Answered step by step

Verified Expert Solution

Question

1 Approved Answer

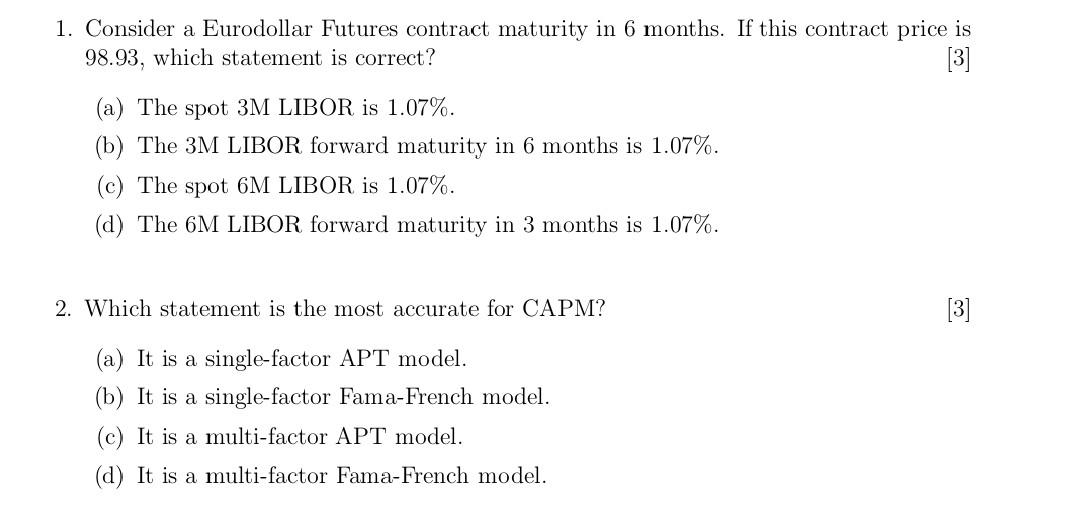

Give correct answers in 25 mins i will thumnb up 1. Consider a Eurodollar Futures contract maturity in 6 months. If this contract price is

Give correct answers in 25 mins i will thumnb up

1. Consider a Eurodollar Futures contract maturity in 6 months. If this contract price is 98.93, which statement is correct? [3] (a) The spot 3M LIBOR is 1.07%. (b) The 3M LIBOR forward maturity in 6 months is 1.07%. (c) The spot 6M LIBOR is 1.07%. (d) The 6M LIBOR forward maturity in 3 months is 1.07%. 2. Which statement is the most accurate for CAPM? [3] (a) It is a single-factor APT model. (b) It is a single-factor Fama-French model. (c) It is a multi-factor APT model. (d) It is a multi-factor Fama-French modelStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Issues In Behavioral Finance

Authors: Simon Grima

1st Edition

1787698823, 978-1787698826