Answered step by step

Verified Expert Solution

Question

1 Approved Answer

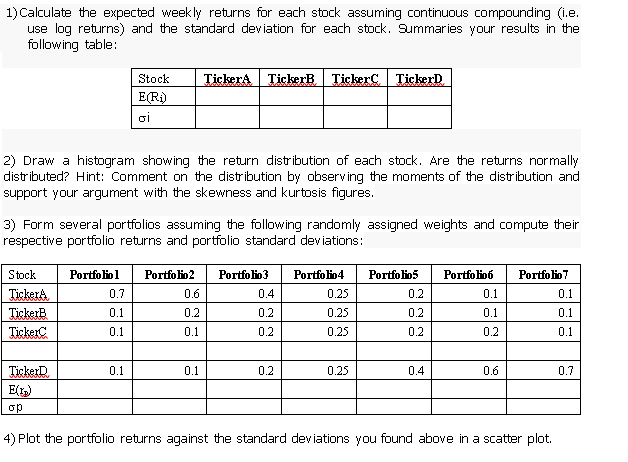

Giving the following table (DO the Job in Excel) Date A B C D index 3-Jan-16 84.87 14.05 67.55 41.7 6,517.71 10-Jan-16 67.02 12.25 57.84

Giving the following table (DO the Job in Excel)

| Date | A | B | C | D | index |

| 3-Jan-16 | 84.87 | 14.05 | 67.55 | 41.7 | 6,517.71 |

| 10-Jan-16 | 67.02 | 12.25 | 57.84 | 37.4 | 6,038.03 |

| 17-Jan-16 | 54.05 | 9.7 | 45.8 | 34 | 5,459.84 |

| 24-Jan-16 | 59.93 | 10.35 | 47.07 | 38.6 | 5,698.56 |

| 31-Jan-16 | 66.53 | 11.4 | 55.09 | 41.1 | 5,927.36 |

| 7-Feb-16 | 64.82 | 11.65 | 52.35 | 42.5 | 5,832.92 |

| 14-Feb-16 | 62.13 | 11.2 | 39.89 | 41 | 5,801.65 |

| 21-Feb-16 | 66.28 | 11.3 | 40.74 | 41.8 | 5,942.28 |

| 28-Feb-16 | 68.24 | 11.95 | 42 | 42.8 | 6,170.16 |

| 6-Mar-16 | 67.51 | 12.35 | 47.07 | 44.5 | 6,370.37 |

| 13-Mar-16 | 76.07 | 12.8 | 49.39 | 44 | 6,305.78 |

| 20-Mar-16 | 72.15 | 13.35 | 49.18 | 43 | 6,460.98 |

| 27-Mar-16 | 68 | 13.25 | 50.66 | 41 | 6,215.65 |

| 3-Apr-16 | 64.33 | 13.9 | 43.27 | 41.8 | 6,213.58 |

| 10-Apr-16 | 66.04 | 14.5 | 47.7 | 44.5 | 6,442.04 |

| 17-Apr-16 | 66.77 | 14.95 | 47.07 | 47.5 | 6,512.43 |

| 24-Apr-16 | 69.95 | 15.05 | 53.61 | 49.1 | 6,820.30 |

| 1-May-16 | 67.26 | 14 | 57.84 | 48 | 6,586.50 |

| 8-May-16 | 71.18 | 13.55 | 61.64 | 50.5 | 6,654.20 |

| 15-May-16 | 68.97 | 14.2 | 58.68 | 51 | 6,737.40 |

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Banking Secrecy And Global Finance

Authors: Donato Masciandaro, Olga Balakina

1st Edition

1137400099, 978-1137400093