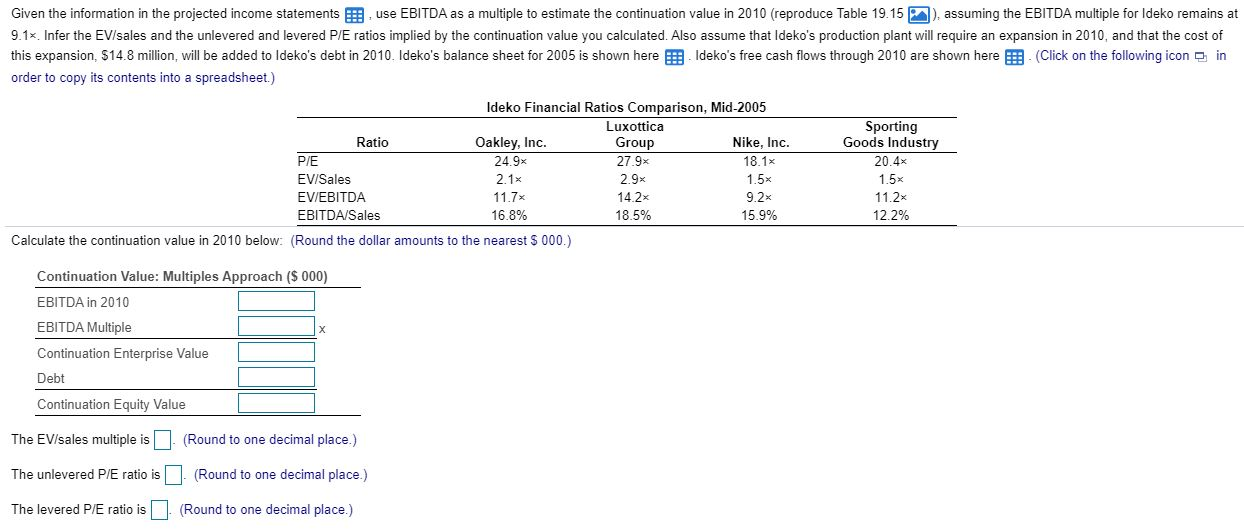

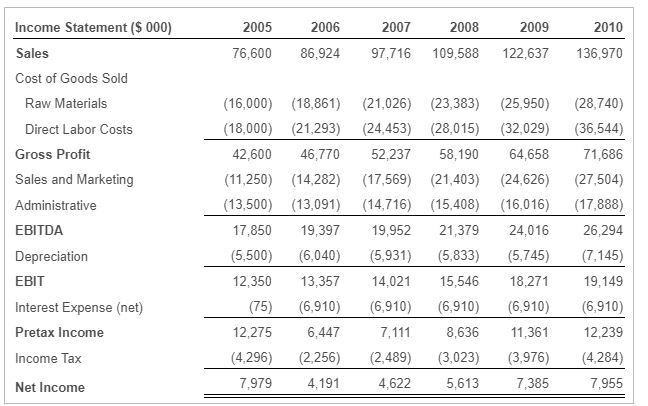

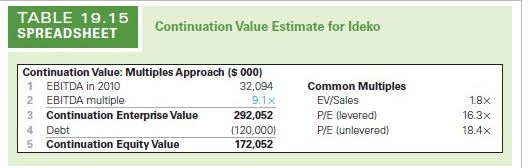

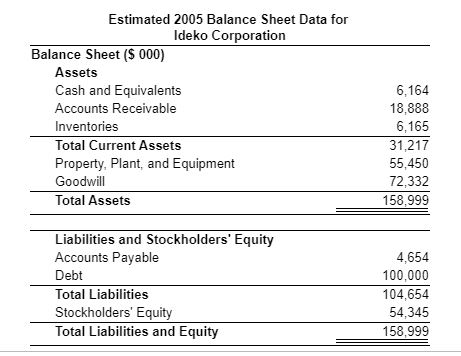

Given the information in the projected income statements , use EBITDA as a multiple to estimate the continuation value in 2010 (reproduce Table 19.15 ), assuming the EBITDA multiple for Ideko remains at 9.1x. Infer the EV/sales and the unlevered and levered P/E ratios implied by the continuation value you calculated. Also assume that Ideko's production plant will require an expansion in 2010, and that the cost of this expansion, $14.8 million, will be added to Ideko's debt in 2010. Ideko's balance sheet for 2005 is shown here . ldeko's free cash flows through 2010 are shown here . (Click on the following icon in order to copy its contents into a spreadsheet.) Ideko Financial Ratios Comparison, Mid-2005 Luxottica Ratio Oakley, Inc. Group Nike, Inc. PIE 24.9x 27.9 18.1% EV/Sales 2.1 2.9x 1.5% EV/EBITDA 11.7x 14.2 9.2x EBITDA/Sales 16.8% 18.5% 15.9% Calculate the continuation value in 2010 below: (Round the dollar amounts to the nearest S 000.) Sporting Goods Industry 20.4% 1.5% 11.2x 12.2% Continuation Value: Multiples Approach ($ 000) EBITDA in 2010 EBITDA Multiple Continuation Enterprise Value Debt Continuation Equity Value The EV/sales multiple is (Round to one decimal place.) The unlevered P/E ratio is (Round to one decimal place.) The levered P/E ratio is . (Round to one decimal place.) Income Statement ($ 000) 2005 76,600 2006 86,924 2007 97,716 2008 109,588 2009 122,637 2010 136,970 Sales Cost of Goods Sold Raw Materials Direct Labor Costs Gross Profit Sales and Marketing Administrative EBITDA (16,000) (18,000) 42,600 (11,250) (13,500) 17,850 (5,500) 12,350 (75) 12,275 (4.296) 7,979 (18,861) (21,293) 46,770 (14,282) (13,091) 19,397 (6,040) 13,357 (6,910) 6,447 (2,256) 4,191 (21,026) (24.453) 52,237 (17,569) (14,716) 19,952 (5,931) 14.021 (6,910) 7,111 (2,489) 4,622 (23,383) (28,015) 58,190 (21,403) (15,408) 21,379 (5,833) 15,546 (6,910) 8 636 (3,023) 5,613 (25,950) (32,029) 64,658 (24.626) (16,016) 24,016 (5,745) 18,271 (6,910) 11,361 (3,976) 7,385 (28,740) (36,544) 71,686 (27,504) (17,888) 26,294 (7.145) 19,149 (6,910) 12,239 (4.284) 7,955 Depreciation EBIT Interest Expense (net) Pretax Income Income Tax Net Income TABLE 19.15 SPREADSHEET Continuation Value Estimate for ldeko Continuation Value: Multiples Approach ($ 000) 1 EBITDA in 2010 32,094 2 EBITDA multiple 9.1 x 3 Continuation Enterprise Value 292,052 4 Debt (120,000) 5 Continuation Equity Value 172,052 Common Multiples EV/Sales P/E (levered) P/E (unlevered) 1.8% 16.3x 18.4x Estimated 2005 Balance Sheet Data for Ideko Corporation Balance Sheet ($ 000) Assets Cash