Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Good Day Could you please assist in Financial Institution Management: A Risk Management Approach (9th Edition). Chapter 13 Question 10. Its about foreign currency. Thank

Good Day

Could you please assist in Financial Institution Management: A Risk Management Approach (9th Edition).

Chapter 13 Question 10.

Its about foreign currency.

Thank You

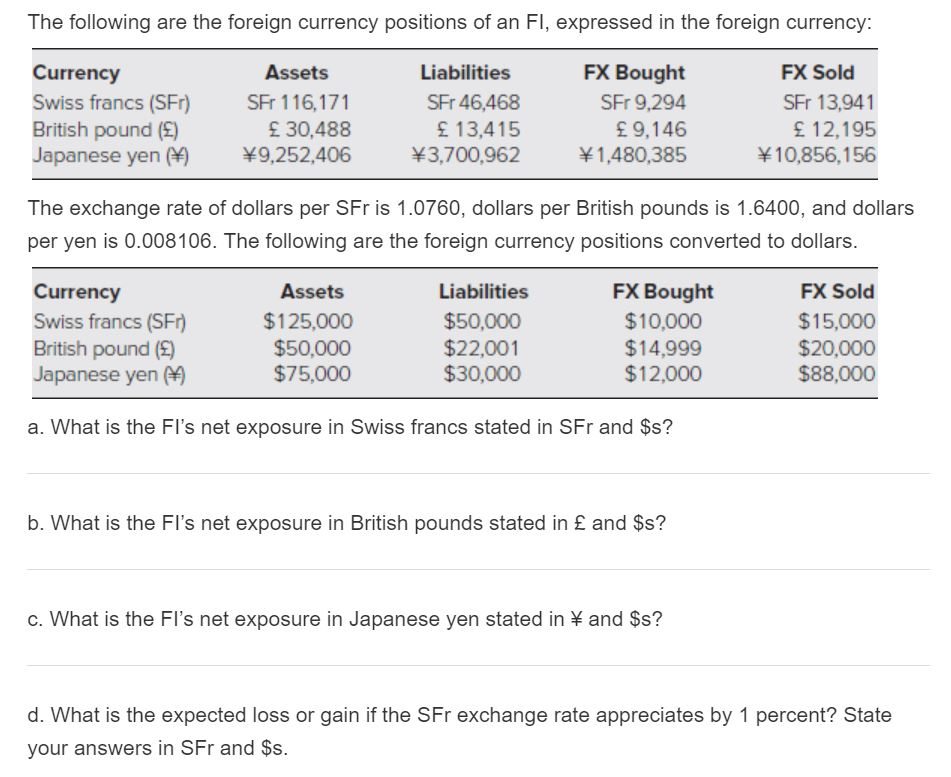

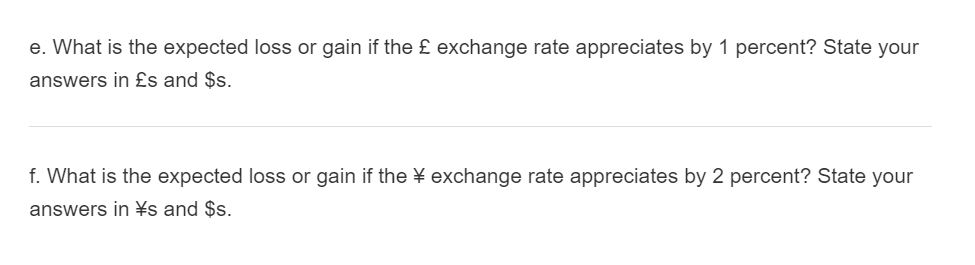

The following are the foreign currency positions of an FI, expressed in the foreign currency: Currency Swiss francs (SFr) British pound () Japanese yen () Assets SFr 116,171 30,488 9,252,406 Liabilities SFr 46,468 13,415 3,700,962 FX Bought SFr 9,294 9,146 1,480,385 FX Sold SFr 13,941 12,195 10,856,156 The exchange rate of dollars per SFr is 1.0760, dollars per British pounds is 1.6400, and dollars per yen is 0.008106. The following are the foreign currency positions converted to dollars. Currency Swiss francs (SFO) British pound () Japanese yen Assets $125,000 $50,000 $75,000 Liabilities $50,000 $22,001 $30,000 FX Bought $10.000 $14,999 $12,000 FX Sold $15,000 $20,000 $88,000 a. What is the Fl's net exposure in Swiss francs stated in SFr and $s? b. What is the Fl's net exposure in British pounds stated in and $s? c. What is the Fl's net exposure in Japanese yen stated in \ and $s? d. What is the expected loss or gain if the SFr exchange rate appreciates by 1 percent? State your answers in SFr and $s. e. What is the expected loss or gain if the exchange rate appreciates by 1 percent? State your answers in s and $s. f. What is the expected loss or gain if the \ exchange rate appreciates by 2 percent? State your answers in s and $sStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mechanical Day Trading Strategies

Authors: James Muranno

1st Edition

979-8392305735