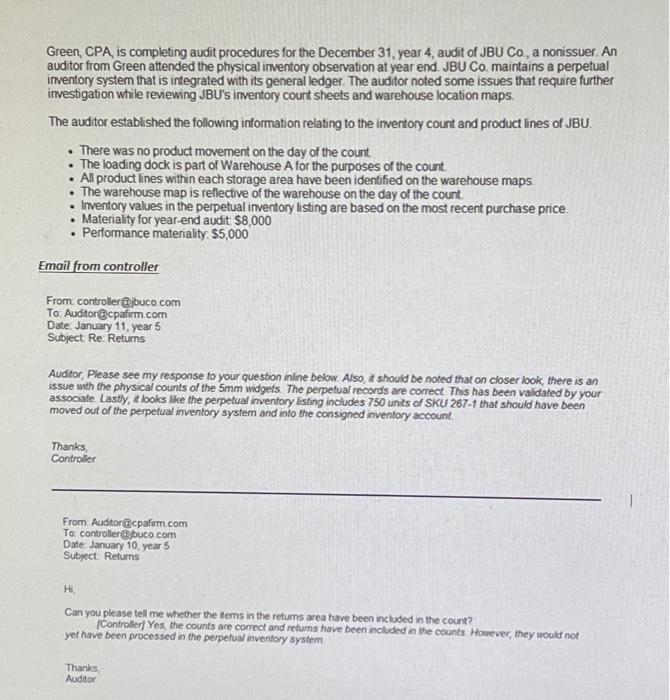

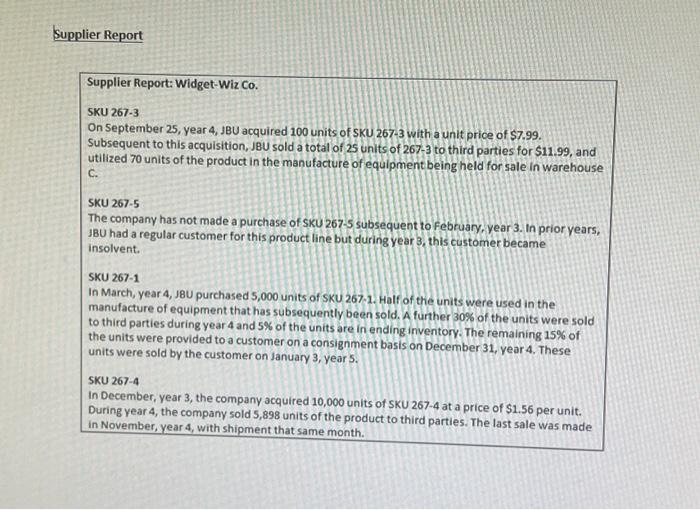

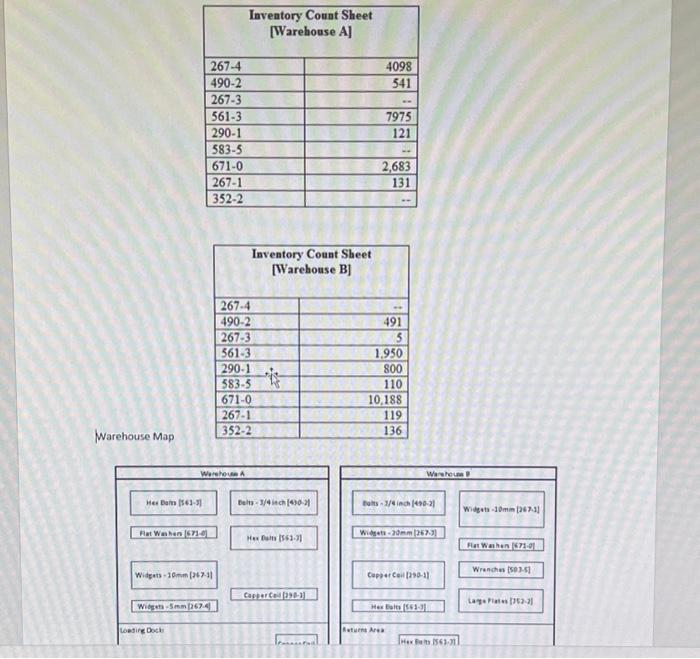

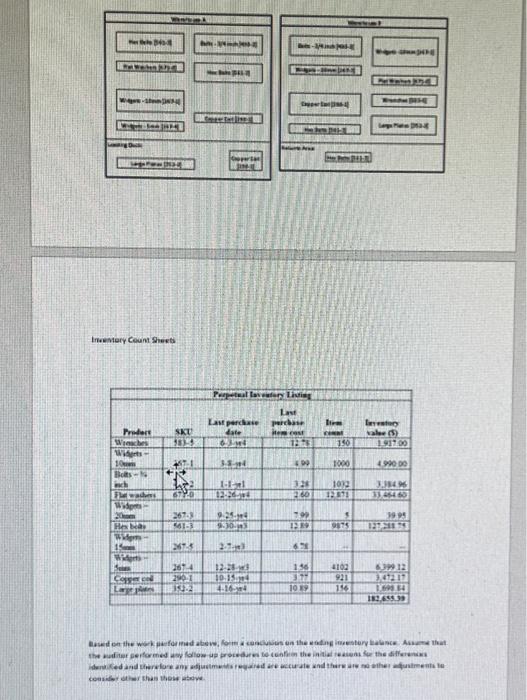

Green, CPA, is completing audit procedures for the December 31 , year 4 , audit of JBUC0, a nonissuer. An auditor from Green attended the physical irventory observation at year end. JBU Co. maintains a perpetual inventory system that is integrated with its general ledger. The auditor noted some issues that require further investigation while reviewing JBU's imventory count sheets and warehouse location maps. The auditor established the following information relating to the inventory count and product lines of JBU. - There was no product movernent on the day of the count - The loading dock is part of Warehouse A for the purposes of the count. - All product lines within each storage area have been identified on the warehouse maps. - The warehouse map is reflective of the warehouse on the day of the count. - Inventory values in the perpetual irventory listing are based on the most recent purchase price. - Materiality for year-end audit $8,000 - Performance materiality. $5,000 Email from controller From controler@ibuco com To. Audiongcpafirm com Date January 11 year 5 Subject Re: Returns Avditor, Please see my response to your question inine below. Also, it should be noted that on cioser look, there is an issue wth the physical counts of the 5mm widgets. The perpetual records are correct. This has been validated by your assocate. Lasty, it tooks lke the perpetual inventory listing includes 750 unds of SKU 267 -1 that should have been moved out of the perpetual inventory system and into the consigned inventory account. Thanks, Controlier From: Auditor excpafirm com To controller(i) buco com Date; January 10, year 5 Subject Returns H. Can you please tel me whether the tems in the