Question

Hello, I know this looks like a lot but everything with out the red x or the green checks is filled out automatically ( not

Hello, I know this looks like a lot but everything with out the red x or the green checks is filled out automatically ( not the balance sheet) So obviously everything with the red x is wrong. So if you could help me with those that would be awesome. Oh and the balance sheet.

Thank you a bunch!

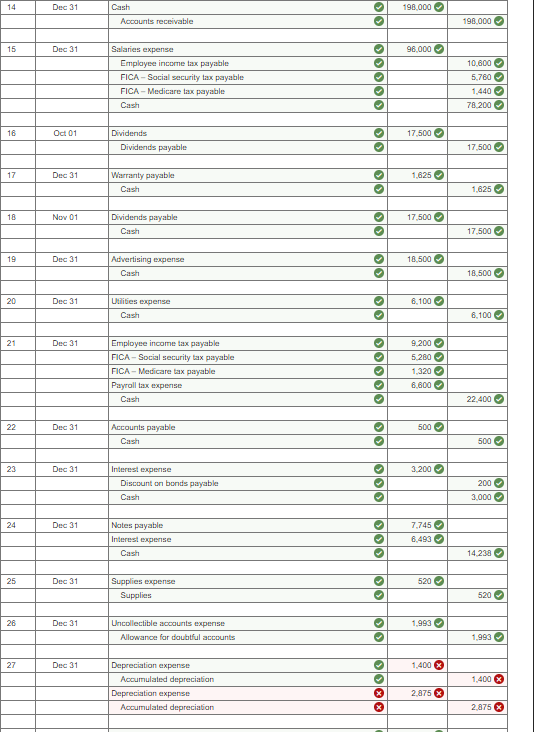

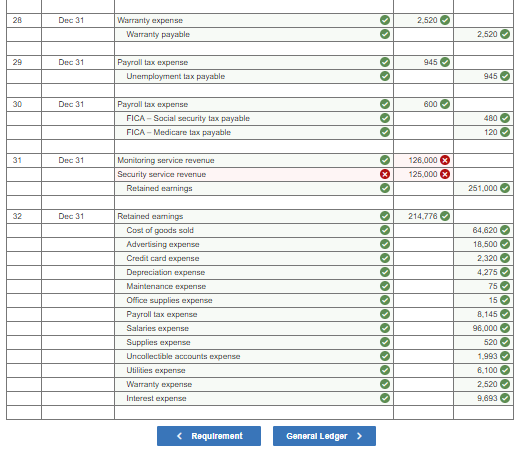

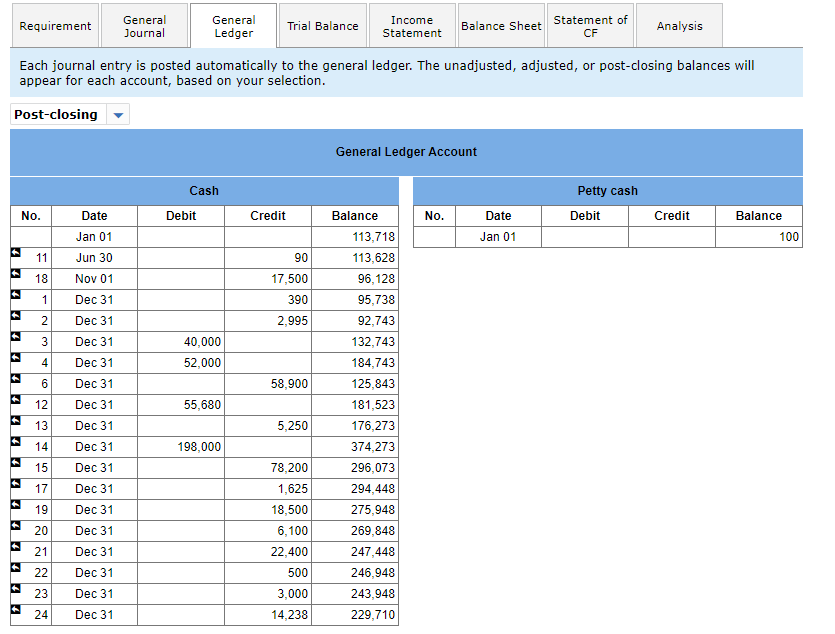

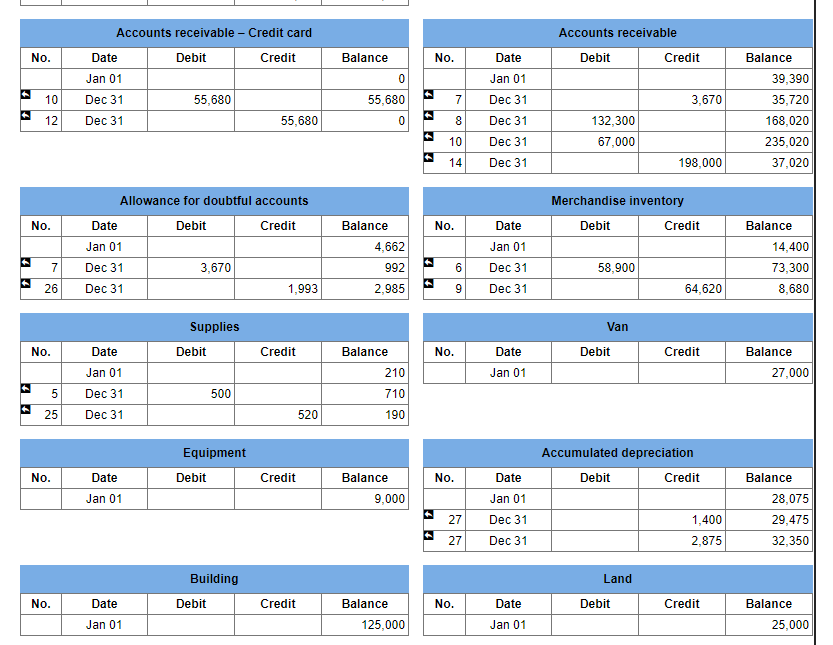

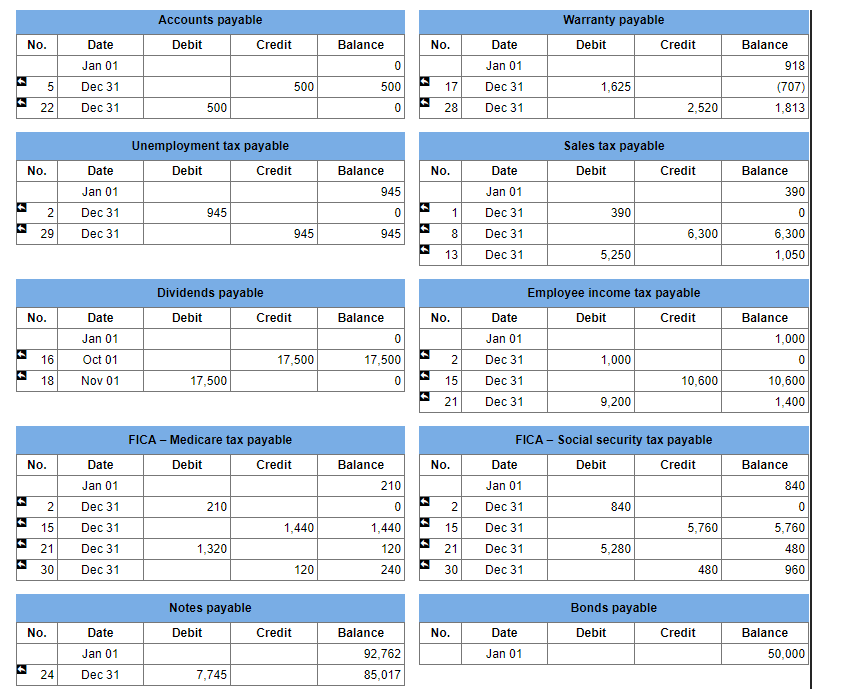

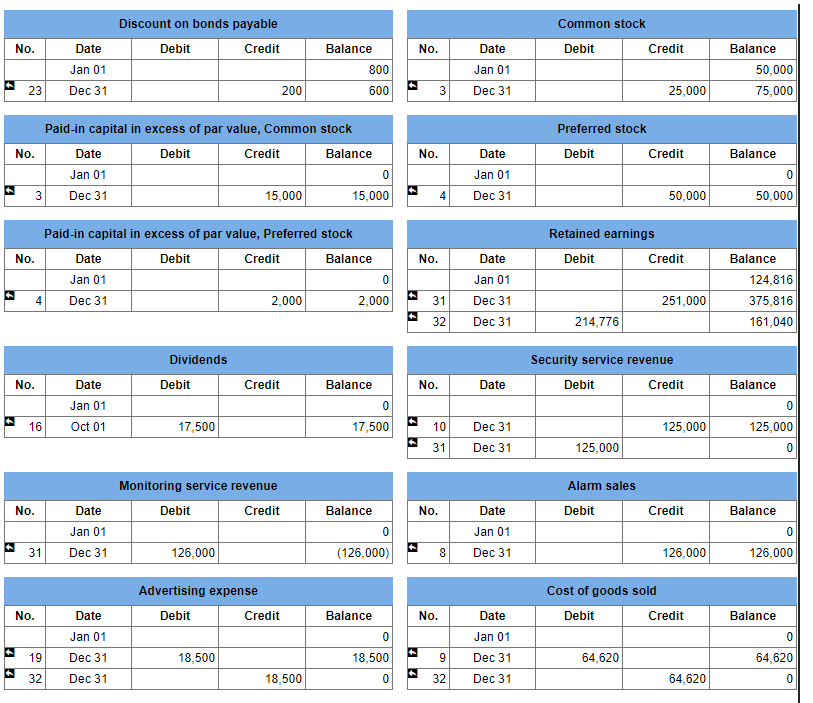

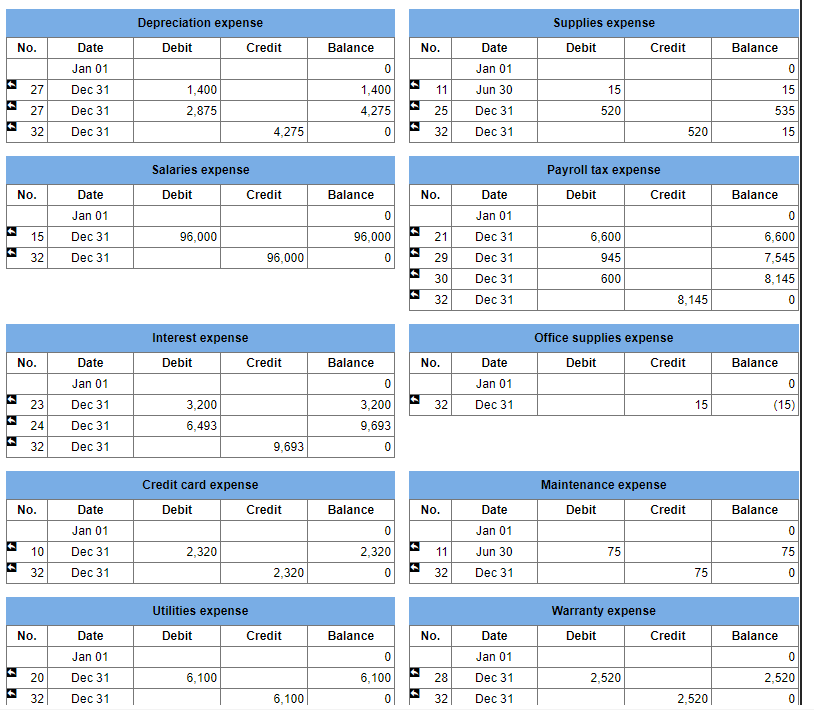

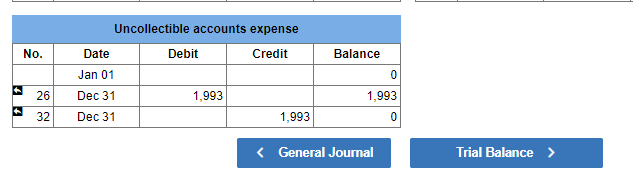

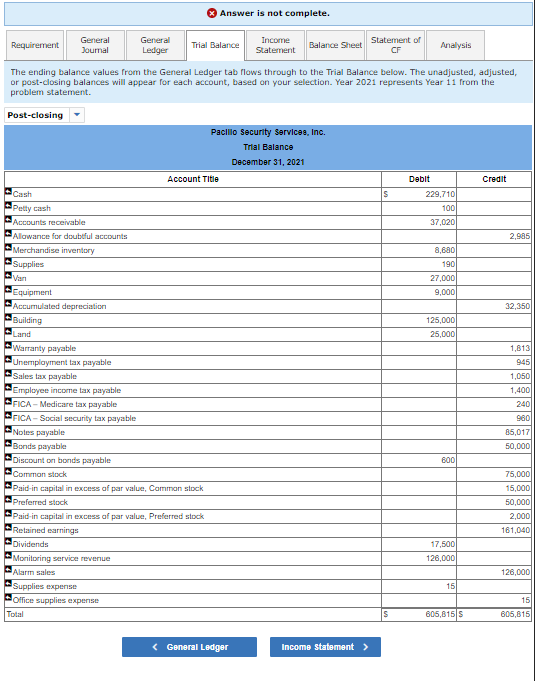

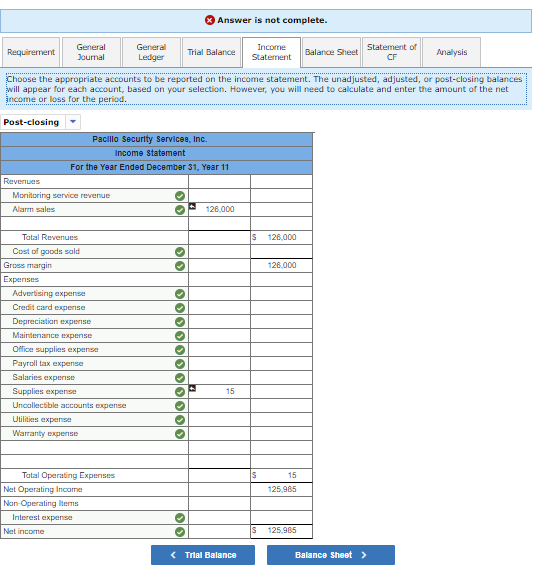

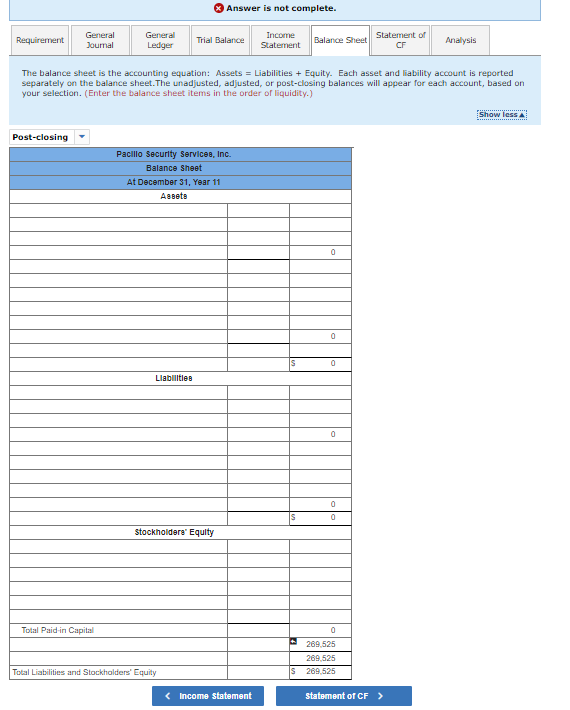

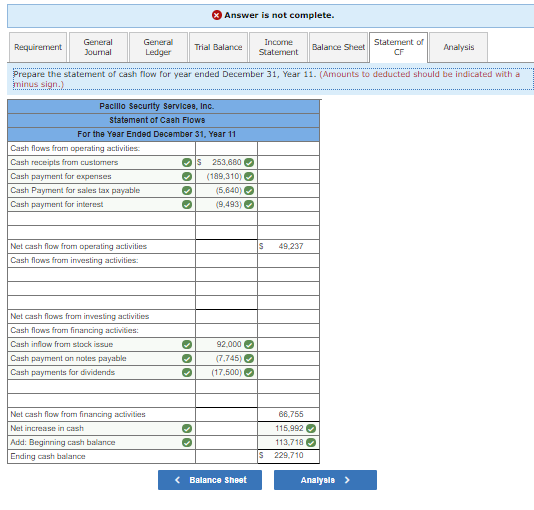

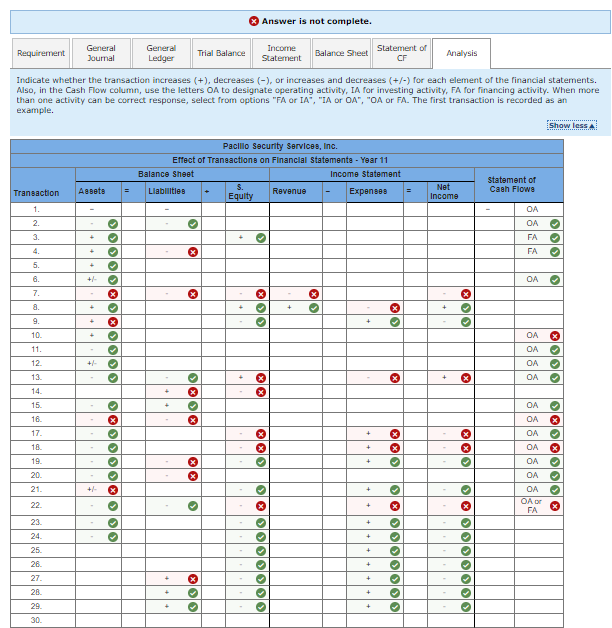

The trial balance of Pacilio Security Services, Inc. as of January 1, Year 11, had the following normal balances: Cash Petty cash Accounts receivable Allowance for doubtful accounts Supplies Merchandise inventory (48 @ $300) Equipment Van Building Accumulated depreciation Land Sales tax payable Employee income tax payable FICA-Social Security tax payable FICA-Medicare tax payable Warranty payable Unemployment tax payable Notes payable-Building Bonds payable Discount on bonds payable Common stock Retained earnings $113, 718 100 39,390 4,662 210 14,400 9,000 27,000 125,000 28,075 25,000 390 1,000 840 210 918 945 92,762 50,000 800 50,000 124,816 During Year 11, Pacilio Security Services experienced the following transactions: 1. Paid the sales tax payable from Year 10. 2. Paid the balance of the payroll liabilities due for Year 10 (federal income tax, FICA taxes, and unemployment taxes). 3. Issued 5,000 additional shares of the $5 par value common stock for $8 per share. 4. Issued 1,000 shares of $50 stated value, 5 percent cumulative preferred stock for $52 per share. 5. Purchased $500 of supplies on account. 6. Purchased 190 alarm systems at a cost of $310. Cash was paid for the purchase. 7. After numerous attempts to collect from customers, wrote off $3,670 of uncollectible accounts receivable. 8. Sold 210 alarm systems for $600 each plus sales tax of 5 percent. All sales were on account. 9. Record the cost of goods sold related to the sale from Event 8 using the FIFO method. 10. Billed $125,000 of monitoring services for the year. Credit card sales amounted to $58,000, and the credit card company charged a 4 percent fee. The remaining $67,000 were sales on account. Sales tax is not charged on this service. 11. Replenished the petty cash fund on June 30. The fund had $10 cash and receipts of $75 for yard mowing and $15 for office supplies expense. 12. Collected the amount due from the credit card company. 13. Paid the sales tax collected on $105,000 of the alarm sales. 14. Collected $198,000 of accounts receivable during the year. 15. Paid installers and other employees a total of $96,000 for salaries for the year. Assume the Social Security tax rate is 6 percent and the Medicare tax rate is 1.5 percent. Federal income taxes withheld amounted to $10,600. No employee exceeded $110,000 in total wages. The net salaries were paid in cash. 16. On October 1, declared a dividend on the preferred stock and a $1 per share dividend on the common stock to be paid to shareholders of record on October 15, payable on November 1, Year 11. 17. Paid $1,625 in warranty repairs during the year. 18. On November 1, Year 11, paid the dividends that had been previously declared. 19. Paid $18,500 of advertising expense during the year. 20. Paid $6,100 of utilities expense for the year. 21. Paid $9,200 of the Employee Income Tax Payable, $5,280 of the FICA Tax Soc. Sec. Tax Payable and $1,320 of the FICA Tax Medicare Tax Payable. Also, paid the Payroll Tax Expense for the 7.5% employer matching of FICA taxes on $88,000 of salaries. 22. Paid the accounts payable. 23. Paid bond interest and amortized the discount. The bond was issued in Year 10 and pays interest at 6 percent. 24. Paid the annual installment of $14,238 on the amortized note. The interest rate for the note is 7 percent. Adjustment 25. There was $190 of supplies on hand at the end of the year. 26. Recognized the uncollectible accounts expense for the year using the allowance method. Pacilio now estimates that 1 percent of sales on account will not be collected. 