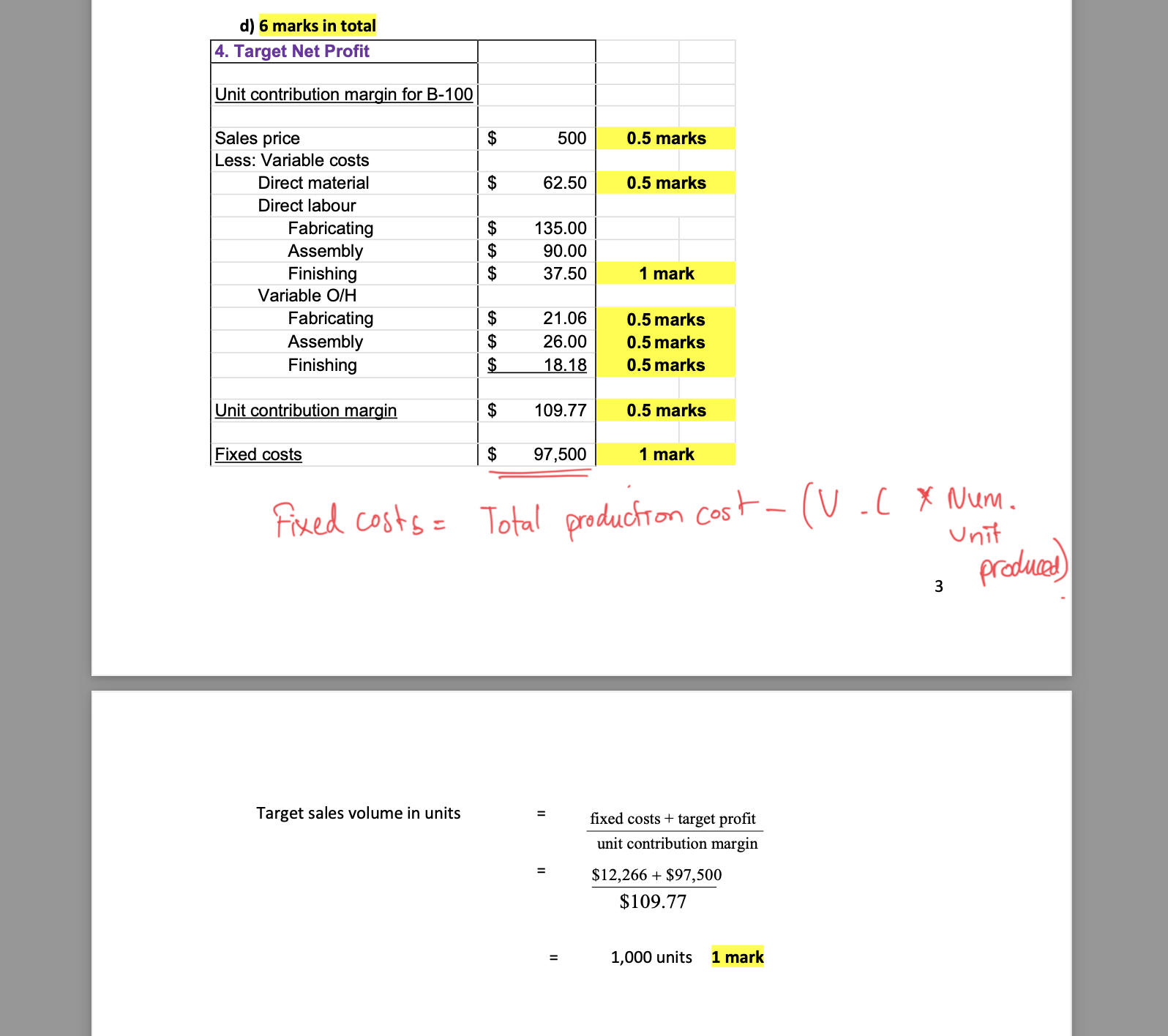

Hello Experts! I'm stuck on how they can get the fixed cost in Section D below. Here is the question and answer. Please help explain

Hello Experts! I'm stuck on how they can get the fixed cost in Section D below. Here is the question and answer. Please help explain me how they can get the fixed cost to calculate the target volume!

