Answered step by step

Verified Expert Solution

Question

1 Approved Answer

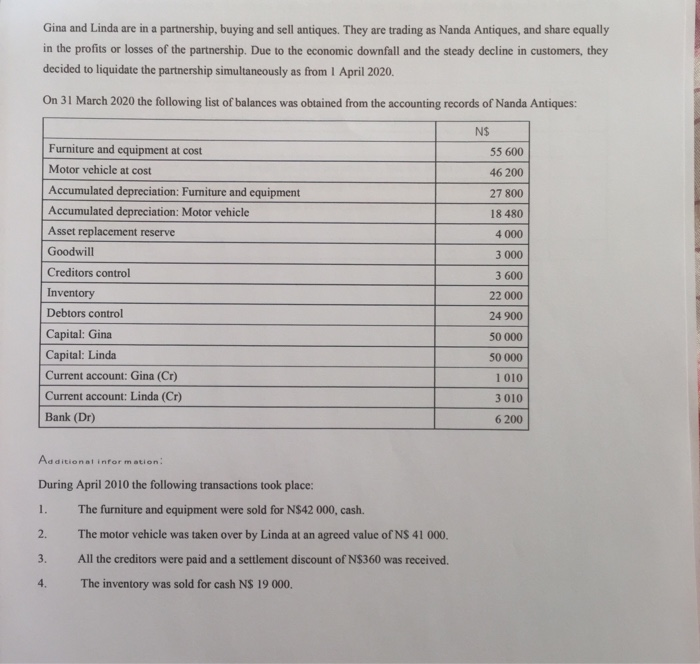

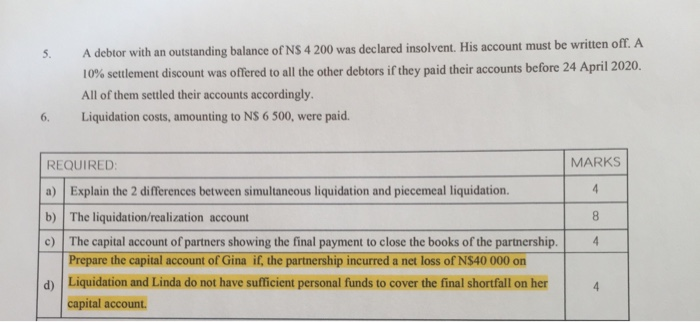

Gina and Linda are in a partnership, buying and sell antiques. They are trading as Nanda Antiques, and share equally in the profits or losses

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Corporate Ethics Audit As A New Tool For Management By Values Case Betapharm Arzneimittel GmbH Augsburg

Authors: Teresa Beste

1st Edition

3639000234, 978-3639000238