27. Recognized depreciation expense on the equipment, van, and building. The equipment, purchased in Year 8, has a five-year life and a $2,000 salvage value. The van has a four-year life and a $6,000 salvage value. The building has a 40-year life and a $10,000 salvage value. The company uses straight-line for the equipment and the building. The van is fully depreciated. 28. The alarm systems sold in transaction 7 were covered with a one-year warranty. Pacilio estimated that the warranty cost would be 2 percent of alarm sales. 29. The unemployment tax on the three employees has not been paid. Record the accrued unemployment tax on the salaries for the year. The unemployment tax rate is 4.5 percent and gross wages for all three employees exceeded $7,000. 30. Recognized the employer Social Security and Medicare payroll tax that has not been paid on $8,000 of salaries expense. Requirement General Journal General Ledger Trial Balance Income Statement Balance Sheet Statement of CF Analysis General Journal tab - Prepare the journal entries to record transactions (1) through (24). Then prepare the necessary adjusting entries (25) through (30) to correctly report net income for the period. Then record the closing entries (31) through (33) as of December 31, Year 11. General Ledger tab - Each journal entry is posted automatically to the general ledger. Trial Balance tab - The ending balance values from the General Ledger tab flows through to the Trial Balance tab. Income Statement tab - Use the drop-down to select the accounts properly included on the income statement. Balance Sheet tab - Prepare a classified Balance Sheet at December 31, Year 11. Statement of Cash flows - Prepare the statement of cash flow for year ended December 31, Year 11. Analysis tab - Use a horizontal statements model to show how each transaction affects the balance sheet, income statement, and statement of cash flows. No Date General Journal Debit Credit 1 Dec 31 390 Sales tax payable Cash 390 2. Dec 31 1.000 840 Employee income tax payable FICA - Social security tax payable FICA - Medicare tax payable Unemployment tax payable Cash 210 OOOO 945 2.995 Dec 31 Cash 40.000 O 100 Common stock 25.000 Paid-in capital in excess of par value, Common stock 15,000 4 Dec 31 Cash 52.000 Preferred stock Paid-in capital in excess of par value, Preferred stock DOO 50,000 2,000 5 Dec 31 500 Supplies Accounts payable 010 500 Dec 31 58.900 Merchandise inventory Cash lolo 58.900 7 Dec 31 3.670 Allowance for doubtful accounts Accounts receivable DO 3.670 8 Dec 31 132.300 . Accounts receivable Alarm sales Sales tax payable olo 126.000 6.300 9 Dec 31 64.620 . Cast of goods sold Merchandise inventory olo 64.620 10 Dec 31 Accounts receivable - Credit card Accounts receivable Credit card expense Security service revenu OOO 55,680 67 000 2,320 125.000 11 Jun 30 Supplies expense Maintenance expense Cash OO 15 75 90 12 Dec 31 Cash 55,680 DO Accounts receivable - Credit card 55.680 13 Dec 31 5.250 Sales tax payable Cash OO 5.250 14 Dec 31 196.000 Cash Accounts receivable 196.000 15 Dec 31 96.000 Salaries expense Employee income tax payable FICA - Social security tax payable FICA - Medicare tax payable Cash OOOOOO 10.600 5.780 1.440 78.200 16 Oct 01 17,500 Dividends Dividends payable 17,500 17 Dec 31 1,625 Warranty payable Cash lolo 1,625 18 Nov 01 17,500 Dividends payable Cash lolo 17.500 19 Dec 31 18,500 Advertising expense Cash 18.500 20 Dec 31 Utilities expense 6.100 Cash 6.100 OOOO OOOOO 21 Dec 31 Employee income tax payable FICA - Social security tax payable FICA - Medicare tax payable Payroll tax expense Cash 9.200 5.280 1.320 8.600 22.400 22 Dec 31 500 Accounts payable Cash 500 OO OOO 23 Dec 31 3.200 Interest expense Discount on bonds payable Cash 200 3,000 24 Dec 31 Notes payable Interest expense Cash lololo 7.745 8,493 14.238 25 Dec 31 Supplies expense Supplies lolo 520 520 26 Dec 31 Uncollectible accounts expense 1.993 Allowance for doubtful accounts 1,993 OOOO 27 Dec 31 1,400 1,400 Depreciation expense Accumulated depreciation Depreciation expense Accumulated depreciation 3 2.875 2.875 28 Dec 31 2.520 Warranty expense Warranty payable olo 2.520 29 Dec 31 945 Payroll tax expense Unemployment tax payable lolo 945 30 Dec 31 600 . Payroll tax expense FICA - Social security tax payable FICA - Medicare tax payable OOO 480 120 lolo 31 Dec 31 Monitoring service revenue Security service revenue Retained earnings 126.000 125.000 X 251.000 32 Dec 31 214,776 > lololol 64.620 Retained earnings Cost of goods sold Advertising expense Credit card expense