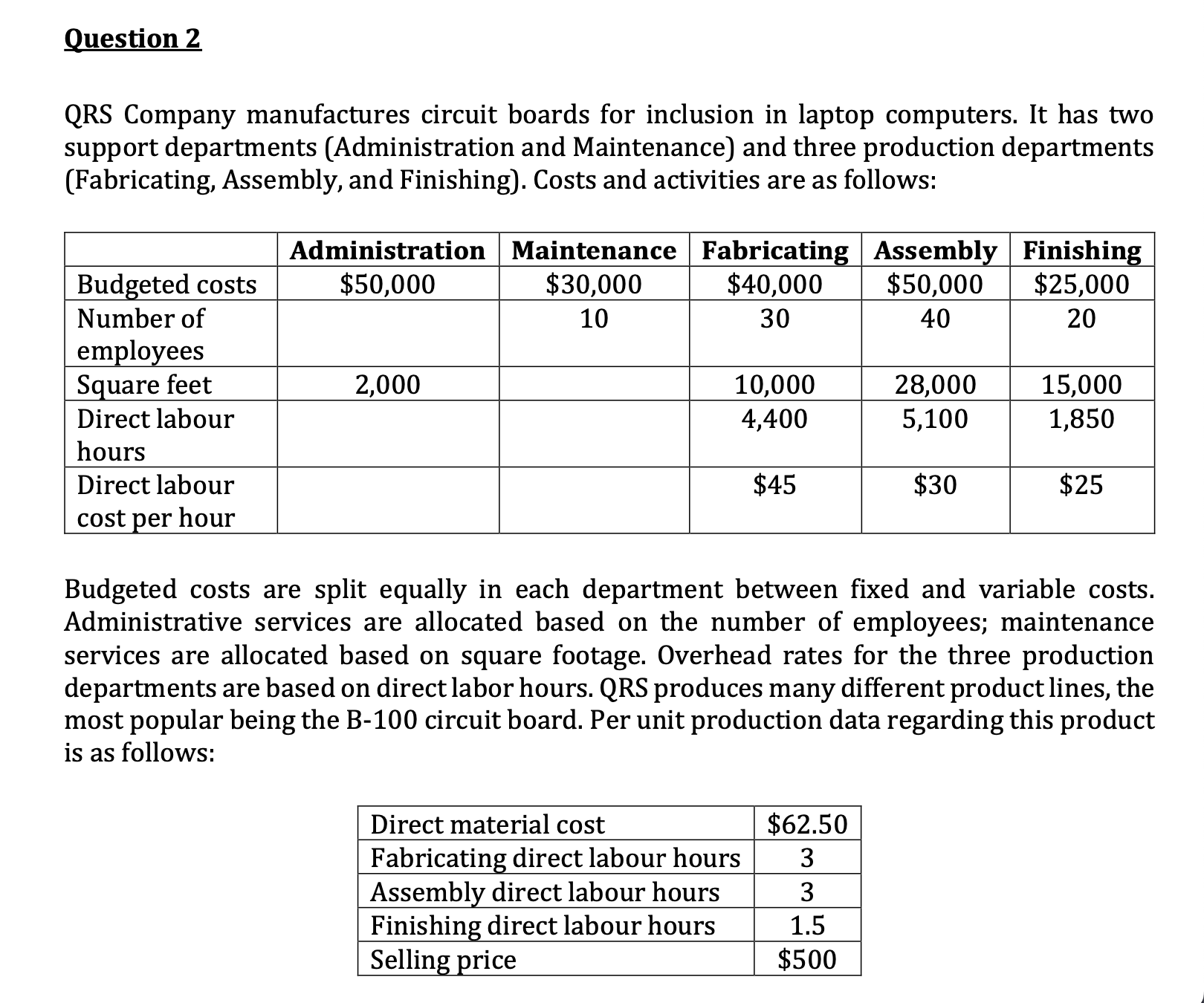

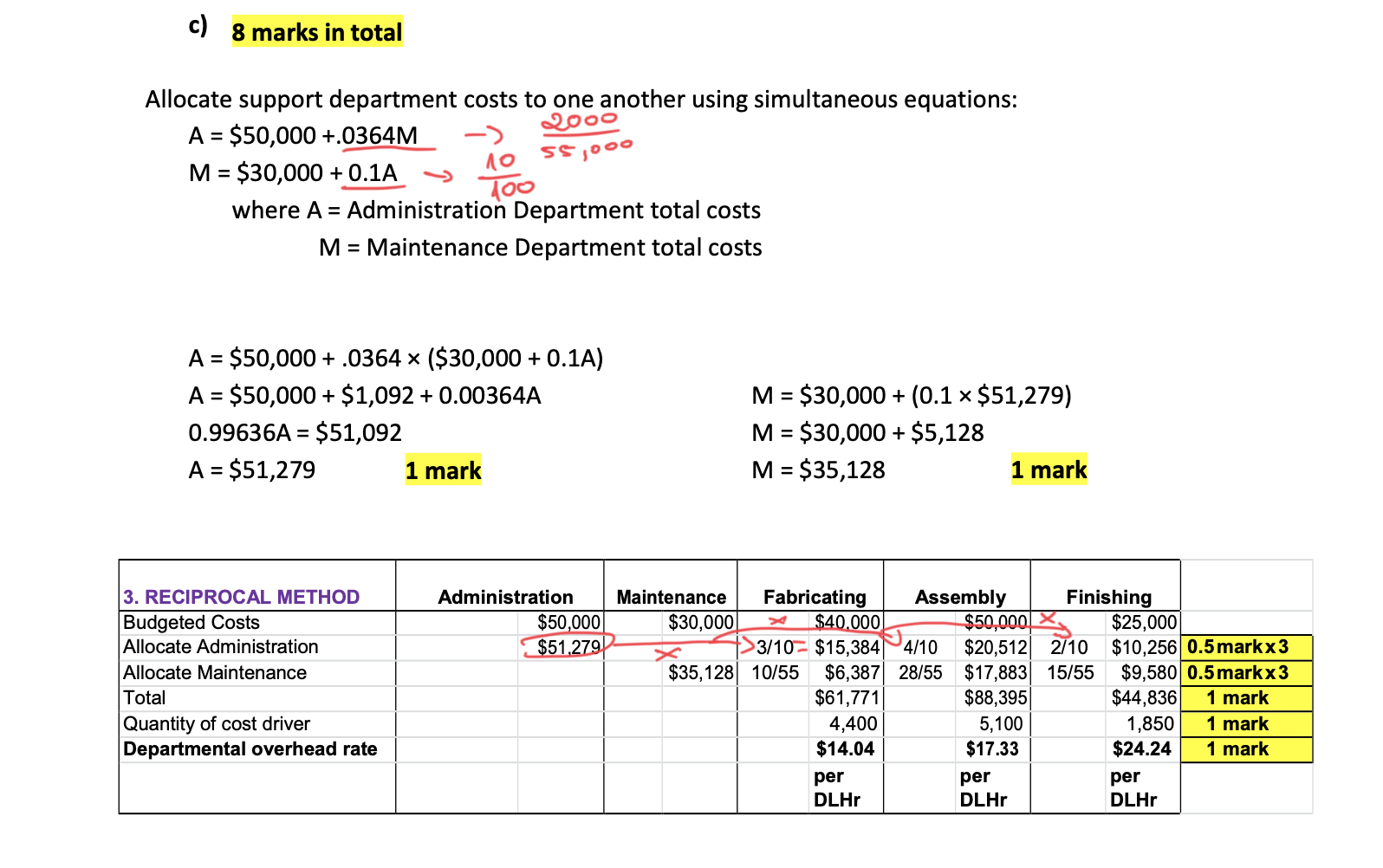

Question 2 QRS Company manufactures circuit boards for inclusion in laptop computers. It has two support departments (Administration and Maintenance) and three production departments (Fabricating, Assembly, and Finishing]. Costs and activities are as follows: Budgeted costs Number of employees S - uare feet Direct labour hours Direct labour cost - er hour Budgeted costs are split equally in each department between fixed and variable costs. Administrative services are allocated based on the number of employees; maintenance services are allocated based on square footage. Overhead rates for the three production departments are based on direct labor hours. QRS produces many different product lines, the most popular being the 3-100 circuit board. Per unit production data regarding this product is as follows: Direct material cost Fabricatin - direct labour hours Assembly direct labour hours Finishin - direct labour hours Sellin_ - rice Required: a] What is the difference between a production department and a support department? Why is this distinction important in terms of allocating overhead costs? (2 marks) b] Describe how the direct and step-down methods of overhead allocation treat the interaction among support departments? (2 marks) c] Determine the overhead application rates for each production department using the reciprocal allocation method. (8 marks] (1) How many units of B-100 