Question

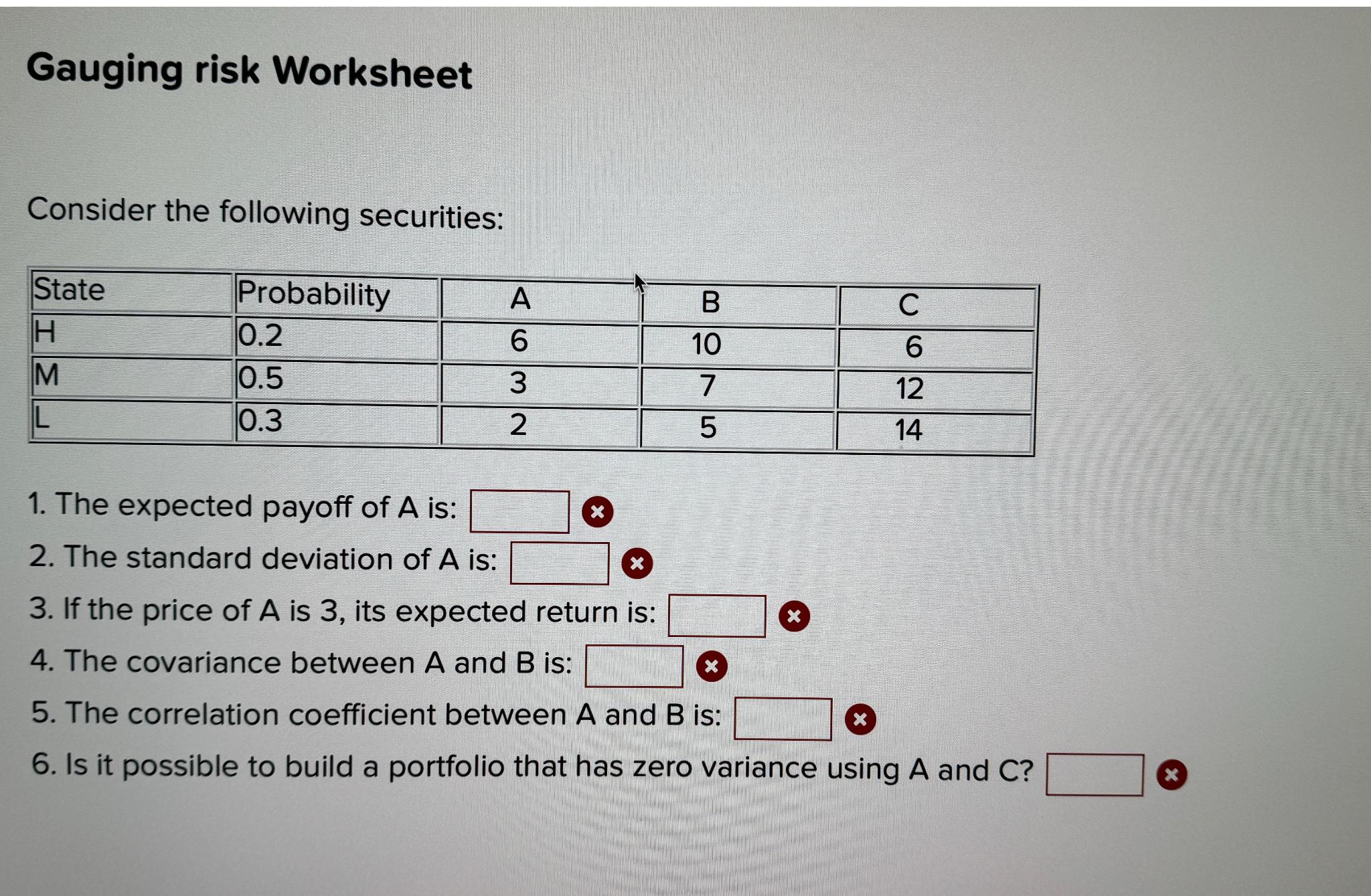

Gauging risk Worksheet Consider the following securities: table[[State,Probability,A,B,C],[ H ,0.2,6,10,6],[ M ,0.5,3,7,12],[ L ,0.3,2,5,14]] The expected payoff of A is: The standard deviation of A

Gauging risk Worksheet\ Consider the following securities:\ \\\\table[[State,Probability,A,B,C],[

H,0.2,6,10,6],[

M,0.5,3,7,12],[

L,0.3,2,5,14]]\ The expected payoff of

Ais:\ The standard deviation of

Ais:\ If the price of

Ais 3 , its expected return is:\ The covariance between

Aand

Bis:\ The correlation coefficient between

Aand

Bis:\ Is it possible to build a portfolio that has zero variance using

Aand

C?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Data Management Databases And Organizations

Authors: Richard T. Watson

6th Edition

1943153035, 978-1943153039