Question

H A R V A R D B U S I N E S S S C HO O L 9-1 05-005 REV: APRIL 18,

H A R V A R D B U S I N E S S S C HO O L 9-1 05-005 REV: APRIL 18, 2005 DENNIS CAMPBELL SUSAN KULP TOYS The decline in margins on our popular Geoffrey doll product has become intolerable. Increasing production costs have dropped our pretax margin to less than 10%, far below our historical 25% margins. If we are going to increase our margins, we need to consider drastically shifting our production towards specialty dolls that are earning a large premium in price over our standard doll line. Robert Parker, President, G.G. Toys

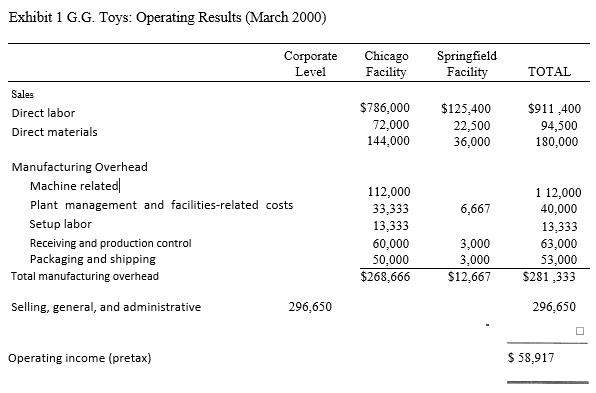

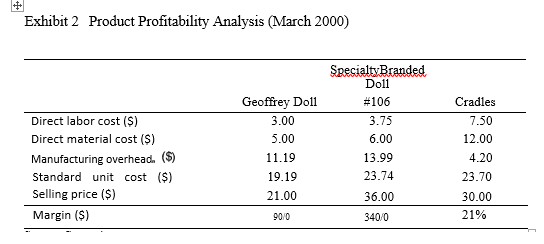

BACKGROUND- Robert Parker, president of G.G. Toys, was discussing last month's operating results with Audrey Hausner, G.G.'s controller, and David Morehouse, G.G.'s manufacturing manager. The meeting was taking place in an atmosphere tinged with apprehension because margins on their most popular product, the "Geoffrey doll," had been declining rapidly in the last few years due to rising production costs (summary operating results for the previous month, March 2000, are shown in Exhibits 1 and 2). Parker saw no choice but to shift the company's product mix towards specialty dolls that carried a high price premium, and thus, a 34% margin.

G.G. Toys was a leading supplier of high-quality dolls to retail toy stores throughout the U.S. The company had started with a unique design for molding highly durable dolls using vinyl and resin materials. G.G. quickly established a loyal customer base among retailers because of the high quality and popularity of its manufactured dolls. It soon established a major presence in the market with its high-volume Geoffrey doll product line. The company operated two separate plants. The Chicago plant was used for the production of various dolls. The Springfield plant was used solely to assemble doll cradles to complement the company's dolls.

The Geoffrey doll was designed to be a replica of an infant boy or girl clothed in a simple pajama outfit with movable acrylic eyelids and jointed, movable arms and legs. Boy and girl versions of the doll were produced to almost identical specifications with minor differences in the face and length of hair. The early popularity of the Geoffrey doll allowed the company to produce both versions of the doll in high volumes using the same production process. While prices for the standard Geoffrey doll line remained steady, rising costs of production had eroded gross margins in this product line from well over 25% to 9%.

Competition from other doll manufacturers and demand from retailers prompted G.G. Toys to complement its existing product line with highly specialized versions of the Geoffrey doll that retailers could brand as their own line. G.G. Toys began producing customized dolls for retailers under their "specialty-branded" product line. Under this product line, retailers placed orders for dolls with their own customized specifications for hair color, skin tone, and pajama style to reflect the tastes of the customer segments they served.

CHICAGO MANUFACTURING PLANT- G.G. Toy's production process for dolls started with the purchase of raw materials, such as vinyl and resin for the doll bodies and wool and other fibers for doll hair and pajamas, from several suppliers. In its modern Chicago manufacturing facility, the company machine-molded the vinyl and resin into doll bodies, hand- and machine-sewed the various fibers into pajamas and hair for the dolls, and assembled the final product.

