Question

General Journal: Accounts payable Accounts receivable Accumulated depreciation - Store equipment Advertising expense Cash Common stock Cost of goods sold Depreciation expense - Store equipment

General Journal:

Accounts payable

Accounts receivable

Accumulated depreciation - Store equipment

Advertising expense

Cash

Common stock

Cost of goods sold

Depreciation expense - Store equipment

Dividends

Insurance expense

Merchandise inventory

Prepaid insurance

Rent expense

Retained earnings

Salaries expense

Sales

Sales discounts

Sales returns and allowances

Store equipment

Store supplies

Store supplies expense

Accounts payable

Accumulated depreciation

Advertising expense

Cash

Cost of goods sold

Depreciation expense - Store equpment

Insurance expense

Merchandise inventory

Office salaries expense

Prepaid insurance

Rent expense - Office space

Rent expense - Selling space

Sales

Sales salaries expense

Store supplies expense

Accounts payable

Accumulated depreciation - Store equipment

Cash

Common stock

Cost of goods sold

Dividends

General and administrative expenses

Merchandise inventory

Net sales

Prepaid insurance

Retained earnings

Selling expenses

Store equipment

Store supplies

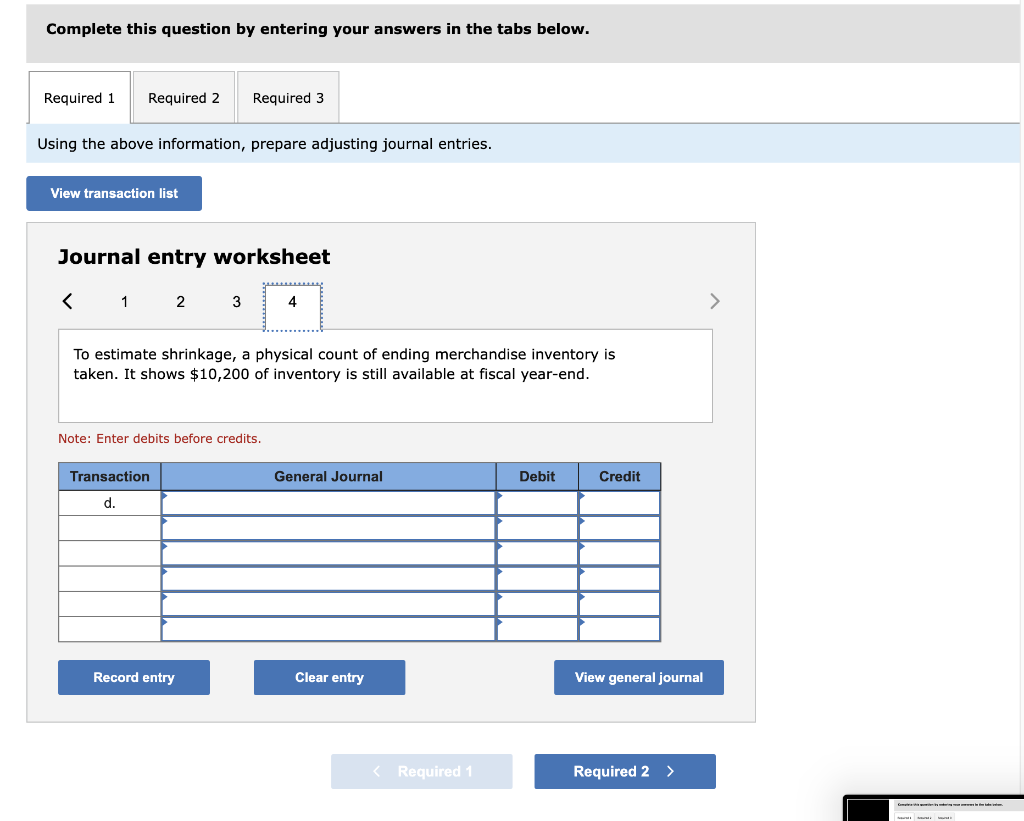

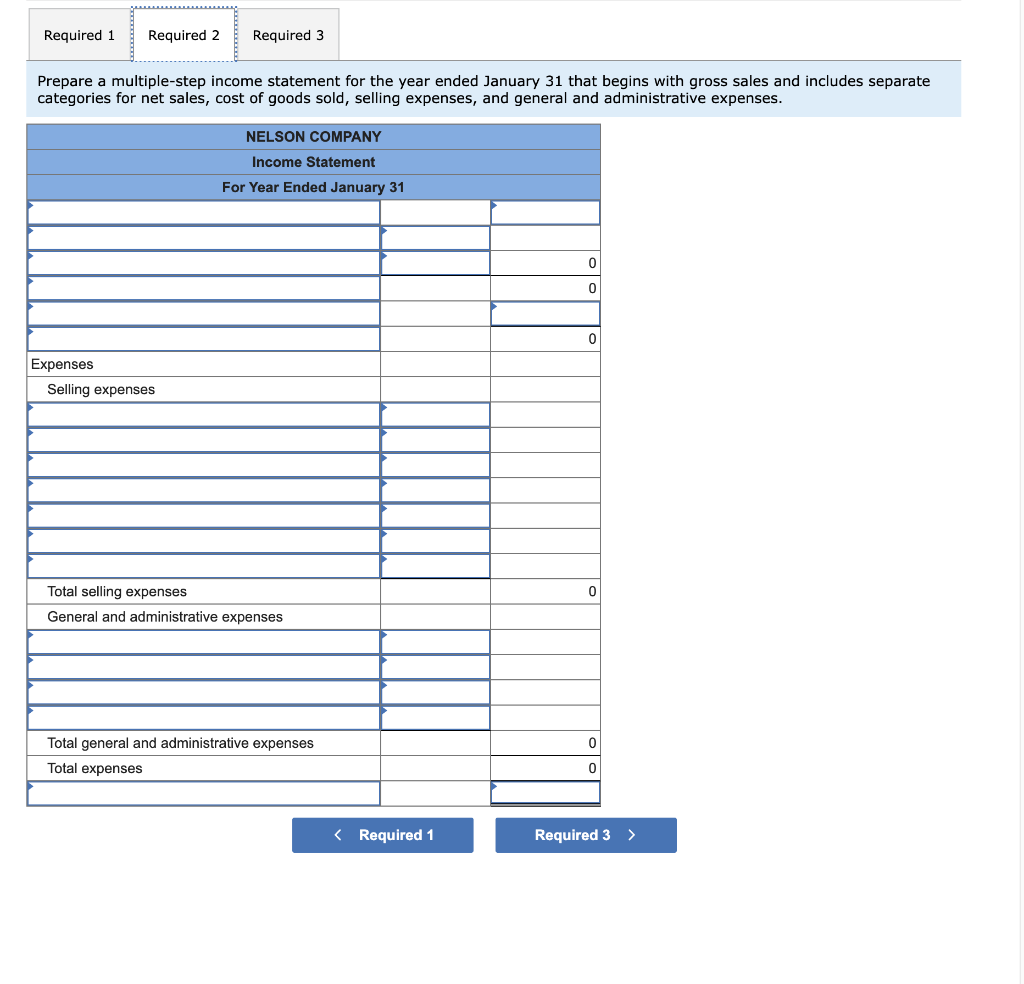

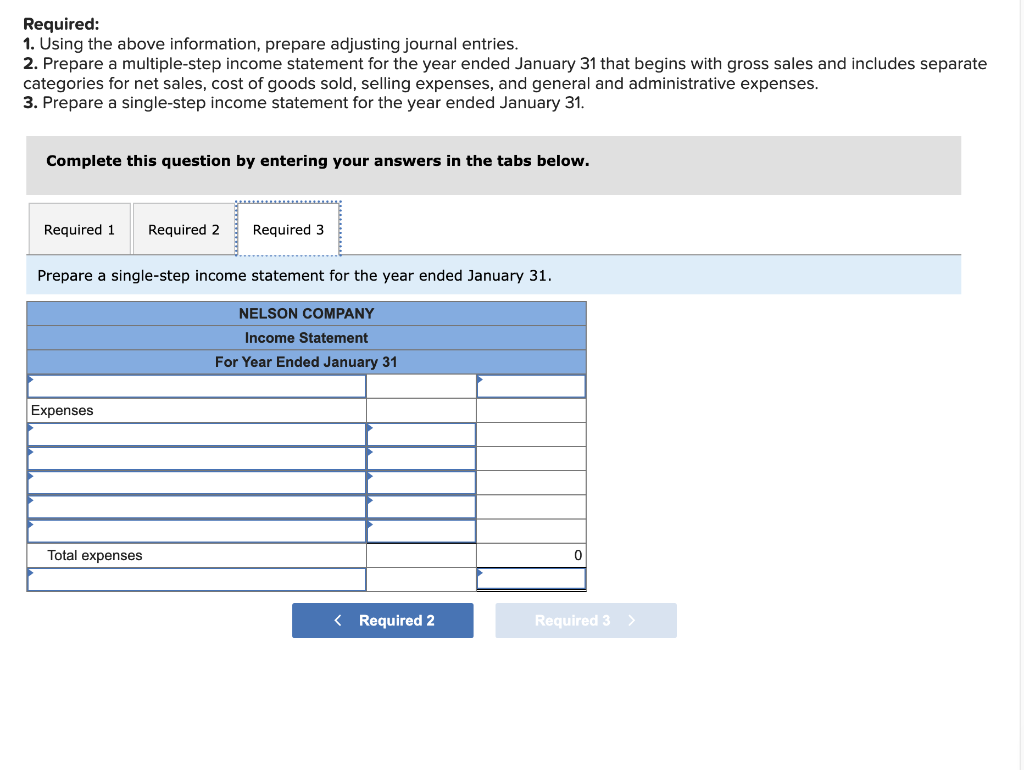

