Answered step by step

Verified Expert Solution

Question

1 Approved Answer

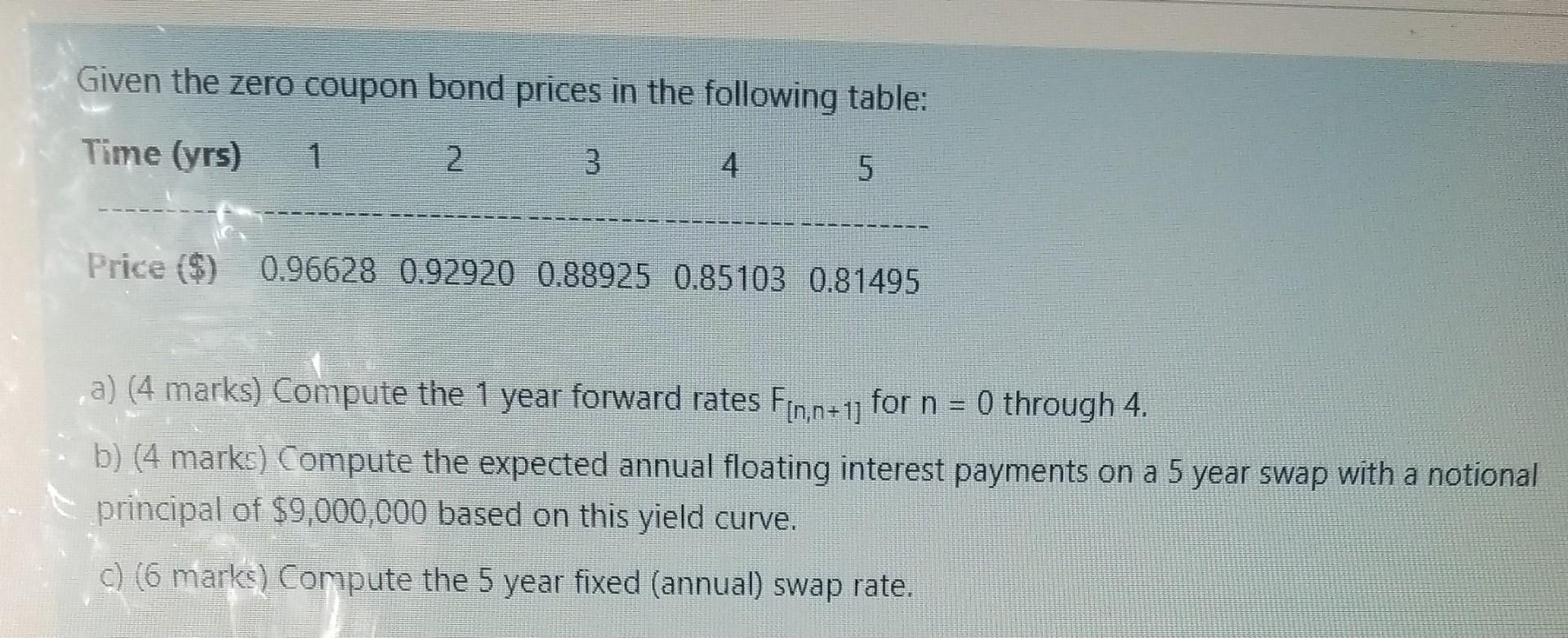

Given the zero coupon bond prices in the following table: Time (yrs) 1 2 3 5 Price ($) 0.96628 0.92920 0.88925 0.85103 0.81495 a) (4

Given the zero coupon bond prices in the following table: Time (yrs) 1 2 3 5 Price ($) 0.96628 0.92920 0.88925 0.85103 0.81495 a) (4 marks) Compute the 1 year forward rates Fin, n = 11 for n = 0 through 4. b) (4 marks) Compute the expected annual floating interest payments on a 5 year swap with a notional principal of $9,000,000 based on this yield curve. c) (6 marks) Compute the 5 year fixed (annual) swap rate

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: Jack Kapoor, Les Dlabay, Robert Hughes, Melissa Hart

14th Edition

1264101597, 9781264101597