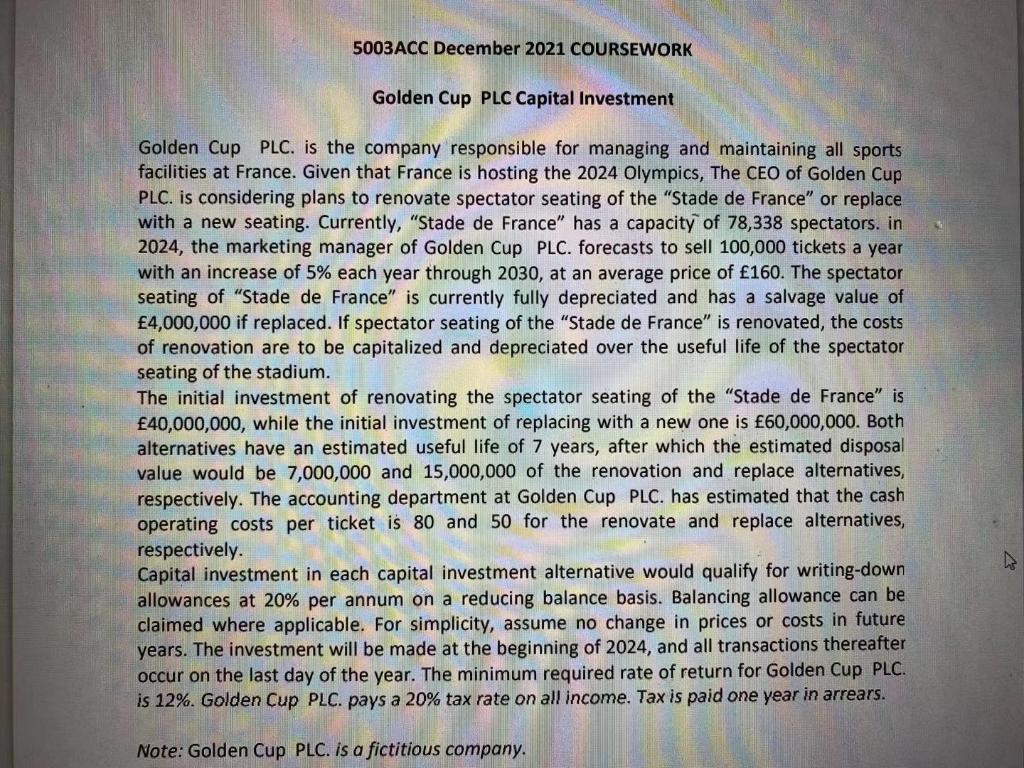

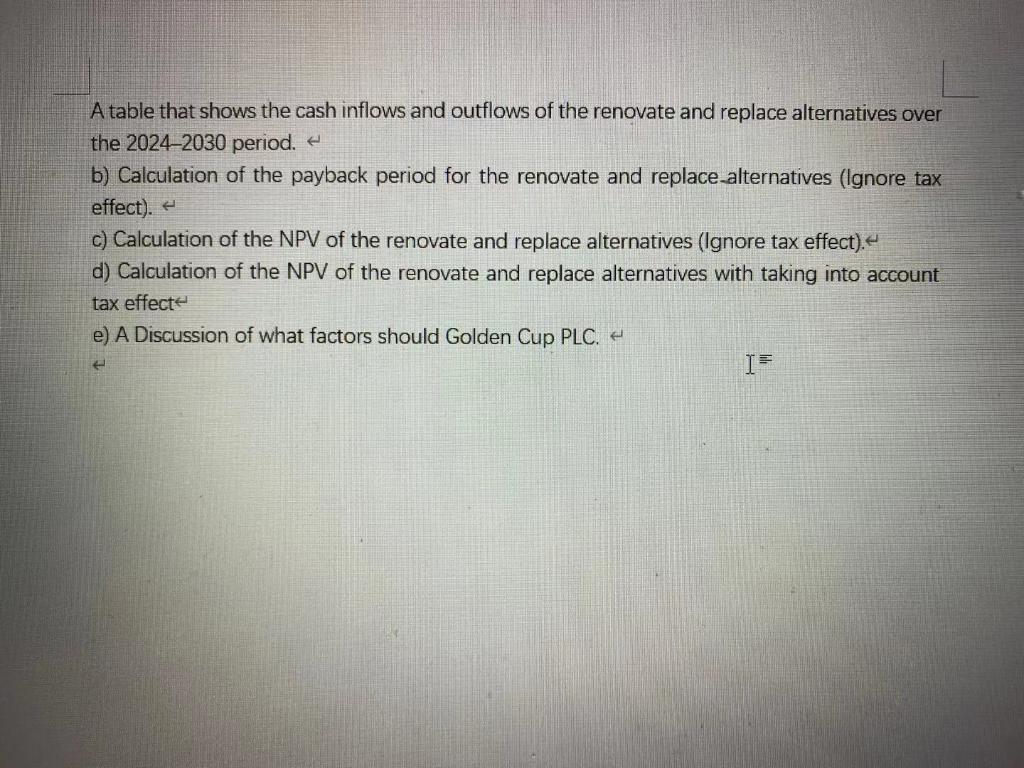

Golden Cup PLC Capital Investment Golden Cup PLC. is the company responsible for managing and maintaining all sports facilities at France. Given that France is hosting the 2024 Olympics, The CEO of Golden Cup PLC. is considering plans to renovate spectator seating of the Stade de France or replace with a new seating. Currently, Stade de France has a capacity of 78,338 spectators. in 2024, the marketing manager of Golden Cup PLC. forecasts to sell 100,000 tickets a year with an increase of 5% each year through 2030, at an average price of 160. The spectator seating of Stade de France is currently fully depreciated and has a salvage value of 4,000,000 if replaced. If spectator seating of the Stade de France is renovated, the costs of renovation are to be capitalized and depreciated over the useful life of the spectator seating of the stadium. The initial investment of renovating the spectator seating of the Stade de France is 40,000,000, while the initial investment of replacing with a new one is 60,000,000. Both alternatives have an estimated useful life of 7 years, after which the estimated disposal value would be 7,000,000 and 15,000,000 of the renovation and replace alternatives, respectively. The accounting department at Golden Cup PLC. has estimated that the cash operating costs per ticket is 80 and 50 for the renovate and replace alternatives, respectively. Capital investment in each capital investment alternative would qualify for writing-down allowances at 20% per annum on a reducing balance basis. Balancing allowance can be claimed where applicable. For simplicity, assume no change in prices or costs in future years. The investment will be made at the beginning of 2024, and all transactions thereafter occur on the last day of the year. The minimum required rate of return for Golden Cup PLC. is 12%. Golden Cup PLC. pays a 20% tax rate on all income. Tax is paid one year in arrears. Note: Golden Cup PLC. is a fictitious company. a) A table that shows the cash inflows and outflows of the renovate and replace alternatives over the 20242030 period. b) Calculation of the payback period for the renovate and replace alternatives (Ignore tax effect). c) Calculation of the NPV of the renovate and replace alternatives (Ignore tax effect). d) Calculation of the NPV of the renovate and replace alternatives with taking into account tax effect. e) A Discussion of what factors should Golden Cup PLC.