Depreciation expense Maintenance expense Office supplies expense Payroll tax expense Salaries expense Supplies expense Uncollectible accounts expense Utilities expense Warranty expense Interest expense 18.500 2320 4.275 75 15 8.145 96.000 520 1.993 6.100 2.520 9.693 Requirement General Journal General Ledger Trial Balance Income Statement Balance Sheet Statement of CF Analysis Each journal entry is posted automatically to the general ledger. The unadjusted, adjusted, or post-closing balances will appear for each account, based on your selection. Post-closing General Ledger Account Cash Debit Petty cash Debit No. Date Credit Balance No. Date Credit Balance 100 Jan 01 Jan 01 11 90 18 1 Jun 30 Nov 01 Dec 31 17,500 390 2,995 2 3 Dec 31 Dec 31 Dec 31 Dec 31 40,000 52,000 4 6 58,900 12 Dec 31 55,680 13 5,250 113,718 113,628 96,128 95,738 92,743 132,743 184,743 125,843 181,523 176,273 374,273 296,073 294,448 275,948 269,848 247,448 246,948 243,948 229,710 14 198,000 15 ttt 17 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 19 78,200 1,625 18,500 6,100 22,400 500 20 21 22 23 3,000 24 14,238 Warranty payable Accounts payable Debit Credit No. Balance No. Date Debit Credit Balance 0 918 Date Jan 01 Dec 31 Dec 31 5 500 500 17 + 1 Jan 01 Dec 31 Dec 31 1,625 (707) 1,813 22 500 0 28 2,520 Unemployment tax payable Debit Credit Sales tax payable Debit Credit No. Balance No. Date Balance 945 390 Date Jan 01 Dec 31 Dec 31 7 2 945 0 1 390 0 Jan 01 Dec 31 Dec 31 Dec 31 1 1 29 945 945 8 6,300 6,300 1,050 T 13 5,250 Dividends payable Debit Credit No. Balance No. 0 Date Jan 01 Oct 01 Nov 01 Employee income tax payable Date Debit Credit Jan 01 Dec 31 1,000 Dec 31 10,600 Dec 31 9,200 Balance 1,000 0 16 tt 17,500 17,500 tt 2 15 18 17,500 0 10,600 1,400 T 21 FICA - Medicare tax payable Debit Credit No. Balance No. Balance 840 210 1 210 0 2 + + 0 FICA - Social security tax payable Date Debit Credit Jan 01 Dec 31 840 Dec 31 5,760 Dec 31 5,280 Dec 31 480 Date Jan 01 Dec 31 Dec 31 Dec 31 Dec 31 7 1,440 15 21 30 1,440 120 7 5,760 480 15 21 30 1,320 7 120 240 960 Notes payable Debit Credit Bonds payable Debit Credit No. No. Date Date Jan 01 Dec 31 Balance 92,762 85,017 Balance 50,000 Jan 01 24 7,745 Common stock Discount on bonds payable Debit Credit No. No. Date Debit Credit Date Jan 01 Dec 31 Balance 800 600 Jan 01 Balance 50,000 75,000 23 200 3 Dec 31 25,000 Preferred stock No. Date Debit Credit Balance Paid-in capital in excess of par value, Common stock No. Date Debit Credit Balance Jan 01 0 3 Dec 31 15,000 15,000 Jan 01 0 4 Dec 31 50,000 50,000 Retained earnings Debit Credit No. No. Paid-in capital in excess of par value, Preferred stock Date Debit Credit Balance Jan 01 Dec 31 2,000 2,000 Date Jan 01 Dec 31 Dec 31 Balance 124,816 375,816 161,040 1 4 31 251,000 t 32 214,776 Dividends Security service revenue Debit Credit No. Date Debit Credit Balance No. Date Balance Jan 01 0 0 11 16 Oct 01 17,500 17,500 10 125,000 Dec 31 Dec 31 125,000 0 + 31 125,000 Alarm sales Monitoring service revenue Debit Credit No. Balance No. Debit Credit Balance Date Jan 01 Dec 31 0 Date Jan 01 Dec 31 0 31 126,000 (126,000) 8 126,000 126,000 Advertising expense Debit Credit Cost of goods sold Debit Credit No. Balance No. Balance Date Jan 01 Date Jan 01 0 0 19 11 18,500 9 tt Dec 31 64,620 Dec 31 Dec 31 64,620 18,500 0 32 18,500 32 Dec 31 64,620 Depreciation expense Supplies expense No. Debit Credit No. Date Debit Credit Balance 0 Date Jan 01 Dec 31 Dec 31 Balance 0 1,400 4,275 7 t 11 15 Jan 01 Jun 30 Dec 31 27 27 15 1,400 2,875 2 25 520 535 32 Dec 31 4,275 0 32 Dec 31 520 15 Salaries expense Payroll tax expense No. Date Debit Credit Balance No. Date Debit Credit Balance 0 0 7 15 Jan 01 Dec 31 Dec 31 96,000 96,000 21 6,600 945 7 32 96,000 0 Jan 01 Dec 31 Dec 31 Dec 31 Dec 31 29 6,600 7,545 8,145 0 30 600 t 32 8,145 Interest expense Debit Credit Office supplies expense Debit Credit No. Balance No. Balance 0 Date Jan 01 Dec 31 0 7 Date Jan 01 Dec 31 Dec 31 Dec 31 23 32 15 (15) 3,200 6,493 24 tt 3,200 9,693 0 32 9,693 Maintenance expense Credit card expense Debit Credit No. Balance No. Date Debit Credit Balance 0 Jan 01 0 Date Jan 01 Dec 31 Dec 31 7 2,320 11 75 75 10 32 2,320 0 f Jun 30 Dec 31 2,320 32 75 0 Utilities expense Debit Credit Warranty expense Debit Credit No. Balance No. Balance Date Jan 01 Date Jan 01 0 0 20 tt Dec 31 6.100 6,100 28 Dec 31 2,520 2,520 0 32 Dec 31 6,100 0 32 Dec 31 2,520 Uncollectible accounts expense No. Debit Credit Balance 0 Date Jan 01 Dec 31 Dec 31 26 1,993 1,993 0 32 1,993 Answer is not