Answered step by step

Verified Expert Solution

Question

1 Approved Answer

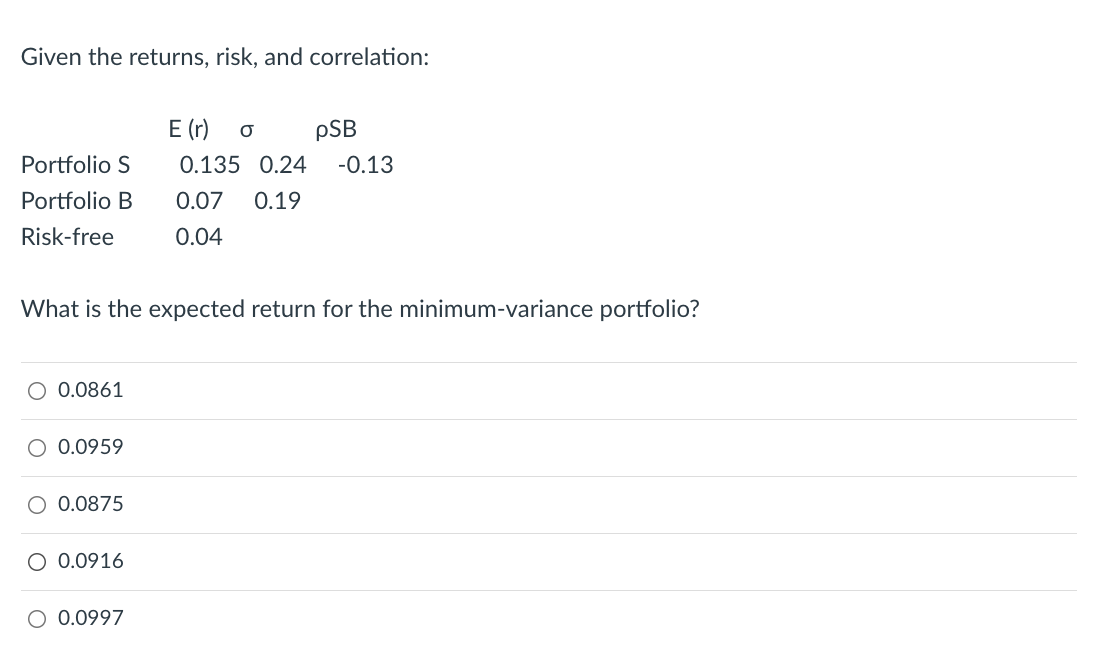

Given the returns, risk, and correlation: E (r) O pSB Portfolio S 0.135 0.24 -0.13 Portfolio B 0.07 0.19 Risk-free 0.04 What is the expected

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Financial Management

Authors: James C. Van Horne

10th Edition

0138596875, 978-0138596873