Golden Cup PLC Capital Investment Golden Cup PLC. is the company responsible for managing and maintaining all sports facilities at France. Given that France is hosting the 2024 Olympics, The CEO of Golden Cup PLC. is considering plans to renovate spectator seating of the Stade de France or replace with a new seating. Currently, Stade de France has a capacity of 78,338 spectators. in 2024, the marketing manager of Golden Cup PLC. forecasts to sell 100,000 tickets a year with an increase of 5% each year through 2030, at an average price of 160. The spectator seating of Stade de France is currently fully depreciated and has a salvage value of 4,000,000 if replaced. If spectator seating of the Stade de France is renovated, the costs of renovation are to be capitalized and depreciated over the useful life of the spectator seating of the stadium. The initial investment of renovating the spectator seating of the Stade de France is 40,000,000, while the initial investment of replacing with a new one is 60,000,000. Both alternatives have an estimated useful life of 7 years, after which the estimated disposal value would be 7,000,000 and 15,000,000 of the renovation and replace alternatives, respectively. The accounting department at Golden Cup PLC. has estimated that the cash operating costs per ticket is 80 and 50 for the renovate and replace alternatives, respectively. Capital investment in each capital investment alternative would qualify for writing-down allowances at 20% per annum on a reducing balance basis. Balancing allowance can be claimed where applicable. For simplicity, assume no change in prices or costs in future years. The investment will be made at the beginning of 2024, and all transactions thereafter occur on the last day of the year. The minimum required rate of return for Golden Cup PLC. is 12%. Golden Cup PLC. pays a 20% tax rate on all income. Tax is paid one year in arrears. Note: Golden Cup PLC. is a fictitious company. a) A table that shows the cash inflows and outflows of the renovate and replace alternatives over the 20242030 period. b) Calculation of the payback period for the renovate and replace alternatives (Ignore tax effect). c) Calculation of the NPV of the renovate and replace alternatives (Ignore tax effect). d) Calculation of the NPV of the renovate and replace alternatives with taking into account tax effect. e) A Discussion of what factors should Golden Cup PLC.