complete. Requirement General Journal General Ledger Trial Balance Income Statement Balance Sheet Statement of CF Analysis The ending balance values from the General Ledger tab flows through to the Trial Balance below. The unadjusted, adjusted, or post-closing balances will appear for each account, based on your selection. Year 2021 represents Year 11 from the problem statement. Post-closing Pacillo Security Services, Inc. Trial Balance December 31, 2021 Account Title Credit IS Debit 229,7101 1001 37,020 2.995 8,680 190 27,000 9,0001 32,350 125,000 25,000 1,613 Cash Petty cash Accounts receivable Allowance for doubtful accounts Merchandise inventory Supplies Van Equipment Accumulated depreciation Building Land Warranty payable Unemployment tax payable Sales tax payable Employee income tax payable FICA-Medicare tax payable FICA - Social security tax payable Noles payable Bonds payable Discount on bonds payable Common stock Paid-in capital in excess of par value, Caminan stock Preferred stock Paid-in capital in excess of par value, Preferred stock Retained earnings Dividends Monitoring service revenue Alarm sales Supplies experise Office supplies expense Total 945 1,050 1,400 240 960 85,017 50,000 600 75,000 15,000 50,000 2,000 161,040 17,500 126,000 128,000 151 15 605,81515 605,815 Answer is not complete. Requirement General Journal General Ledger Trial Balance Income Statement Balance Sheet Statement of CF Analysis Choose the appropriate accounts to be reported on the income statement. The unadjusted, adjusted, or post-closing balances will appear for each account, based on your selection. However, you will need to calculate and enter the amount of the net income or loss for the period. Post-closing Pacillo Security Services, Inc. Income Statement For the Year Ended December 31, Year 11 Revenues Monitoring service revenue Alarm sales 126,000 OO IS 126,000 OO 126,000 Total Revenues Cost of goods sold Gross margin Expenses Advertising expense Credit card expense Depreciation expense Maintenance expense Office supplies expense Payroll tax expense Salaries expense Supplies expense Uncollectible accounts expense Utilities expense Warranty expense OOOOOOOOOOO 15 IS 15 125.965 Talal Operating Expenses Net Operating Income Non-Operating Items Interest expense Net income IS 125.965 O Answer is not complete. Requirement General Journal General Ledger Trial Balance Income Statement Balance Sheet Statement of CF Analysis The balance sheet is the accounting equation: Assets = Liabilities + Equity. Each asset and liability account is reported separately on the balance sheet. The unadjusted, adjusted, or post-closing balances will appear for each account, based on your selection. (Enter the balance sheet items in the order of liquidity.) Show less A ***** Post-closing Pacillo Security Services, Inc. Balance Sheet At December 31, Year 11 Assets 0 0 0 Llabilities 0 0 IS 0 Stockholders' Equity Total Paid in Capital 0 269,525 269,525 269,525 Total Liabilities and Stockholders' Equity Answer is not complete. Requirement General Journal General Ledger Trial Balance Income Statement Balance Sheet Statement of CF Analysis Prepare the statement of cash flow for year ended December 31, Year 11. (Amounts to deducted should be indicated with a minus sign.). Pacillo Security Services, Inc. Statement of Cash Flowe For the Year Ended December 31, Year 11 Cash flows from operating activities Cash receipts from customers S 253.680 Cash payment for expenses (189,310) Cash Payment for sales tax payable (5,640) Cash payment for interest (9,493) OOOO IS 49.237 Net cash flow from operating activities Cash flows from investing activities: Net cash flows from investing activities Cash flows from financing activities: Cash inflow from stock issue Cash payment on notes payable Cash payments for dividends OOO 92,000 (7,745) (17,500) Net cash flow from financing activities Net increase in cash Add: Beginning cash balance Ending cash balance 66.755 115.992 113.718 229.710 IS Answer is not complete. Requirement General Journal General Ledger Trial Balance Income Statement Balance Sheet Statement of CF Analysis Indicate whether the transaction increases (+), decreases (-), or increases and decreases (+/-) for each element of the financial statements. Also, in the Cash Flow column, use the letters OA to designate operating activity, IA for investing activity, FA for financing activity. When more than one activity can be correct response, select from options "FA or IA", "IA or OA", "OA or FA. The first transaction is recorded as an example. Show less A Pacillo Security Services, Inc. Effect of Transactions on Financial Statements - Year 11 Balance Sheet Income Statement Llabilities Revenue Equity Expenses Statement of Cash Flows Transaction Net Income Assets OA 1. 