give me answer in 2 hours for any problem you can comment me.... First of all clear this point only Why do some older people

give me answer in 2 hours for any problem you can comment me....

First of all clear this point only

Why do some older people live in poverty today in spite of the drop in poverty rates? What are the implications of shifting from 'defined benefits' to 'defined contributions and What effect does this have on pension planning? Regarding pension reform, how has the Canadian government changed the public pension system to provide better coverage for all Canadians?

then after completing it you can write in second topic tell what are some of the financial concerns that Mitch and Karen have With respect to gender differences, what are the concerns facing Karen specifically? in last paragraph tell about is Mitch should increase his contribution to his 401k from $6000/year to $18,000/year?

you can write this answer in this structure for more information you can comment me

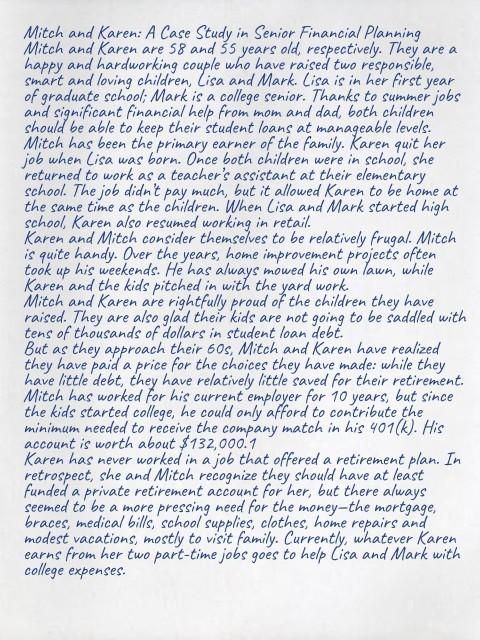

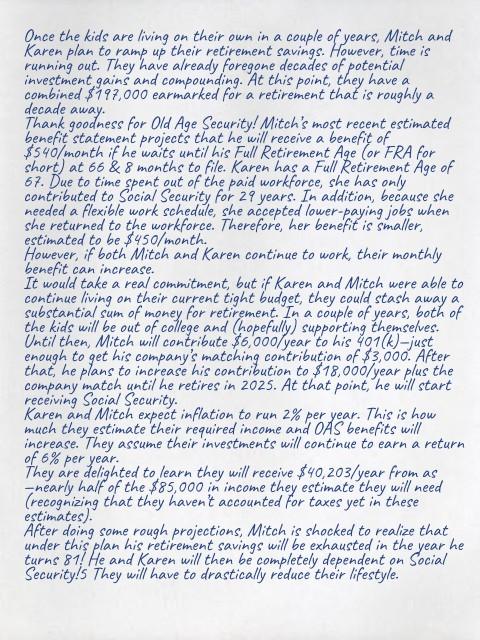

case study Question 1. Clear all the points in a question by using material from mitch and Karen case study first of all tell what are some of the financial concerns that Mitch and Karen have With respect to gender differences and what are the concerns facing Karen specifically. Do you think Mitch should increase his contribution to his 401k from $6000/year to $18,000/year and in the second paragraph tell Why do some older people live in poverty today in spite of the drop in poverty rates you should also clear the point that What are the implications of shifting from 'defined benefits' to 'defined contributions what effect does this have on pension planning. Regarding pension reform, how has the Canadian government changed the public pension system to provide better coverage for all Canadians at the last of the question, tell the one strength and weakness of Canada's public pension system.? Mitch and Karen: A Case Study in Senior Financial Planning Mitch and Karen are 58 and 5 years old, respectively. They are a happy and hardworking couple who have raised two responsible, smart and loving children, Lisa and Mark. Lisa is in her first year of graduate school; Mark is a college senior. Thanks to summer jobs and significant financial help from mom and dad, both children should be able to keep their student loans at manageable levels. Mitch has been the primary earner of the family. Karen quit her job when Lisa was born. Once both children were in school , she returned to work as a teacher's assistant at their elementary school. The job didn't pay much, but it allowed Karen to be home at the same time as the children. When Lisa and Mark started high school , Karen also resumed working in retail. Karen and Mitch consider themselves to be relatively frugal. Mitch is quite handy. Over the years, home improvement projects often took up his weekends. He has always mowed his own lawn, while Karen and the kids pitched in with the yard work. Mitch and Karen are rightfully proud of the children they have raised. They are also glad their kids are not going to be saddled with tens of thousands of dollars in student loan debt. But as they approach their 60s, Mitch and Karen have realized they have paid a price for the choices they have made: while they have little debt, they have relatively little saved for their retirement. Mitch has worked for his current employer for 10 years, but since the kids started college, he could only' afford to contribute the minimum needed to receive the company match in his 401(k). His account is worth about $132,000.1 Karen has never worked in a job that offered a retirement plan. In retrospect, she and Mitch recognize they should have at least funded a private retirement account for her, but there always seemed to be a more pressing need for the money-the mortgage, braces, medical bills, school supplies, clothes, home repairs and modest vacations, mostly to visit family. Currently, whatever Karen earns from her two part-time jobs goes to help Lisa and Mark with college expenses. decade away Once the kids are living on their own in a couple of years, Mitch and Karen plan to ramp up their retirement savings. However, time is running out. They have already foregone decades of potential combined $197.000 earmarked for a retirement that is roughly a Thank goodness for Old Age Security! Mitch's most recent estimated benefit statement projects that he will receive a benefit of $540/month if he waits until his Full Retirement Age (or FRA for short) at 66 & 8 months to file. Karen has a Full Retirement Age of 67. Due to time spent out of the paid workforce, she has only contributed to Social Security for 29 years. In addition, because she needed a flexible work schedule, she accepted lower-paying jobs when she returned to the workforce. Therefore, her benefit is smaller, estimated to be $450/month. However, if both Mitch and Karen continue to work, their monthly benefit can increase. It would take a real commitment, but if Karen and Mitch were able to continue living on their current tight budget, they could stash away a substantial sum of money for retirement. In a couple of years, both of the kids will be out of college and (hopefully) supporting themselves. Until then, Mitch will contribute $6.000/year to his 401(k)-just enough to get his company's matching contribution of $3,000. After that, he plans to increase his contribution to $18,000/year plus the company match until he retires in 2025. At that point, he will start receiving Social Security. Karen and Mitch expect inflation to run 2% per year. This is how much they estimate their required income and OAS benefits will increase. They assume their investments will continue to earn a return of 6% per year. They are delighted to