Answered step by step

Verified Expert Solution

Question

1 Approved Answer

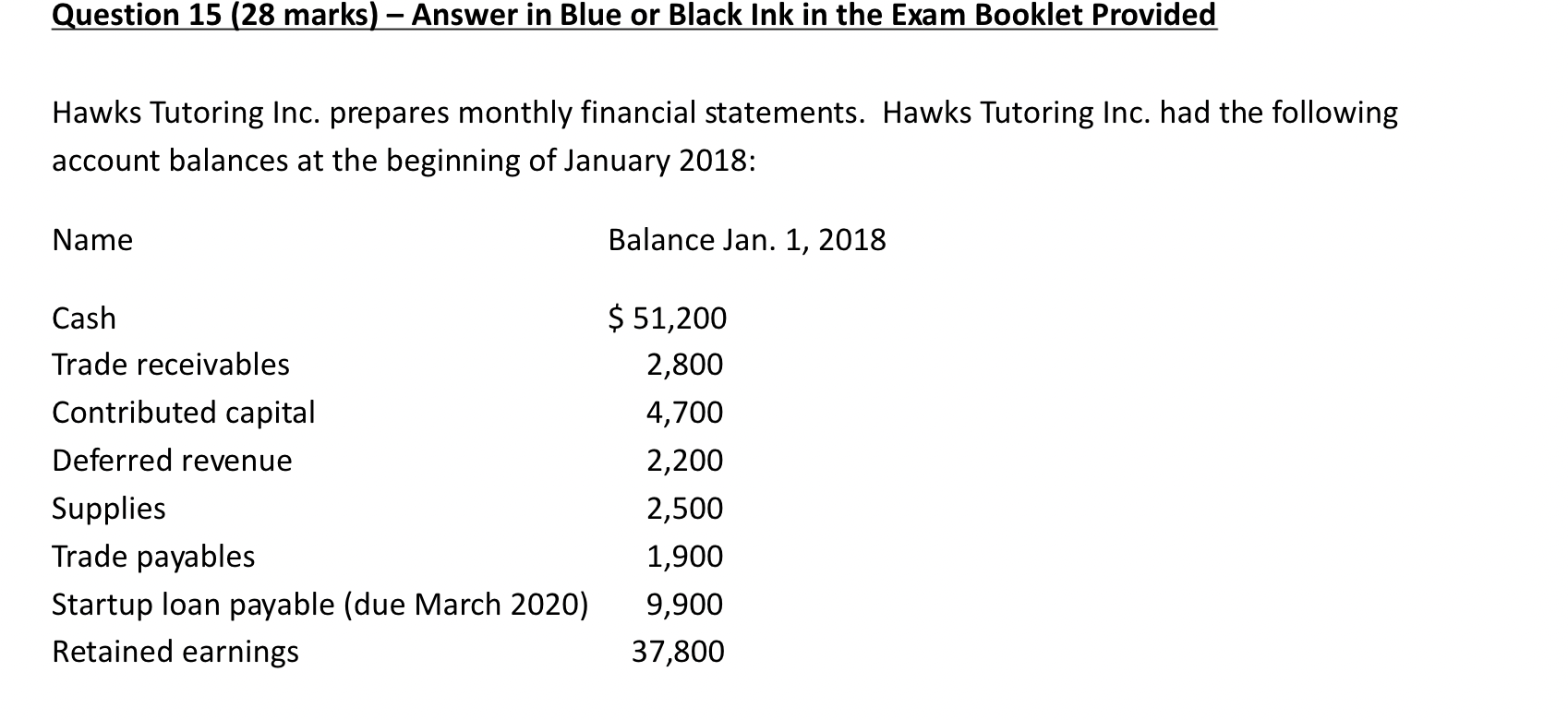

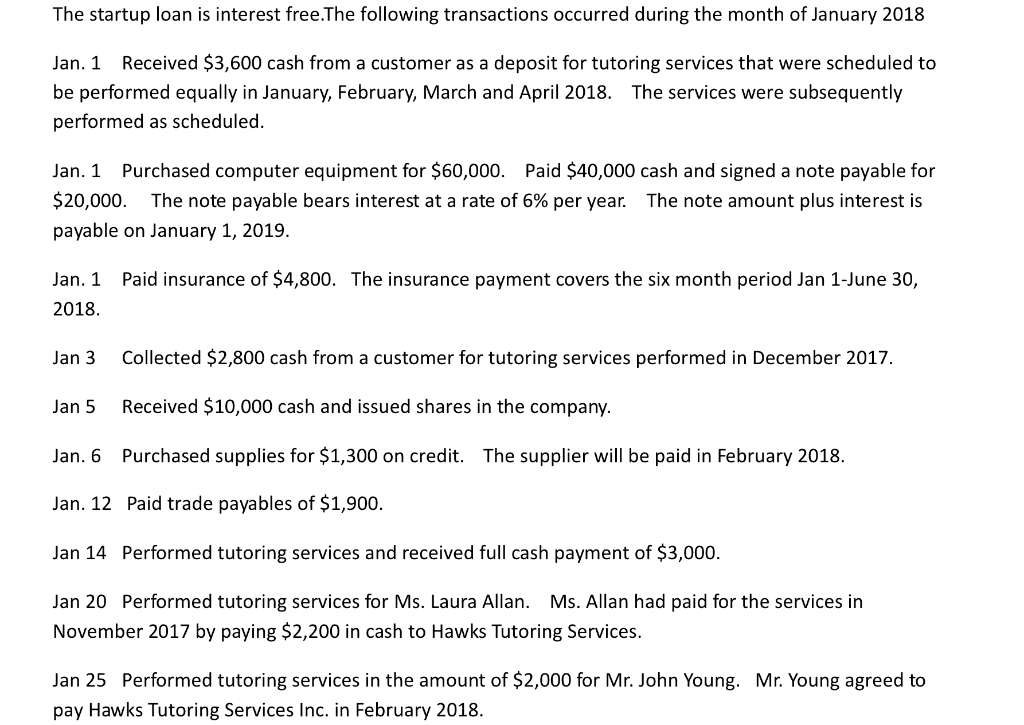

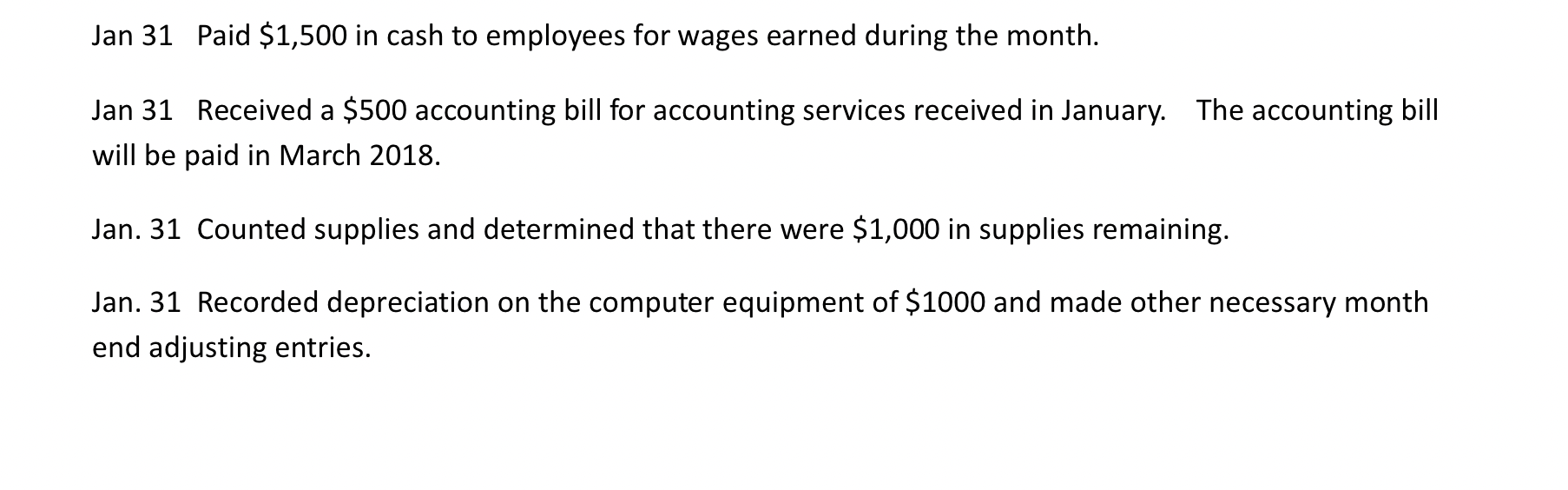

