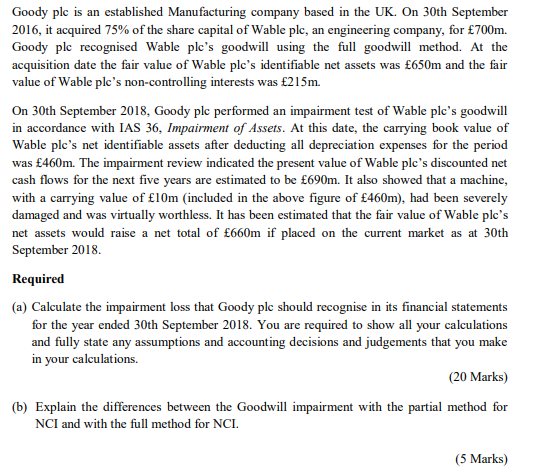

Goody plc is an established Manufacturing company based in the UK. On 30th September 2016, it acquired 75% of the share capital of Wable plc, an engineering company, for 700m. Goody plc recognised Wable plc's goodwill using the full goodwill method. At the acquisition date the fair value of Wable ple's identifiable net assets was 650m and the fair value of Wable ple's non-controlling interests was 215m. On 30th September 2018, Goody plc performed an impairment test of Wable ple's goodwill in accordance with IAS 36, Impairment of Assets. At this date, the carrying book value of Wable ple's net identifiable assets after deducting all depreciation expenses for the period was 460m. The impairment review indicated the present value of Wable plc's discounted net cash flows for the next five years are estimated to be 690m. It also showed that a machine, with a carrying value of 10m (included in the above figure of 460m), had been severely damaged and was virtually worthless. It has been estimated that the fair value of Wable ple's net assets would raise a net total of 660m if placed on the current market as at 30th September 2018 Required (a) Calculate the impairment loss that Goody ple should recognise in its financial statements for the year ended 30th September 2018. You are required to show all your calculations and fully state any assumptions and accounting decisions and judgements that you make in your calculations. (20 Marks) (b) Explain the differences between the Goodwill impairment with the partial method for NCI and with the full method for NCI. (5 Marks) Goody plc is an established Manufacturing company based in the UK. On 30th September 2016, it acquired 75% of the share capital of Wable plc, an engineering company, for 700m. Goody plc recognised Wable plc's goodwill using the full goodwill method. At the acquisition date the fair value of Wable ple's identifiable net assets was 650m and the fair value of Wable ple's non-controlling interests was 215m. On 30th September 2018, Goody plc performed an impairment test of Wable ple's goodwill in accordance with IAS 36, Impairment of Assets. At this date, the carrying book value of Wable ple's net identifiable assets after deducting all depreciation expenses for the period was 460m. The impairment review indicated the present value of Wable plc's discounted net cash flows for the next five years are estimated to be 690m. It also showed that a machine, with a carrying value of 10m (included in the above figure of 460m), had been severely damaged and was virtually worthless. It has been estimated that the fair value of Wable ple's net assets would raise a net total of 660m if placed on the current market as at 30th September 2018 Required (a) Calculate the impairment loss that Goody ple should recognise in its financial statements for the year ended 30th September 2018. You are required to show all your calculations and fully state any assumptions and accounting decisions and judgements that you make in your calculations. (20 Marks) (b) Explain the differences between the Goodwill impairment with the partial method for NCI and with the full method for NCI