Answered step by step

Verified Expert Solution

Question

1 Approved Answer

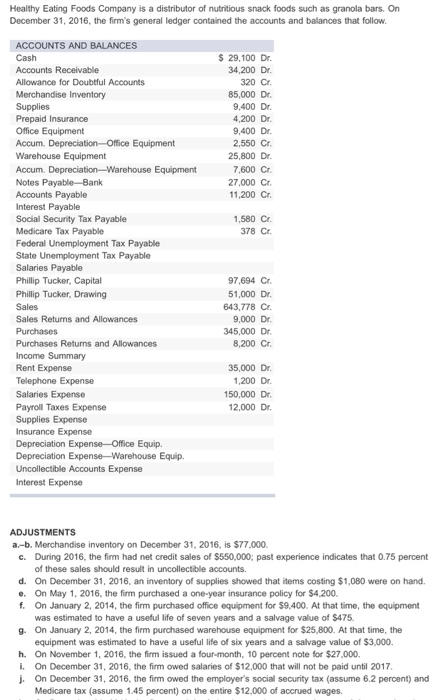

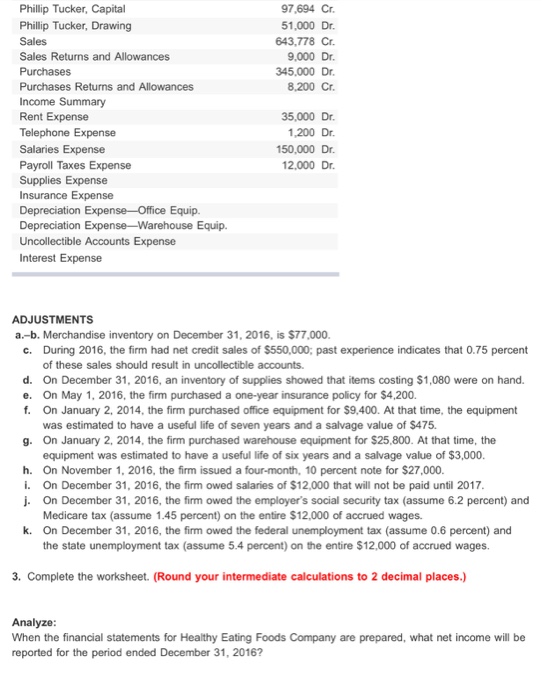

Healthy Eating Foods Company is a distributor of nutritious snack foods such as granola bars. On December 31, 2016, the firm's general ledger contained the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Property Companies An Industry Accounting And Auditing Guide

Authors: Accountancy Books

1st Edition

1853558079, 978-1853558078