Answered step by step

Verified Expert Solution

Question

1 Approved Answer

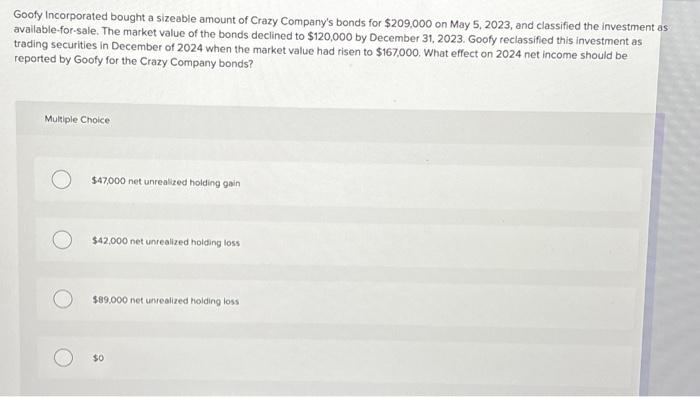

Goofy Incorporated bought a sizeable amount of Crazy Company's bonds for $209,000 on May 5, 2023, and classified the investment avaliable-for-sale. The market value of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Prescription Audit And Client Satisfaction A Health Service Research Study Based On Outdoor Patients

Authors: Amitabha Chattopadhyay

1st Edition

3843355541, 978-3843355544