2. ol OA lololo FA FA OOO 5. G. + OA * 3 x x 7. 8. 9. O OO + 10. x OA OA 11. 12 + lolo OA OA 13 x X 14 BOBO 15. 16 17. OOO OOOOO + x X x 18 + + 19. 20 OOOOOOOO OA OA OA OA OA OA OA DE FA 21 + + 22 . + 23 24 25. O OOOOOOO + OOOOOOOO ololololololo + 26 + 27. + + 28 29. 30. OO + The trial balance of Pacilio Security Services, Inc. as of January 1, Year 11, had the following normal balances: Cash Petty cash Accounts receivable Allowance for doubtful accounts Supplies Merchandise inventory (48 @ $300) Equipment Van Building Accumulated depreciation Land Sales tax payable Employee income tax payable FICA-Social Security tax payable FICA-Medicare tax payable Warranty payable Unemployment tax payable Notes payable-Building Bonds payable Discount on bonds payable Common stock Retained earnings $113, 718 100 39,390 4,662 210 14,400 9,000 27,000 125,000 28,075 25,000 390 1,000 840 210 918 945 92,762 50,000 800 50,000 124,816 During Year 11, Pacilio Security Services experienced the following transactions: 1. Paid the sales tax payable from Year 10. 2. Paid the balance of the payroll liabilities due for Year 10 (federal income tax, FICA taxes, and unemployment taxes). 3. Issued 5,000 additional shares of the $5 par value common stock for $8 per share. 4. Issued 1,000 shares of $50 stated value, 5 percent cumulative preferred stock for $52 per share. 5. Purchased $500 of supplies on account. 6. Purchased 190 alarm systems at a cost of $310. Cash was paid for the purchase. 7. After numerous attempts to collect from customers, wrote off $3,670 of uncollectible accounts receivable. 8. Sold 210 alarm systems for $600 each plus sales tax of 5 percent. All sales were on account. 9. Record the cost of goods sold related to the sale from Event 8 using the FIFO method. 10. Billed $125,000 of monitoring services for the year. Credit card sales amounted to $58,000, and the credit card company charged a 4 percent fee. The remaining $67,000 were sales on account. Sales tax is not charged on this service. 11. Replenished the petty cash fund on June 30. The fund had $10 cash and receipts of $75 for yard mowing and $15 for office supplies expense. 12. Collected the amount due from the credit card company. 13. Paid the sales tax collected on $105,000 of the alarm sales. 14. Collected $198,000 of accounts receivable during the year. 15. Paid installers and other employees a total of $96,000 for salaries for the year. Assume the Social Security tax rate is 6 percent and the Medicare tax rate is 1.5 percent. Federal income taxes withheld amounted to $10,600. No employee exceeded $110,000 in total wages. The net salaries were paid in cash. 16. On October 1, declared a dividend on the preferred stock and a $1 per share dividend on the common stock to be paid to shareholders of record on October 15, payable on November 1, Year 11. 17. Paid $1,625 in warranty repairs during the year. 18. On November 1, Year 11, paid the dividends that had been previously declared. 19. Paid $18,500 of advertising expense during the year. 20. Paid $6,100 of utilities expense for the year. 21. Paid $9,200 of the Employee Income Tax Payable, $5,280 of the FICA Tax Soc. Sec. Tax Payable and $1,320 of the FICA Tax Medicare Tax Payable. Also, paid the Payroll Tax Expense for the 7.5% employer matching of FICA taxes on $88,000 of salaries. 22. Paid the accounts payable. 23. Paid bond interest and amortized the discount. The bond was issued in Year 10 and pays interest at 6 percent. 24. Paid the annual installment of $14,238 on the amortized note. The interest rate for the note is 7 percent. Adjustment 25. There was $190 of supplies on hand at the end of the year. 26. Recognized the uncollectible accounts expense for the year using the allowance method. Pacilio now estimates that 1 percent of sales on account will not be collected. 27. Recognized depreciation expense on the equipment, van, and building. The equipment, purchased in Year 8, has a five-year life and a $2,000 salvage value. The van has a four-year life and a $6,000 salvage value. The building has a 40-year life and a $10,000 salvage value. The company uses straight-line for the equipment and the building. The van is fully depreciated. 28. The alarm systems sold in transaction 7 were covered with a one-year warranty. Pacilio estimated that the warranty cost would be 2 percent of alarm sales. 