5003ACC December 2021 COURSEWORK Golden Cup PLC Capital Investment Golden Cup PLC. is the company responsible for managing and maintaining all sports facilities at France. Given that France is hosting the 2024 Olympics, The CEO of Golden Cup PLC. is considering plans to renovate spectator seating of the "Stade de France" or replace with a new seating. Currently, "Stade de France" has a capacity of 78,338 spectators. in 2024, the marketing manager of Golden Cup PLC. forecasts to sell 100,000 tickets a year with an increase of 5% each year through 2030, at an average price of 160. The spectator seating of "Stade de France" is currently fully depreciated and has a salvage value of 4,000,000 if replaced. If spectator seating of the "Stade de France" is renovated, the costs of renovation are to be capitalized and depreciated over the useful life of the spectator seating of the stadium. The initial investment of renovating the spectator seating of the "Stade de France" is 40,000,000, while the initial investment of replacing with a new one is 60,000,000. Both alternatives have an estimated useful life of 7 years, after which the estimated disposal value would be 7,000,000 and 15,000,000 of the renovation and replace alternatives, respectively. The accounting department at Golden Cup PLC. has estimated that the cash operating costs per ticket is 80 and 50 for the renovate and replace alternatives, respectively. Capital investment in each capital investment alternative would qualify for writing down allowances at 20% per annum on a reducing balance basis. Balancing allowance can be claimed where applicable. For simplicity, assume no change in prices or costs in future years. The investment will be made at the beginning of 2024, and all transactions thereafter occur on the last day of the year. The minimum required rate of return for Golden Cup PLC. is 12%. Golden Cup PLC. pays a 20% tax rate on all income. Tax is paid one year in arrears. Note: Golden Cup PLC. is a fictitious company. A table that shows the cash inflows and outflows of the renovate and replace alternatives over the 2024-2030 period. b) Calculation of the payback period for the renovate and replace-alternatives (Ignore tax effect). + c) Calculation of the NPV of the renovate and replace alternatives (Ignore tax effect). d) Calculation of the NPV of the renovate and replace alternatives with taking into account tax effect e) A Discussion of what factors should Golden Cup PLC. H IS 5003ACC December 2021 COURSEWORK Golden Cup PLC Capital Investment Golden Cup PLC. is the company responsible for managing and maintaining all sports facilities at France. Given that France is hosting the 2024 Olympics, The CEO of Golden Cup PLC. is considering plans to renovate spectator seating of the "Stade de France" or replace with a new seating. Currently, "Stade de France" has a capacity of 78,338 spectators. in 2024, the marketing manager of Golden Cup PLC. forecasts to sell 100,000 tickets a year with an increase of 5% each year through 2030, at an average price of 160. The spectator seating of "Stade de France" is currently fully depreciated and has a salvage value of 4,000,000 if replaced. If spectator seating of the "Stade de France" is renovated, the costs of renovation are to be capitalized and depreciated over the useful life of the spectator seating of the stadium. The initial investment of renovating the spectator seating of the "Stade de France" is 40,000,000, while the initial investment of replacing with a new one is 60,000,000. Both alternatives have an estimated useful life of 7 years, after which the estimated disposal value would be 7,000,000 and 15,000,000 of the renovation and replace alternatives, respectively. The accounting department at Golden Cup PLC. has estimated that the cash operating costs per ticket is 80 and 50 for the renovate and replace alternatives, respectively. Capital investment in each capital investment alternative would qualify for writing down allowances at 20% per annum on a reducing balance basis. Balancing allowance can be claimed where applicable. For simplicity, assume no change in prices or costs in future years. The investment will be made at the beginning of 2024, and all transactions thereafter occur on the last day of the year. The minimum required rate of return for Golden Cup PLC. is 12%. Golden Cup PLC. pays a 20% tax rate on all income. Tax is paid one year in arrears. Note: Golden Cup PLC. is a fictitious company. A table that shows the cash inflows and outflows of the renovate and replace alternatives over the 2024-2030 period. b) Calculation of the payback period for the renovate and replace-alternatives (Ignore tax effect). + c) Calculation of the NPV of the renovate and replace alternatives (Ignore tax effect). d) Calculation of the NPV of the renovate and replace alternatives with taking into account tax effect e) A Discussion of what factors should Golden Cup PLC. H IS