Required information [The following information applies to the questions displayed below.] The following unadjusted trial balance is prepared at fiscal year-end for Nelson Company. Nelson Company uses a perpetual inventory system. It categorizes the following accounts as selling expenses: Depreciation Expense-Store Equipment, Sales Salaries Expense, Rent Expense-Selling Space, Store Supplies Expense, and Advertising Expense. It categorizes the remaining expenses as general and administrative. Additional Information: a. Store supplies still available at fiscal year-end amount to $1,950. b. Expired insurance, an administrative expense, is $1,600 for the fiscal year. c. Depreciation expense on store equipment, a selling expense, is $1,575 for the fiscal year. d. To estimate shrinkage, a physical count of ending merchandise inventory is taken. It shows $10,200 of inventory is still available at fiscal year-end. Required: . Using the above information, prepare adjusting journal entries. . Prepare a multiple-step income statement for the year ended January 31 that begins with gross sales and includes separate ategories for net sales, cost of goods sold, selling expenses, and general and administrative expenses. Prepare a single-step income statement for the year ended January 31. Complete this question by entering your answers in the tabs below. Using the above information, prepare adjusting journal entries. Journal entry worksheet Store supplies still available at fiscal year-end amount to $1,950. Note: Enter debits before credits. Complete this question by entering your answers in the tabs below. Using the above information, prepare adjusting journal entries. Journal entry worksheet Expired insurance, an administrative expense, is $1,600 for the fiscal year. Note: Enter debits before credits. Complete this question by entering your answers in the tabs below. Using the above information, prepare adjusting journal entries. Journal entry worksheet Depreciation expense on store equipment, a selling expense, is $1,575 for the fiscal year. Note: Enter debits before credits. Complete this question by entering your answers in the tabs below. Using the above information, prepare adjusting journal entries. Journal entry worksheet To estimate shrinkage, a physical count of ending merchandise inventory is taken. It shows $10,200 of inventory is still available at fiscal year-end. Note: Enter debits before credits. Prepare a multiple-step income statement for the year ended January 31 that begins with gross sales and includes separate categories for net sales, cost of goods sold, selling expenses, and general and administrative expenses. Required: 1. Using the above information, prepare adjusting journal entries. 2. Prepare a multiple-step income statement for the year ended January 31 that begins with gross sales and includes separate categories for net sales, cost of goods sold, selling expenses, and general and administrative expenses. 3. Prepare a single-step income statement for the year ended January 31. Complete this question by entering your answers in the tabs below. Prepare a single-step income statement for the year ended January 31Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

From Zero To Zen Secret Keys To Nurturing Your Numbers And Finding Financial Flow

Authors: Liz Lajoie

1st Edition

1683507045, 978-1683507048