Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Heads Up Company was started several years ago by two hockey instructors. The company's comparative balance sheets and income statement follow, along with additional information.

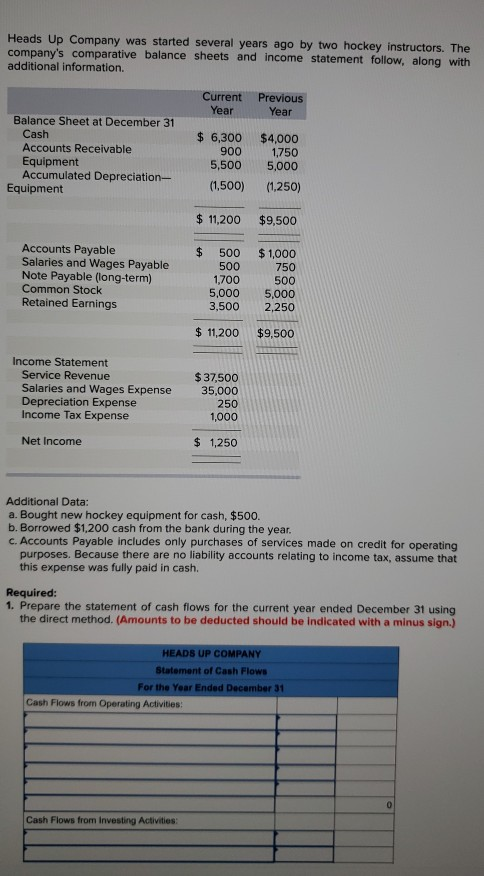

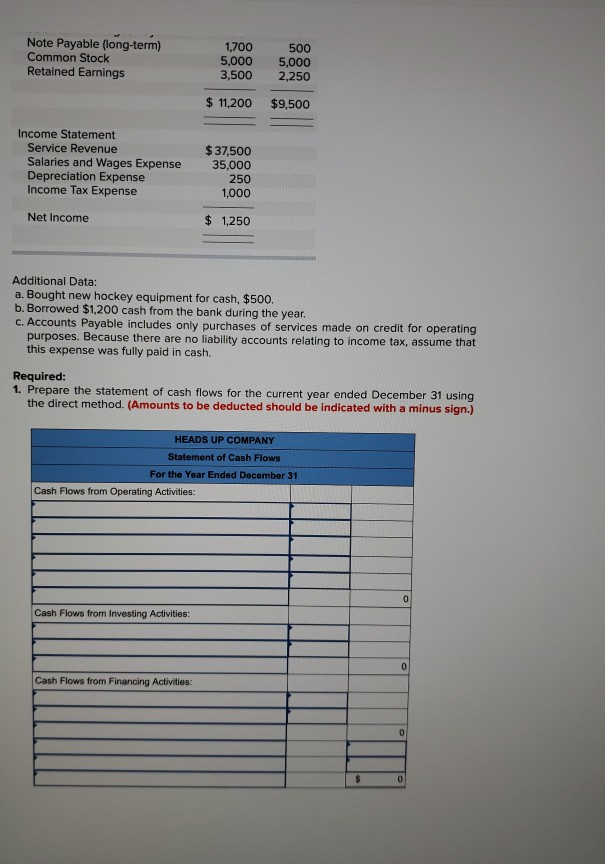

Heads Up Company was started several years ago by two hockey instructors. The company's comparative balance sheets and income statement follow, along with additional information. Current Previous Year Year Balance Sheet at December 31 Cash Accounts Receivable Equipment Accumulated Depreciation- 6,300 $4,000 900 1,750 5,500 5,000 Equipment (1,500) (1,250) $11,200 $9,500 Accounts Payable Salaries and Wages Payable Note Payable (long-term) Common Stock Retained Earnings $ 500 $1,000 500 750 1.700 500 5,000 5,000 3,500 2,250 11,200 $9,500 Income Statement Service Revenue Salaries and Wages Expense Depreciation Expense Income Tax Expense $37,500 35,000 Net Income 1,250 Additional Data a. Bought new hockey equipment for cash, $500. b. Borrowed $1,200 cash from the bank during the year c. Accounts Payable includes only purchases of services made on credit for operating purposes. Because there are no liability accounts relating to income tax, assume that this expense was fully paid in cash. Required: 1. Prepare the statement of cash flows for the current year ended December 31 using the direct method. (Amounts to be deducted should be indicated with a minus sign.) HEADS UP COMPANY Statement of Cash Flows or the Year Ended December 3 Cash Flows from Operating Activities: Cash Flows from Investing Activities Note Payable (long-term) Common Stock 1,700 500 5,000 5,000 3,500 2,250 Retained Earnings $11,200 $9,500 Income Statement Service Revenue Salaries and Wages Expense Depreciation Expense Income Tax Expense $37,500 35,000 250 1,000 Net Income 1,250 Additional Data: a. Bought new hockey equipment for cash, $500. b. Borrowed $1,200 cash from the bank during the year. c. Accounts Payable includes only purchases of services made on credit for operating purposes. Because there are no liability accounts relating to income tax, assume that this expense was fully paid in cash. Required 1. Prepare the statement of cash flows for the current year ended December 31 using the direct method. (Amounts to be deducted should be indicated with a minus sign.) HEADS UP COMPANY Statement of Cash Flows For the Year Ended December 31 Cash Flows from Operating Activities: Cash Flows from Investing Activities: Cash Flows from Financing Activities

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Modern Accounting And Auditing Forms

Authors: Wendell

1st Edition

0882621769, 978-0882621760