Answered step by step

Verified Expert Solution

Question

1 Approved Answer

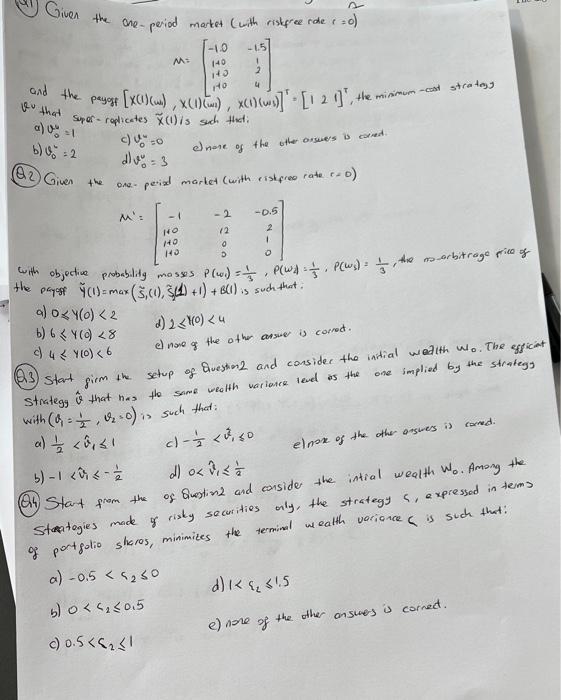

Given the one- and the payoff Ru that period market (with riskfree rader =0) [-1.0 -15] M: 140 143 2 140 4 # [X(1)(cm), X(1)(u),

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Grow Your Small Business Profits How I Find A 100K In Any Business In 45 Minutes

Authors: Sharon Coleman

1st Edition

B0C9S9CCZJ, 979-8850917258