and Equivalents Accounts Receivable Inventories Total Current Assets Property, Plant, and Equipment Goodwill Total Assets 6,164 18,888 6,165 31,217 55,450 72,332 158,999 Liabilities and Stockholders' Equity Accounts Payable Debt Total Liabilities Stockholders' Equity Total Liabilities and Equity 4,654 100.000 104,654 54,345 158,999 2005 2010 7,955 4.492 Free Cash Flow ($ 000) Net Income Plus: After-tax Interest Expense Unlevered Net Income Plus: Depreciation Less: Increase in NWC 12,447 2006 4.191 4,492 8,683 6,040 (3,659) (4,950) 6,114 2007 4 ,622 4.492 9,114 5,931 (3,603) (4.950) 6,492 2008 5,613 4.492 10,105 5,833 (3,986) (4.950) 7,002 2009 7,385 4.492 11,877 5,745 (4.515) (4.950) 8,157 Less: Capital Expenditures Free Cash Flow of Firm 7,145 (4,995) (19,750) (5,153) 14,800 (4.492) 5,155 Plus: Net Borrowing Less: After-tax Interest Expense Free Cash Flow to Equity (4.492) 1,622 (4.492) 2,000 (4.492) 2,510 (4.492) 2,510 i Click the icon to see the Worked Solution (Formula Solution). Calculate the continuation value in 2010 below: (Round the dollar amounts to the nearest $ 000.) Continuation Value: Multiples Approach ($ 000) EBITDA in 2010 26,294 EBITDA Multiple 9.1 x Continuation Enterprise Value 239,276 Debt (114,800) Continuation Equity Value 124,475 The EV/sales multiple is 1.7. (Round to one decimal place.) The unlevered P/E ratio is 19.2(Round to one decimal place.) The levered P/E ratio is 15.6". (Round to one decimal place.) Given the information in the projected income statements , use EBITDA as a multiple to estimate the continuation value in 2010 (reproduce Table 19.15 ), assuming the EBITDA multiple for Ideko remains at 9.1x. Infer the EV/sales and the unlevered and levered P/E ratios implied by the continuation value you calculated. Also assume that Ideko's production plant will require an expansion in 2010, and that the cost of this expansion, $14.8 million, will be added to Ideko's debt in 2010. Ideko's balance sheet for 2005 is shown here . ldeko's free cash flows through 2010 are shown here . (Click on the following icon in order to copy its contents into a spreadsheet.) Ideko Financial Ratios Comparison, Mid-2005 Luxottica Ratio Oakley, Inc. Group Nike, Inc. PIE 24.9x 27.9 18.1% EV/Sales 2.1 2.9x 1.5% EV/EBITDA 11.7x 14.2 9.2x EBITDA/Sales 16.8% 18.5% 15.9% Calculate the continuation value in 2010 below: (Round the dollar amounts to the nearest S 000.) Sporting Goods Industry 20.4% 1.5% 11.2x 12.2% Continuation Value: Multiples Approach ($ 000) EBITDA in 2010 EBITDA Multiple Continuation Enterprise Value Debt Continuation Equity Value The EV/sales multiple is (Round to one decimal place.) The unlevered P/E ratio is (Round to one decimal place.) The levered P/E ratio is . (Round