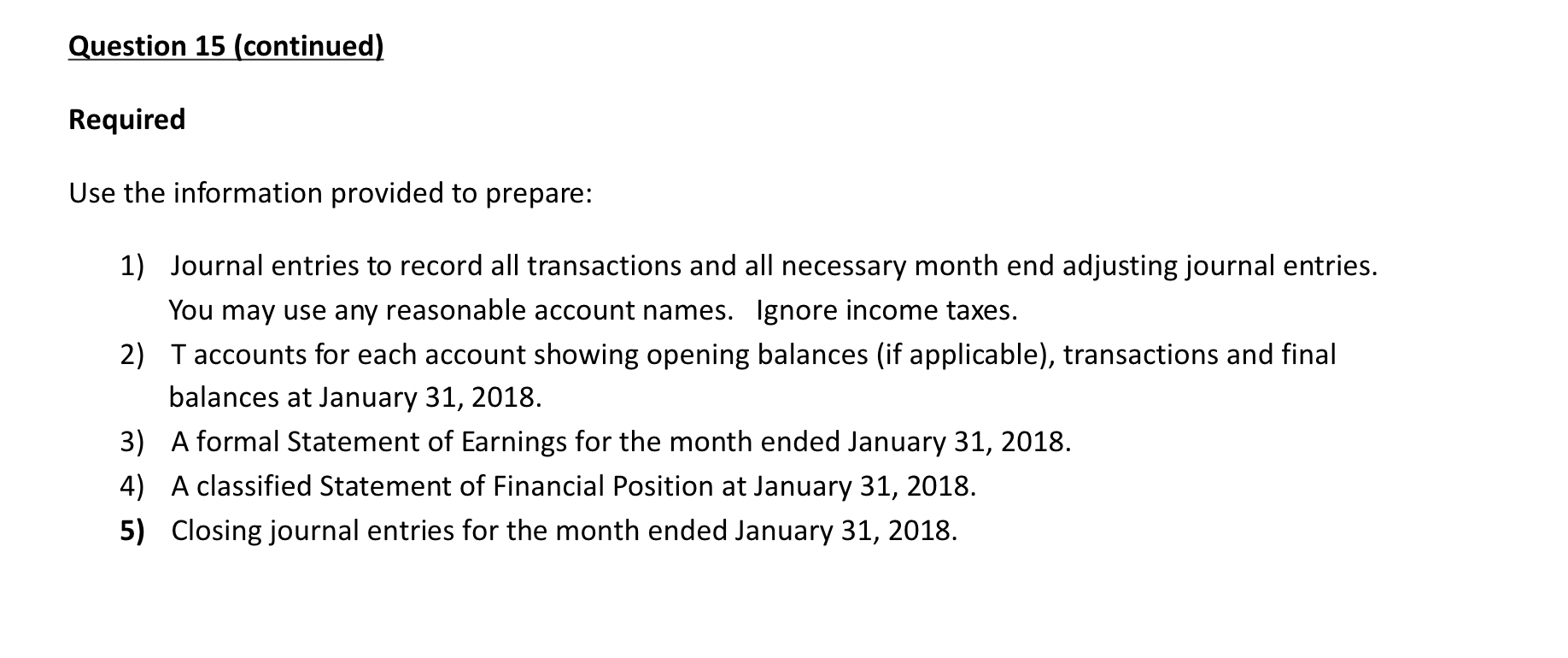

Hawks Tutoring Inc. prepares monthly financial statements. Hawks Tutoring Inc. had the following account balances at the beginning of January 2018: The startup loan is

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting

Authors: Carl s. warren, James m. reeve, Philip e. fess

21st Edition

978-0324400205, 324225016, 324188005, 324400209, 9780324225013, 978-0324188004