk manager estimates daily variance of using a GARCH model on daily returns ut: 07 = w + au{-1 + Box-1, with w = 0.00005; a = 0.04; = 0.94. The long-run annualized volatility is approximately a) 13.54% b) 7.94% c) 72.72% d) 25.00%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments

Authors: Zvi Bodie, Alex Kane, Alan J. Marcus

9th Edition

73530700, 978-0073530703