must QRS sell in order to make a target net profit of $12,266 for this product line? (6 marks] (2+2+8+6=18marks] c) 8 marks in total Allocate support department costs to one another using simultaneous equations: 0 A = $50,000 +.0364M -3 '2'\" _ Ito $I M$30,000+0.1A 3 75:: where A = Administration Department total costs M = Maintenance Department total costs A = $50,000 + .0364 x ($30,000 + 0.1A) A = $50,000 + $1,092 + 0.00364A M = $30,000 + (0.1 x $51,279) 0.99636A = $51,092 M = $30,000 + $5,128 A = $51,279 1 mark M = $35,128 1 mark 3. RECIPROCAL METHOD Administration Fabricating Assembly mm Budgeted Costs Allocate Administration l Allocate Maintenance l Total 1 | $51 ,771| $88,395l Quantity of cost driver 1 | 4,400 | 5,100 1 Departmental overhead rate 1 | $14.04 | $17.33 1 -$35,128| 10/55 $6, 337| 28/55 $175531 15/55 d) 6 marks in total 4. Target Net Profit Unit contribution margin for B-100 Sales price $ 500 0.5 marks Less: Variable costs Direct material $ 62.50 0.5 marks Direct labour Fabricating 135.00 Assembly 90.00 Finishing 37.50 1 mark Variable O/H Fabricating 21.06 0.5 marks Assembly 26.00 0.5 marks Finishing 18.18 0.5 marks Unit contribution margin $ 109.77 0.5 marks Fixed costs $ 97,500 1 mark Fixed costs = Total production cost - ( V . ( X Num. Unit 3 produced) Target sales volume in units = fixed costs + target profit unit contribution margin 2 $12,266 + $97,500 $109.77 = 1,000 units 1 mark

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance