Question

h 7 1 Adapted from CIMA Stage 2 Cost IM7.4 Intermediate: Calculation of overhead absorption rates and an explanation of the differences in profits. A

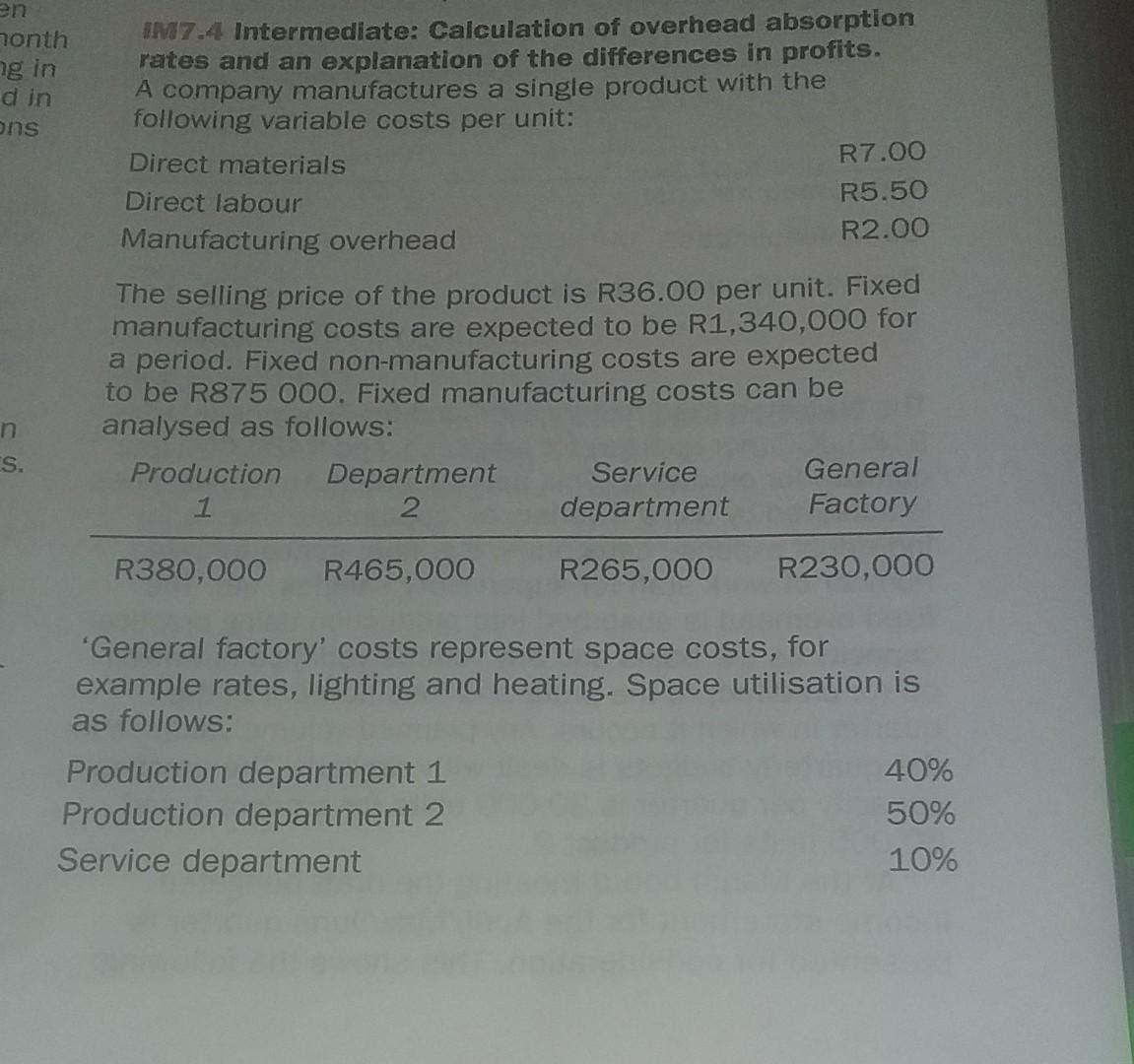

h 7 1 Adapted from CIMA Stage 2 Cost IM7.4 Intermediate: Calculation of overhead absorption rates and an explanation of the differences in profits. A company manufactures a single product with the following variable costs per unit: Direct materials Direct labour Manufacturing overhead The selling price of the product is R36.00 per unit. Fixed manufacturing costs are expected to be R1,340,000 for a period. Fixed non-manufacturing costs are expected to be R875 000. Fixed manufacturing costs can be analysed as follows: Production Department 1 2 R380,000 R465,000 R7.00 R5.50 R2.00 Service department R265,000 Production department 1 Production department 2

Service department General Factory R230,000 'General factory' costs represent space costs, for example rates, lighting and heating. Space utilisation is as follows: 40% 50% 10%

The selling price of the product is R36.00 per unit. Fixed manufacturing costs are expected to be R1,340,000 for a period. Fixed non-manufacturing costs are expected to be R875 000. Fixed manufacturing costs can be analysed as follows: 'General factory' costs represent space costs, for example rates, lighting and heating. Space utilisation is as followsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Cybersecurity Body Of Knowledge The ACM IEEE AIS IFIP Recommendations For A Complete Curriculum In Cybersecurity Internal Audit And IT Audit

Authors: Daniel Shoemaker, Anne Kohnke, Ken Sigler

1st Edition

1032400218, 978-1032400211