29. The unemployment tax on the three employees has not been paid. Record the accrued unemployment tax on the salaries for the year. The unemployment tax rate is 4.5 percent and gross wages for all three employees exceeded $7,000. 30. Recognized the employer Social Security and Medicare payroll tax that has not been paid on $8,000 of salaries expense. Requirement General Journal General Ledger Trial Balance Income Statement Balance Sheet Statement of CF Analysis General Journal tab - Prepare the journal entries to record transactions (1) through (24). Then prepare the necessary adjusting entries (25) through (30) to correctly report net income for the period. Then record the closing entries (31) through (33) as of December 31, Year 11. General Ledger tab - Each journal entry is posted automatically to the general ledger. Trial Balance tab - The ending balance values from the General Ledger tab flows through to the Trial Balance tab. Income Statement tab - Use the drop-down to select the accounts properly included on the income statement. Balance Sheet tab - Prepare a classified Balance Sheet at December 31, Year 11. Statement of Cash flows - Prepare the statement of cash flow for year ended December 31, Year 11. Analysis tab - Use a horizontal statements model to show how each transaction affects the balance sheet, income statement, and statement of cash flows. No Date General Journal Debit Credit 1 Dec 31 390 Sales tax payable Cash 390 2. Dec 31 1.000 840 Employee income tax payable FICA - Social security tax payable FICA - Medicare tax payable Unemployment tax payable Cash 210 OOOO 945 2.995 Dec 31 Cash 40.000 O 100 Common stock 25.000 Paid-in capital in excess of par value, Common stock 15,000 4 Dec 31 Cash 52.000 Preferred stock Paid-in capital in excess of par value, Preferred stock DOO 50,000 2,000 5 Dec 31 500 Supplies Accounts payable 010 500 Dec 31 58.900 Merchandise inventory Cash lolo 58.900 7 Dec 31 3.670 Allowance for doubtful accounts Accounts receivable DO 3.670 8 Dec 31 132.300 . Accounts receivable Alarm sales Sales tax payable olo 126.000 6.300 9 Dec 31 64.620 . Cast of goods sold Merchandise inventory olo 64.620 10 Dec 31 Accounts receivable - Credit card Accounts receivable Credit card expense Security service revenu OOO 55,680 67 000 2,320 125.000 11 Jun 30 Supplies expense Maintenance expense Cash OO 15 75 90 12 Dec 31 Cash 55,680 DO Accounts receivable - Credit card 55.680 13 Dec 31 5.250 Sales tax payable Cash OO 5.250 14 Dec 31 196.000 Cash Accounts receivable 196.000 15 Dec 31 96.000 Salaries expense Employee income tax payable FICA - Social security tax payable FICA - Medicare tax payable Cash OOOOOO 10.600 5.780 1.440 78.200 16 Oct 01 17,500 Dividends Dividends payable 17,500 17 Dec 31 1,625 Warranty payable Cash lolo 1,625 18 Nov 01 17,500 Dividends payable Cash lolo 17.500 19 Dec 31 18,500 Advertising expense Cash 18.500 20 Dec 31 Utilities expense 6.100 Cash 6.100 OOOO OOOOO 21 Dec 31 Employee income tax payable FICA - Social security tax payable FICA - Medicare tax payable Payroll tax expense Cash 9.200 5.280 1.320 8.600 22.400 22 Dec 31 500 Accounts payable Cash 500 OO OOO 23 Dec 31 3.200 Interest expense Discount on bonds payable Cash 200 3,000 24 Dec 31 Notes payable Interest expense Cash lololo 7.745 8,493 14.238 25 Dec 31 Supplies expense Supplies lolo 520 520 26 Dec 31 Uncollectible accounts expense 1.993 Allowance for doubtful accounts 1,993 OOOO 27 Dec 31 1,400 1,400 Depreciation expense Accumulated depreciation Depreciation expense Accumulated depreciation 3 2.875 2.875 28 Dec 31 2.520 Warranty expense Warranty payable olo 2.520 29 Dec 31 945 Payroll tax expense Unemployment tax payable lolo 945 30 Dec 31 600 . Payroll tax expense FICA - Social security tax payable FICA - Medicare tax payable OOO 480 120 lolo 31 Dec 31 Monitoring service revenue Security service revenue Retained earnings 126.000 125.000 X 251.000 32 Dec 31 214,776 > lololol 64.620 Retained earnings Cost of goods sold Advertising expense Credit card expense Depreciation expense Maintenance expense Office supplies expense Payroll tax expense Salaries expense Supplies expense Uncollectible accounts expense Utilities expense Warranty expense Interest expense 18.500 2320 4.275 75 15 8.145 96.000 520 1.993 6.100 2.520 9.693 Requirement General Journal General Ledger Trial Balance Income Statement Balance Sheet Statement of CF Analysis Each journal entry is posted automatically to the general ledger. The unadjusted, adjusted, or