learn they will receive $40,203/year from as anearly half of the $85,000 in income they estimate they will need (recognizing that they havent accounted for taxes yet in these estimates). After doing some rough projections, Mitch is shocked to realize that under this plan his retirement savings will be exhausted in the year he turns 81. He and Karen will then be completely dependent on Social Security! They will have to drastically reduce their lifestyle. case study Question 1. Clear all the points in a question by using material from mitch and Karen case study first of all tell what are some of the financial concerns that Mitch and Karen have With respect to gender differences and what are the concerns facing Karen specifically. Do you think Mitch should increase his contribution to his 401k from $6000/year to $18,000/year and in the second paragraph tell Why do some older people live in poverty today in spite of the drop in poverty rates you should also clear the point that What are the implications of shifting from 'defined benefits' to 'defined contributions what effect does this have on pension planning. Regarding pension reform, how has the Canadian government changed the public pension system to provide better coverage for all Canadians at the last of the question, tell the one strength and weakness of Canada's public pension system.? Mitch and Karen: A Case Study in Senior Financial Planning Mitch and Karen are 58 and 5 years old, respectively. They are a happy and hardworking couple who have raised two responsible, smart and loving children, Lisa and Mark. Lisa is in her first year of graduate school; Mark is a college senior. Thanks to summer jobs and significant financial help from mom and dad, both children should be able to keep their student loans at manageable levels. Mitch has been the primary earner of the family. Karen quit her job when Lisa was born. Once both children were in school , she returned to work as a teacher's assistant at their elementary school. The job didn't pay much, but it allowed Karen to be home at the same time as the children. When Lisa and Mark started high school , Karen also resumed working in retail. Karen and Mitch consider themselves to be relatively frugal. Mitch is quite handy. Over the years, home improvement projects often took up his weekends. He has always mowed his own lawn, while Karen and the kids pitched in with the yard work. Mitch and Karen are rightfully proud of the children they have raised. They are also glad their kids are not going to be saddled with tens of thousands of dollars in student loan debt. But as they approach their 60s, Mitch and Karen have realized they have paid a price for the choices they have made: while they have little debt, they have relatively little saved for their retirement. Mitch has worked for his current employer for 10 years, but since the kids started college, he could only' afford to contribute the minimum needed to receive the company match in his 401(k). His account is worth about $132,000.1 Karen has never worked in a job that offered a retirement plan. In retrospect, she and Mitch recognize they should have at least funded a private retirement account for her, but there always seemed to be a more pressing need for the money-the mortgage, braces, medical bills, school supplies, clothes, home repairs and modest vacations, mostly to visit family. Currently, whatever Karen earns from her two part-time jobs goes to help Lisa and Mark with college expenses. decade away Once the kids are living on their own in a couple of years, Mitch and Karen plan to ramp up their retirement savings. However, time is running out. They have already foregone decades of potential combined $197.000 earmarked for a retirement that is roughly a Thank goodness for Old Age Security! Mitch's most recent estimated benefit statement projects that he will receive a benefit of $540/month if he waits until his Full Retirement Age (or FRA for short) at 66 & 8 months to file. Karen has a Full Retirement Age of 67. Due to time spent out of the paid workforce, she has only contributed to Social Security for 29 years. In addition, because she needed a flexible work schedule, she accepted lower-paying jobs when she returned to the workforce. Therefore, her benefit is smaller, estimated to be $450/month. However, if both Mitch and Karen continue to work, their monthly benefit can increase. It would take a real commitment, but if Karen and Mitch were able to continue living on their current tight budget, they could stash away a substantial sum of money for retirement. In a couple of years, both of the kids will be out of college and (hopefully) supporting themselves. Until then, Mitch will contribute $6.000/year to his 401(k)-just enough to get his company's matching contribution of $3,000. After that, he plans to increase his contribution to $18,000/year plus the company match until he retires in 2025. At that point, he will start receiving Social Security. Karen and Mitch expect inflation to run 2% per year. This is how much they estimate their required income and OAS benefits will increase. They assume their investments will continue to earn a return of 6% per year. They are delighted to learn they will receive $40,203/year from as anearly half of the $85,000 in income they estimate they will need (recognizing that they havent accounted for taxes yet in these estimates). After doing some rough projections, Mitch is shocked to realize that under this plan his retirement savings will be exhausted in the year he turns 81. He and Karen will then be completely dependent on Social Security! They will have to drastically reduce their lifestyleStep by Step Solution

There are 3 Steps involved in it

Step: 1

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Stephen L. Nesbitt

2nd Edition

1119944392, 978-1119944393