to one decimal place.) Income Statement ($ 000) 2005 76,600 2006 86,924 2007 97,716 2008 109,588 2009 122,637 2010 136,970 Sales Cost of Goods Sold Raw Materials Direct Labor Costs Gross Profit Sales and Marketing Administrative EBITDA (16,000) (18,000) 42,600 (11,250) (13,500) 17,850 (5,500) 12,350 (75) 12,275 (4.296) 7,979 (18,861) (21,293) 46,770 (14,282) (13,091) 19,397 (6,040) 13,357 (6,910) 6,447 (2,256) 4,191 (21,026) (24.453) 52,237 (17,569) (14,716) 19,952 (5,931) 14.021 (6,910) 7,111 (2,489) 4,622 (23,383) (28,015) 58,190 (21,403) (15,408) 21,379 (5,833) 15,546 (6,910) 8 636 (3,023) 5,613 (25,950) (32,029) 64,658 (24.626) (16,016) 24,016 (5,745) 18,271 (6,910) 11,361 (3,976) 7,385 (28,740) (36,544) 71,686 (27,504) (17,888) 26,294 (7.145) 19,149 (6,910) 12,239 (4.284) 7,955 Depreciation EBIT Interest Expense (net) Pretax Income Income Tax Net Income TABLE 19.15 SPREADSHEET Continuation Value Estimate for ldeko Continuation Value: Multiples Approach ($ 000) 1 EBITDA in 2010 32,094 2 EBITDA multiple 9.1 x 3 Continuation Enterprise Value 292,052 4 Debt (120,000) 5 Continuation Equity Value 172,052 Common Multiples EV/Sales P/E (levered) P/E (unlevered) 1.8% 16.3x 18.4x Estimated 2005 Balance Sheet Data for Ideko Corporation Balance Sheet ($ 000) Assets Cash and Equivalents Accounts Receivable Inventories Total Current Assets Property, Plant, and Equipment Goodwill Total Assets 6,164 18,888 6,165 31,217 55,450 72,332 158,999 Liabilities and Stockholders' Equity Accounts Payable Debt Total Liabilities Stockholders' Equity Total Liabilities and Equity 4,654 100.000 104,654 54,345 158,999 2005 2010 7,955 4.492 Free Cash Flow ($ 000) Net Income Plus: After-tax Interest Expense Unlevered Net Income Plus: Depreciation Less: Increase in NWC 12,447 2006 4.191 4,492 8,683 6,040 (3,659) (4,950) 6,114 2007 4 ,622 4.492 9,114 5,931 (3,603) (4.950) 6,492 2008 5,613 4.492 10,105 5,833 (3,986) (4.950) 7,002 2009 7,385 4.492 11,877 5,745 (4.515) (4.950) 8,157 Less: Capital Expenditures Free Cash Flow of Firm 7,145 (4,995) (19,750) (5,153) 14,800 (4.492) 5,155 Plus: Net Borrowing Less: After-tax Interest Expense Free Cash Flow to Equity (4.492) 1,622 (4.492) 2,000 (4.492) 2,510 (4.492) 2,510 i Click the icon to see the Worked Solution (Formula Solution). Calculate the continuation value in 2010 below: (Round the dollar amounts to the nearest $ 000.) Continuation Value: Multiples Approach ($ 000) EBITDA in 2010 26,294 EBITDA Multiple 9.1 x Continuation Enterprise Value 239,276 Debt (114,800) Continuation Equity Value 124,475 The EV/sales multiple is 1.7. (Round to one decimal place.) The unlevered P/E ratio is 19.2(Round to one decimal place.) The levered P/E ratio is 15.6". (Round to one decimal place.)