Answered step by step

Verified Expert Solution

Question

1 Approved Answer

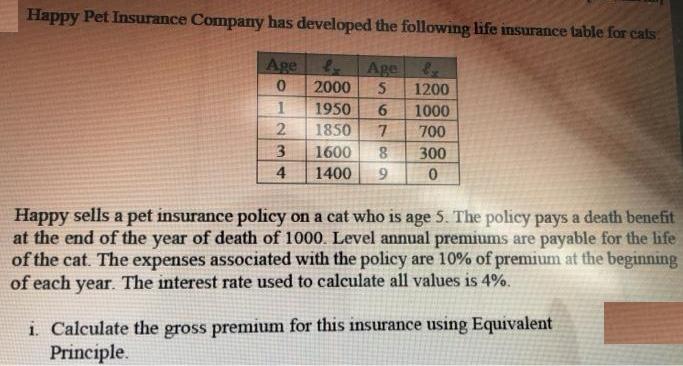

Happy Pet Insurance Company has developed the following life insurance table for cats Age Age 2000 5 1200 1 1950 1000 1850 7 700

Happy Pet Insurance Company has developed the following life insurance table for cats Age Age 2000 5 1200 1 1950 1000 1850 7 700 3. 1600 4 300 1400 9. Happy sells a pet insurance policy on a cat who is age 5. The policy pays a death benefit at the end of the year of death of 1000. Level annual premiums are payable for the life of the cat. The expenses associated with the policy are 10% of premium at the beginning of each year. The interest rate used to calculate all values is 4%. i. Calculate the gross premium for this insurance using Equivalent Principle. 11. Calculate the loss that Happy will incur if the cat dies in the second year if the gross premium is calculated using the Equivalence Principle. 111. Happy decides to charge a gross premium so that the loss will be zero if the cat dies in the second year. Determine the gross premium that Happy decides to charge.

Step by Step Solution

★★★★★

3.41 Rating (151 Votes )

There are 3 Steps involved in it

Step: 1

Stept caleulate the gross premium for this insurance using the equivalence p...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Financial Management

Authors: James R Mcguigan, R Charles Moyer, William J Kretlow

10th Edition

978-0324289114, 0324289111