Doll bodies for the specialty-branded line were produced to the same specifications as the standard Geoffrey doll in terms of shape and size. However, the pajama outfit of this line was often more ornate than the simple pajama outfit of the standard Geoffrey doll. Thus, more specialized material cuts and hand assembly were required. Also, because of the customized nature of the specialty-branded product, there was much more variety in skin tone, eye color, hair color, and hair length for these dolls than there was for the standard Geoffrey doll.

The same equipment and labor were used for all doll product lines, and production runs were scheduled to match customer shipping requirements. Products were packed and shipped as completed.

The Chicago plant had fallen short on production in the current year. While it had planned for production of 24,900 units, only 24,000 units were produced. However, overall revenue during March was $786,000 (see Exhibit 1), which exceeded forecasted revenue of $765,000. Although happy with the over-performance, plant management did not know how to explain these conflicting results.

SPRINGFIELD ASSEMBLY PLANT- Cradles were assembled in the company's small Springfield assembly plant. The plant produced only one model of the cradle and purchased all of the product's finished components from several local manufacturers. The cradles were assembled from these finished components completely by hand. Cradles contained several components ranging from the cradle bed and rocking cradle legs to a small speaker that played preset music. To ensure the quality of the finished components coming from G.G.'s multiple suppliers, assembly line workers tested the components frequently during the assembly process.

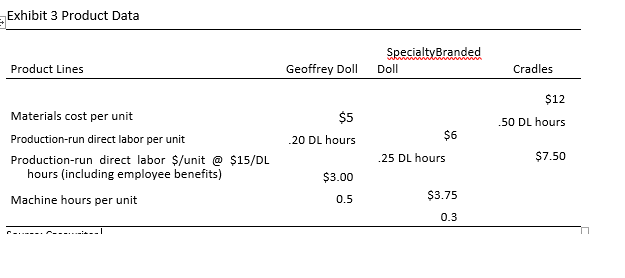

CURRENT COST SYSTEMS- G.G.'s cost accounting system charged each unit of product for direct material and direct labor. Material cost was based on the prices paid for raw materials under annual purchasing agreements. Labor rates, including fringe benefits, were $15 per hour and were charged to product based on the standard run times for each product (see Exhibit 3). Overhead costs in the Chicago plant were allocated to Geoffrey dolls and specialty-branded dolls as a percentage of production-run direct labor cost. The Springfield plant also used production-run direct labor cost to allocate its overhead costs to the production of cradles. The company elected not to allocate selling, general, and administrative costs to products.

INTERNAL COST STUDY- G.G. Toys had recently commissioned a small internal team to study its overhead costs in both plants. The study revealed the following information:

1. Workers in the Chicago facility often operated several machines simultaneously once they were set up. Thus, machine-related expenses might relate more to the machine hours of a product than to its production-run labor hours.

2. A setup was performed in the Chicago facility each time a modification to the dolls was made. For example, to switch from a batch of girl dolls to a batch of boy dolls, a setup was required. Additionally, each time a specialty-branded doll was produced, a separate setup was required to process the raw materials to the required specifications. As the cradles were assembled entirely by hand, there were no setups in the Springfield plant.

3. For each production run, people in the receiving and production-control departrnents of the Chicago plant ordered, processed, inspected, and moved each batch of raw materials. This work required the same amount of time regardless of the production run length. The Springfield plant received materials on a just-in-time basis and continuously inspected and moved these materials.

4. The work in the packaging and shipping areas of both plants had increased during the past couple of years as the company increased the number of customers it served. Each time products were packaged and shipped, about the same amount of work was required, regardless of the number of items in the shipment.

