Question

Hello, Appreciate if you can help me to find out the solution for the following problem. Denote by V(t) V ( t ) the replicating

Hello,

Appreciate if you can help me to find out the solution for the following problem.

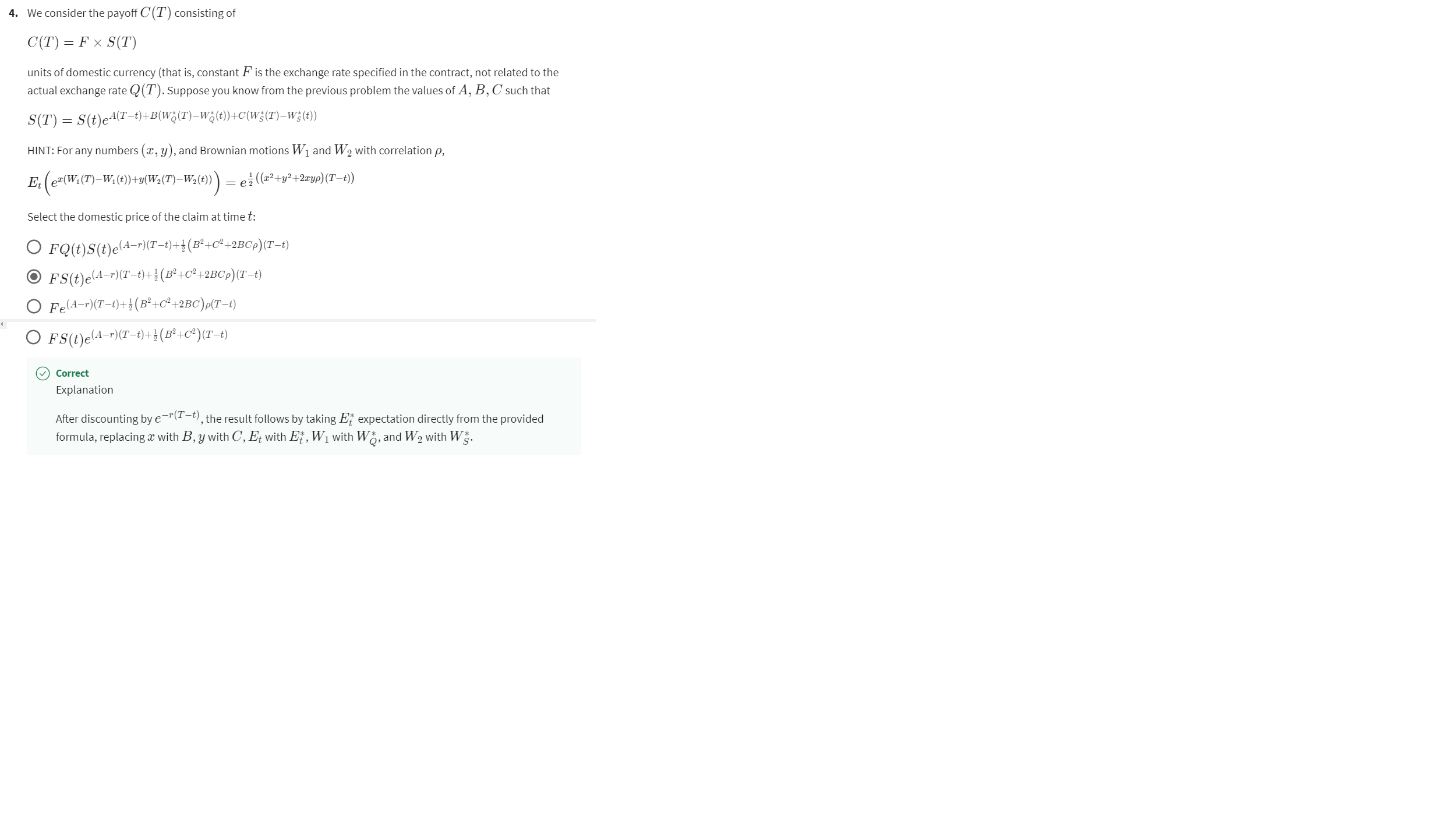

Denote by V(t)V(t) the replicating portfolio of the payoff in problem number 4 (in this unit's practice problems and problem set) that does replication by investing the domestic currency in the foreign stock, the foreign bank account and the domestic bank account. Can you say, in terms of V(t)V(t), how much the replicating portfolio invests in each of these three assets, in each of the above two problems?

