Answered step by step

Verified Expert Solution

Question

1 Approved Answer

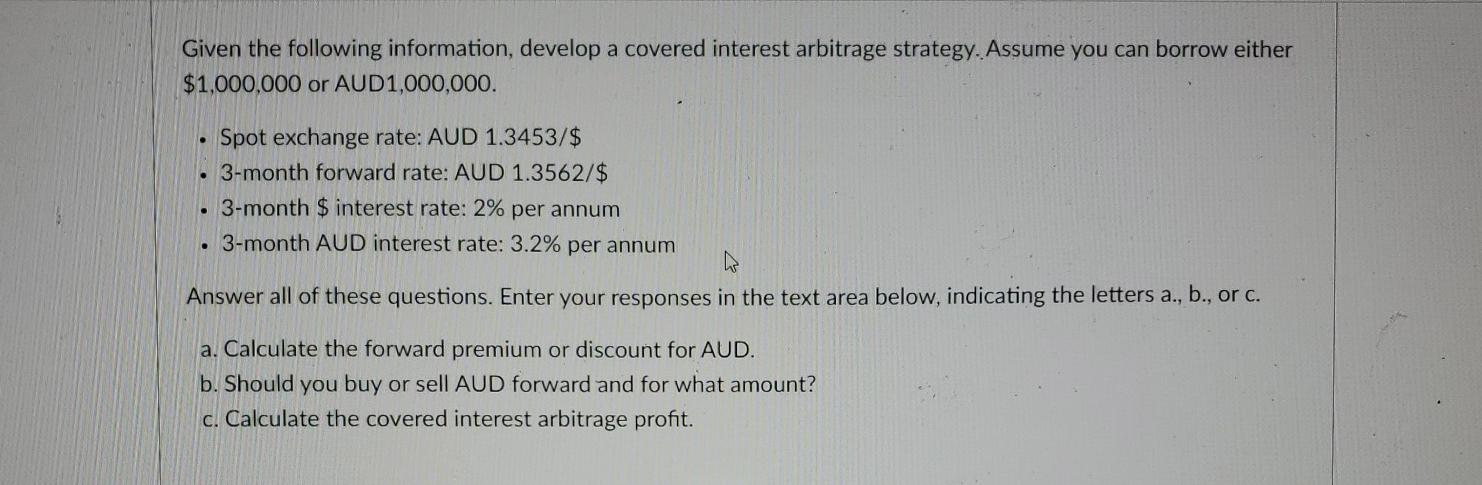

Given the following information, develop a covered interest arbitrage strategy. Assume you can borrow either $1,000,000 or AUD1,000,000. . . Spot exchange rate: AUD 1.3453/$

Given the following information, develop a covered interest arbitrage strategy. Assume you can borrow either $1,000,000 or AUD1,000,000. . . Spot exchange rate: AUD 1.3453/$ 3-month forward rate: AUD 1.3562/$ . 3-month $ interest rate: 2% per annum . 3-month AUD interest rate: 3.2% per annum Answer all of these questions. Enter your responses in the text area below, indicating the letters a., b., or C. a. Calculate the forward premium or discount for AUD. b. Should you buy or sell AUD forward and for what amount? c. Calculate the covered interest arbitrage profit

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Cheol Eun, Bruce Resnick

5thEdition

0073382345, 9780073382340