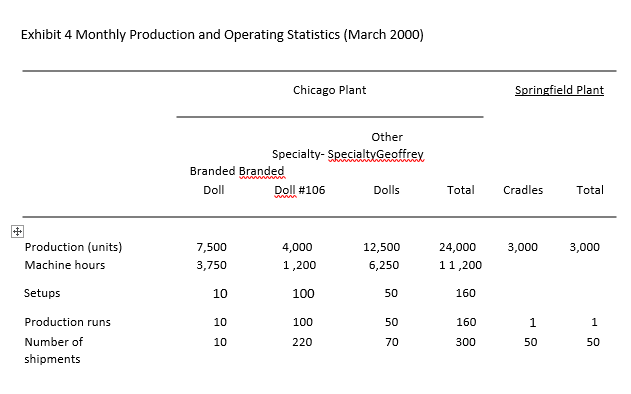

The team had collected the data shown in Exhibit 4 based on operations in March 2000 and felt that this month was typical of ongoing operations with the plant producing at practical capacity. The team decided that plant management and facilities-related costs should continue to be allocated to products in the same way they had been under the old system, as a percentage of production-run direct labor cost.

The team collected data on the standard Geoffrey doll, the specialty-branded doll #106, and the cradle (Exhibits 24). Specialty-branded doll #106 had been ordered by several of G.G. Toy's largest customers and made an extremely successful debut in the marketplace. While the Chicago plant produced many different specialty-branded doll models, this particular doll concerned management. Because each retailer required slight alterations to the doll's clothing (e.g., retailer logo on pajamas), a new setup and production run were required each time the clothing design was changed. Because the doll was fairly new, retailers were conservative in their ordering patterns; most ordered fewer units more frequently. Due to these concerns, G.G. management wanted to assess the profitability of the specialty-branded doll #106.

CURRENT SITUATION- Because of their high margins, Parker was willing to accept many orders for specialty-branded dolls even if this meant that the company had to lower production of the standard Geoffrey doll. In the meeting, Parker would discuss this issue with Hausner and Morehouse. Additionally, Parker wanted to discuss two additional product lines.

G.G. Toys had decided to produce holiday reindeer dolls in the Chicago plant during July, August, and September. The Chicago plant expanded its production capacity (i.e., machines and leased space) and reserved the additional capacity for production of the holiday reindeer. Thus, this capacity would sit idle from October through June. Parker was unsure about how this excess capacity would affect the results of the internal cost study in the Chicago plant and overall plant performance.

Additionally, G.G. Toys was considering producing a hand-made "Romaine Patch" doll. This doll would be a simply constructed doll made of a soft-cloth body stuffed with the same soft-cloth material. Because of the simple construction of the doll, G.G. Toys felt that it would be low cost to produce but was confused by its estimated negative contribution margin. Based on management estimates, the expected sales price per doll was $8.00, the expected direct labor cost per doll was $3.00, and the expected direct material cost per doll was $6.00. The latter material cost was based on two facts: new material cost the Chicago plant $2 per yard, and each Romaine Patch doll would use three yards of material. This doll would be produced in the Chicago plant, and G.G. felt that it could produce all units of this doll by hand, using the scrap material from production of all doll pajamas at the Chicago plant. Currently, the production of pajamas resulted in significant amounts of scrap material This material was disposed of at no additional cost to G.G. Toys. Approximately 20% of the material ordered for the doll pajamas resulted in scrap; all of this material would be used in Romaine Patch production.

QUESTIONS-

1. Do you recommend that G.G. Toys change its existing cost system in the Chicago plant? In the Springfield plant? Why or why not?

2. Calculate the cost of a Geoffrey doll, the specialty-branded doll #106, and a cradle using the cost study conclusions.

3. Compare and contrast the profitability of each doll under the new and old systems. Based on your recomputed product costs, what actions would you recommend the company consider to enhance its profitability? What additional information would you like to have to make these recommendations?

4. How should G.G. Toys account for the excess capacity created to produce the holiday reindeer dolls? Qualitatively, how will this impact your calculated cost of the Geoffrey doll and the specialty-branded dolls in question number 2? Explain your method and its impact. (Answer qualitatively. Do not recompute any of your product costs from question 2.)

5. What explains the difference between forecasted and actual revenue for the Chicago plant during March of 2000? What other information would you collect to help explain this difference?

6. Do you recommend G.G. Toys produce the Romaine Patch doll? Why or why not? (Ignore manufacturing overhead costs including packaging, shipping, and receiving and production control.)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: Ray Garrison, Eric Noreen and Peter Brewer

14th edition

978-007811100, 78111005, 978-0078111006