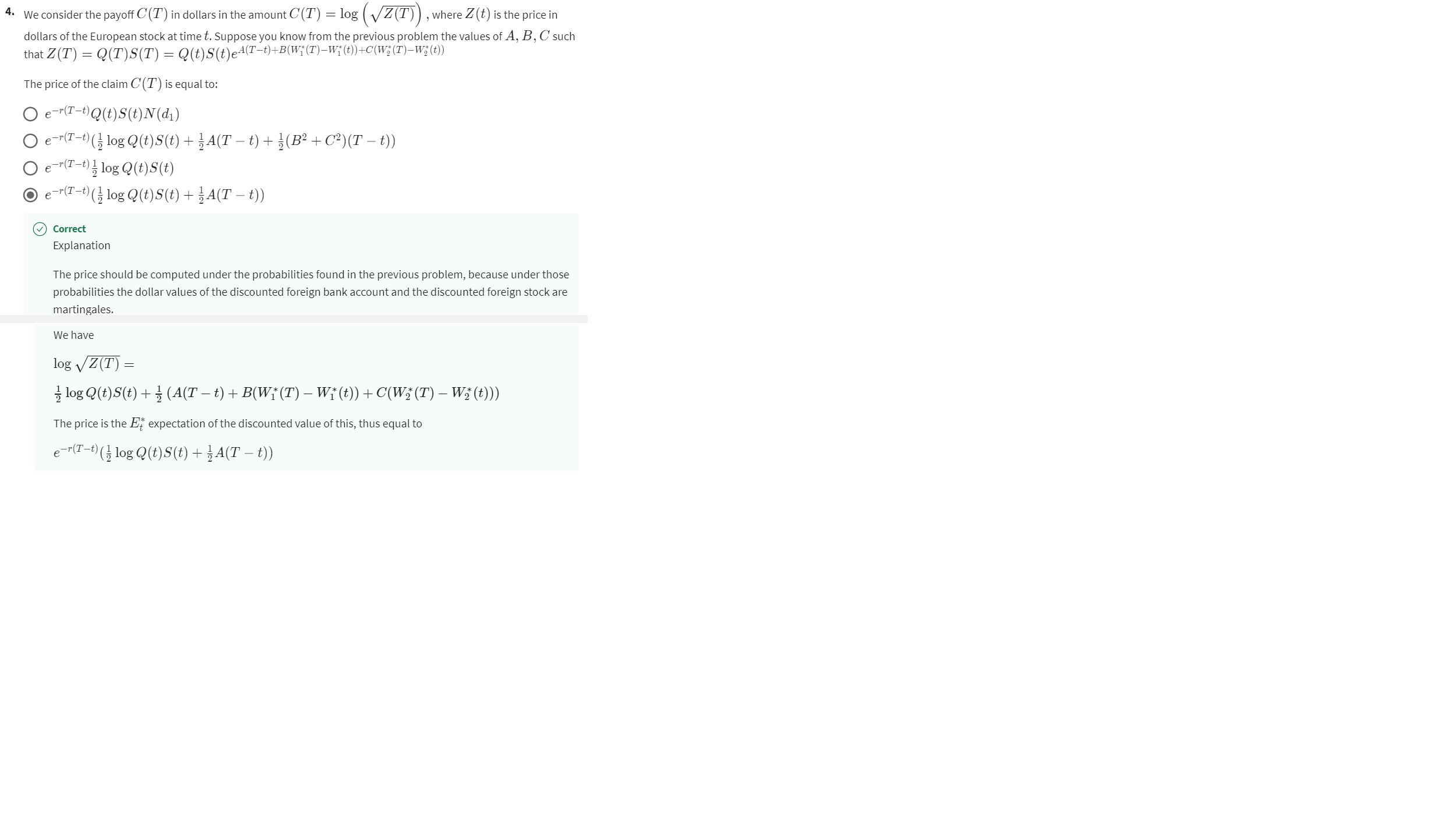

I am attaching the problem 4 of unit's practice problemsand its solution in UnitPracticeProblemAndSol.png

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Infinity Properads And Infinity Wheeled Properads

Authors: Philip Hackney, Marcy Robertson, Donald Yau

1st Edition

3319205471, 9783319205472