post-closing balances will appear for each account, based on your selection. Post-closing General Ledger Account Cash Debit Petty cash Debit No. Date Credit Balance No. Date Credit Balance 100 Jan 01 Jan 01 11 90 18 1 Jun 30 Nov 01 Dec 31 17,500 390 2,995 2 3 Dec 31 Dec 31 Dec 31 Dec 31 40,000 52,000 4 6 58,900 12 Dec 31 55,680 13 5,250 113,718 113,628 96,128 95,738 92,743 132,743 184,743 125,843 181,523 176,273 374,273 296,073 294,448 275,948 269,848 247,448 246,948 243,948 229,710 14 198,000 15 ttt 17 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 Dec 31 19 78,200 1,625 18,500 6,100 22,400 500 20 21 22 23 3,000 24 14,238 Warranty payable Accounts payable Debit Credit No. Balance No. Date Debit Credit Balance 0 918 Date Jan 01 Dec 31 Dec 31 5 500 500 17 + 1 Jan 01 Dec 31 Dec 31 1,625 (707) 1,813 22 500 0 28 2,520 Unemployment tax payable Debit Credit Sales tax payable Debit Credit No. Balance No. Date Balance 945 390 Date Jan 01 Dec 31 Dec 31 7 2 945 0 1 390 0 Jan 01 Dec 31 Dec 31 Dec 31 1 1 29 945 945 8 6,300 6,300 1,050 T 13 5,250 Dividends payable Debit Credit No. Balance No. 0 Date Jan 01 Oct 01 Nov 01 Employee income tax payable Date Debit Credit Jan 01 Dec 31 1,000 Dec 31 10,600 Dec 31 9,200 Balance 1,000 0 16 tt 17,500 17,500 tt 2 15 18 17,500 0 10,600 1,400 T 21 FICA - Medicare tax payable Debit Credit No. Balance No. Balance 840 210 1 210 0 2 + + 0 FICA - Social security tax payable Date Debit Credit Jan 01 Dec 31 840 Dec 31 5,760 Dec 31 5,280 Dec 31 480 Date Jan 01 Dec 31 Dec 31 Dec 31 Dec 31 7 1,440 15 21 30 1,440 120 7 5,760 480 15 21 30 1,320 7 120 240 960 Notes payable Debit Credit Bonds payable Debit Credit No. No. Date Date Jan 01 Dec 31 Balance 92,762 85,017 Balance 50,000 Jan 01 24 7,745 Common stock Discount on bonds payable Debit Credit No. No. Date Debit Credit Date Jan 01 Dec 31 Balance 800 600 Jan 01 Balance 50,000 75,000 23 200 3 Dec 31 25,000 Preferred stock No. Date Debit Credit Balance Paid-in capital in excess of par value, Common stock No. Date Debit Credit Balance Jan 01 0 3 Dec 31 15,000 15,000 Jan 01 0 4 Dec 31 50,000 50,000 Retained earnings Debit Credit No. No. Paid-in capital in excess of par value, Preferred stock Date Debit Credit Balance Jan 01 Dec 31 2,000 2,000 Date Jan 01 Dec 31 Dec 31 Balance 124,816 375,816 161,040 1 4 31 251,000 t 32 214,776 Dividends Security service revenue Debit Credit No. Date Debit Credit Balance No. Date Balance Jan 01 0 0 11 16 Oct 01 17,500 17,500 10 125,000 Dec 31 Dec 31 125,000 0 + 31 125,000 Alarm sales Monitoring service revenue Debit Credit No. Balance No. Debit Credit Balance Date Jan 01 Dec 31 0 Date Jan 01 Dec 31 0 31 126,000 (126,000) 8 126,000 126,000 Advertising expense Debit Credit Cost of goods sold Debit Credit No. Balance No. Balance Date Jan 01 Date Jan 01 0 0 19 11 18,500 9 tt Dec 31 64,620 Dec 31 Dec 31 64,620 18,500 0 32 18,500 32 Dec 31 64,620 Depreciation expense Supplies expense No. Debit Credit No. Date Debit Credit Balance 0 Date Jan 01 Dec 31 Dec 31 Balance 0 1,400 4,275 7 t 11 15 Jan 01 Jun 30 Dec 31 27 27 15 1,400 2,875 2 25 520 535 32 Dec 31 4,275 0 32 Dec 31 520 15 Salaries expense Payroll tax expense No. Date Debit Credit Balance No. Date Debit Credit Balance 0 0 7 15 Jan 01 Dec 31 Dec 31 96,000 96,000 21 6,600 945 7 32 96,000 0 Jan 01 Dec 31 Dec 31 Dec 31 Dec 31 29 6,600 7,545 8,145 0 30 600 t 32 8,145 Interest expense Debit Credit Office supplies expense Debit Credit No. Balance No. Balance 0 Date Jan 01 Dec 31 0 7 Date Jan 01 Dec 31 Dec 31 Dec 31 23 32 15 (15) 3,200 6,493 24 tt 3,200 9,693 0 32 9,693 Maintenance expense Credit card expense Debit Credit No. Balance No. Date Debit Credit Balance 0 Jan 01 0 Date Jan 01 Dec 31 Dec 31 7 2,320 11 75 75 10 32 2,320 0 f Jun 30 Dec 31 2,320 32 75 0 Utilities expense Debit Credit Warranty expense Debit Credit No. Balance No. Balance Date Jan 01 Date Jan 01 0 0 20 tt Dec 31 6.100 6,100 28 Dec 31 2,520 2,520 0 32 Dec 31 6,100 0 32 Dec 31 2,520 Uncollectible accounts expense No. Debit Credit Balance 0 Date Jan 01 Dec 31 Dec 31 26 1,993 1,993 0 32 1,993 Answer is not complete. Requirement General Journal General Ledger Trial Balance Income Statement Balance Sheet Statement of CF Analysis The ending balance values from the General Ledger tab flows through to the Trial Balance below. The unadjusted, adjusted, or post-closing balances will appear for each account, based on your selection. Year 2021 represents Year 11 from the problem statement. Post-closing Pacillo Security Services, Inc. Trial Balance December 31, 2021 