Answered step by step

Verified Expert Solution

Question

1 Approved Answer

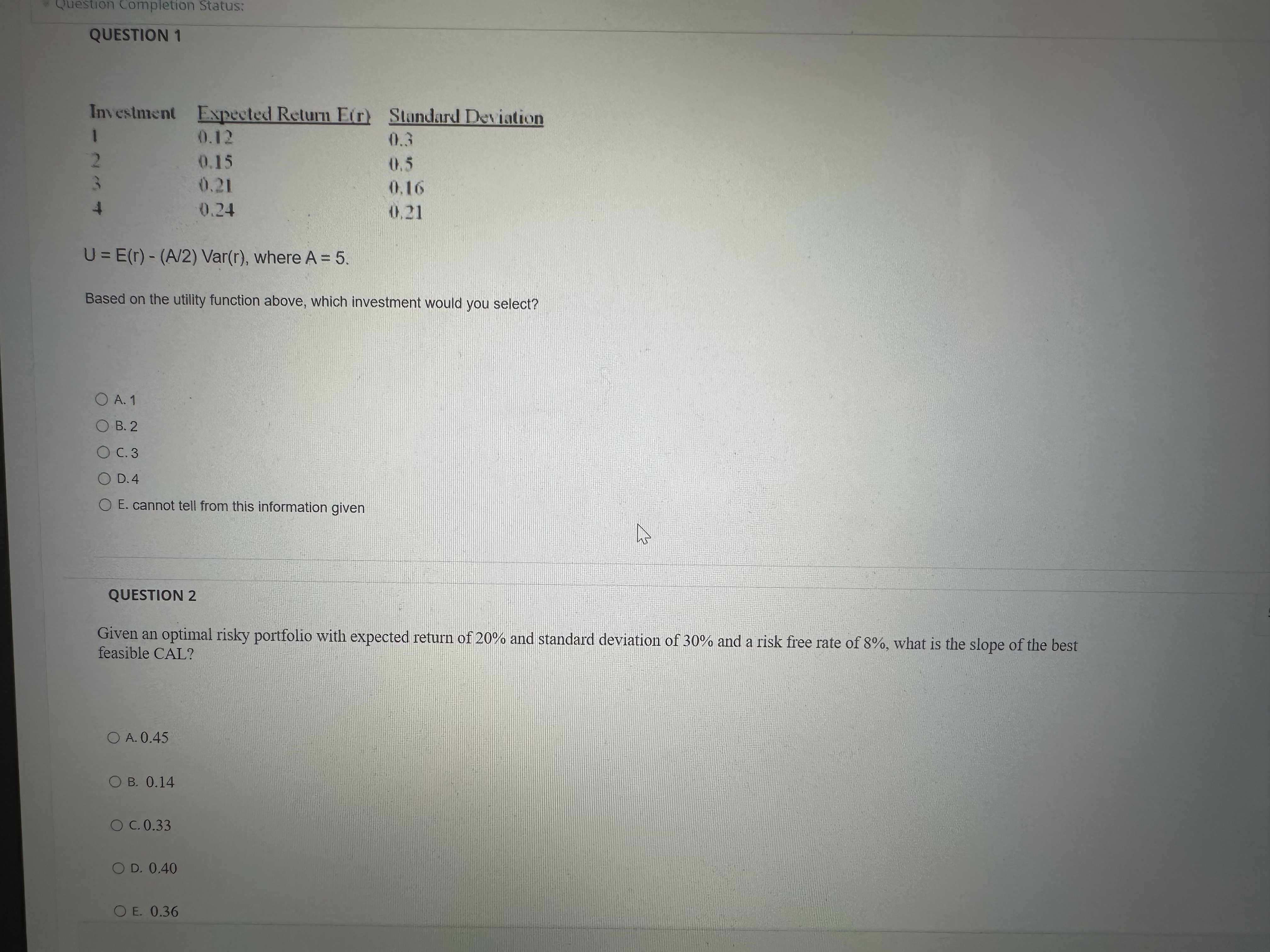

Guestion Completion status: QUESTION 1 table [ [ Investment , Expected Return E ( r ) , Standard Deviation ] , [ 1 ,

Guestion Completion status:

QUESTION

tableInvestmentExpected Return ErStandard Deviation

where

Based on the utility function above, which investment would you select?

A

B

C

D

E cannot tell from this information given

QUESTION

Given an optimal risky portfolio with expected return of and standard deviation of and a risk free rate of what is the slope of the best feasible CAL?

A

B

c

D

E

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Emerald Handbook On Cryptoassets Investment Opportunities And Challenges

Authors: H. Kent Baker, Hugo Benedetti, Ehsan Nikbakht, Sean Stein Smith

1st Edition

1804553212, 978-1804553213