returns area have been mcluded in the count? [Controler) Yes, the counts are correct and retums have been included in the counts However, they would not yet have been processed in the perpefuat inventory system. Thanks. Auditor Supplier Report: Widget-Wiz Co. SKU 267.3 On September 25 , year 4, JBU acquired 100 units of SKU 267.3 with a unit price of $7.99. subsequent to this acquisition, JBU sold a total of 25 units of 267.3 to third parties for $11.99, and utilized 70 units of the product in the manufacture of equipment being held for sale in warehouse C. SKU 267.5 The company has not made a purchase of skU 267.5 subsequent to february, year 3 . In prior years, 38U had a regular customer for this product line but during year 3 , this customer became insolvent. SKU 267-1 In March, year 4, J8U purchased 5,000 units of SKU 267.1. Half of the units were used in the manufacture of equipment that has subsequently been sold. A further 30% of the units were sold to third parties during year 4 and 5% of the units are in ending inventory. The remaining 15% of the units were provided to a customer on a consignment basis on December 31, year 4 . These units were sold by the customer on January 3 , year 5 . SKU2674 In December, year 3 , the company acquired 10,000 units of $KU 267.4 at a price of $1.56 per unit. During year 4 , the company sold 5,898 units of the product to third parties. The last sale was made in November, year 4 , with shipment that same month. Warehouse Map Inewtery ceun ghests ceasilet atier that these aseve. Based on the work performed above, form a conclusion on the ending inventory balance. Assume that the auditor performed any follow-up procedures to confirm the initial reasons for the differences identified and therefore any adjustments required are accurate and there are no other adjustments to consider other than those above