Account Title Credit IS Debit 229,7101 1001 37,020 2.995 8,680 190 27,000 9,0001 32,350 125,000 25,000 1,613 Cash Petty cash Accounts receivable Allowance for doubtful accounts Merchandise inventory Supplies Van Equipment Accumulated depreciation Building Land Warranty payable Unemployment tax payable Sales tax payable Employee income tax payable FICA-Medicare tax payable FICA - Social security tax payable Noles payable Bonds payable Discount on bonds payable Common stock Paid-in capital in excess of par value, Caminan stock Preferred stock Paid-in capital in excess of par value, Preferred stock Retained earnings Dividends Monitoring service revenue Alarm sales Supplies experise Office supplies expense Total 945 1,050 1,400 240 960 85,017 50,000 600 75,000 15,000 50,000 2,000 161,040 17,500 126,000 128,000 151 15 605,81515 605,815 Answer is not complete. Requirement General Journal General Ledger Trial Balance Income Statement Balance Sheet Statement of CF Analysis Choose the appropriate accounts to be reported on the income statement. The unadjusted, adjusted, or post-closing balances will appear for each account, based on your selection. However, you will need to calculate and enter the amount of the net income or loss for the period. Post-closing Pacillo Security Services, Inc. Income Statement For the Year Ended December 31, Year 11 Revenues Monitoring service revenue Alarm sales 126,000 OO IS 126,000 OO 126,000 Total Revenues Cost of goods sold Gross margin Expenses Advertising expense Credit card expense Depreciation expense Maintenance expense Office supplies expense Payroll tax expense Salaries expense Supplies expense Uncollectible accounts expense Utilities expense Warranty expense OOOOOOOOOOO 15 IS 15 125.965 Talal Operating Expenses Net Operating Income Non-Operating Items Interest expense Net income IS 125.965 O Answer is not complete. Requirement General Journal General Ledger Trial Balance Income Statement Balance Sheet Statement of CF Analysis The balance sheet is the accounting equation: Assets = Liabilities + Equity. Each asset and liability account is reported separately on the balance sheet. The unadjusted, adjusted, or post-closing balances will appear for each account, based on your selection. (Enter the balance sheet items in the order of liquidity.) Show less A ***** Post-closing Pacillo Security Services, Inc. Balance Sheet At December 31, Year 11 Assets 0 0 0 Llabilities 0 0 IS 0 Stockholders' Equity Total Paid in Capital 0 269,525 269,525 269,525 Total Liabilities and Stockholders' Equity Answer is not complete. Requirement General Journal General Ledger Trial Balance Income Statement Balance Sheet Statement of CF Analysis Prepare the statement of cash flow for year ended December 31, Year 11. (Amounts to deducted should be indicated with a minus sign.). Pacillo Security Services, Inc. Statement of Cash Flowe For the Year Ended December 31, Year 11 Cash flows from operating activities Cash receipts from customers S 253.680 Cash payment for expenses (189,310) Cash Payment for sales tax payable (5,640) Cash payment for interest (9,493) OOOO IS 49.237 Net cash flow from operating activities Cash flows from investing activities: Net cash flows from investing activities Cash flows from financing activities: Cash inflow from stock issue Cash payment on notes payable Cash payments for dividends OOO 92,000 (7,745) (17,500) Net cash flow from financing activities Net increase in cash Add: Beginning cash balance Ending cash balance 66.755 115.992 113.718 229.710 IS Answer is not complete. Requirement General Journal General Ledger Trial Balance Income Statement Balance Sheet Statement of CF Analysis Indicate whether the transaction increases (+), decreases (-), or increases and decreases (+/-) for each element of the financial statements. Also, in the Cash Flow column, use the letters OA to designate operating activity, IA for investing activity, FA for financing activity. When more than one activity can be correct response, select from options "FA or IA", "IA or OA", "OA or FA. The first transaction is recorded as an example. Show less A Pacillo Security Services, Inc. Effect of Transactions on Financial Statements - Year 11 Balance Sheet Income Statement Llabilities Revenue Equity Expenses Statement of Cash Flows Transaction Net Income Assets OA 1. 2. ol OA lololo FA FA OOO 5. G. + OA * 3 x x 7. 8. 9. O OO + 10. x OA OA 11. 12 + lolo OA OA 13 x X 14 BOBO 15. 16 17. OOO OOOOO + x X x 18 + + 19. 20 OOOOOOOO OA OA OA OA OA OA OA DE FA 21 + + 22 . + 23 24 25. O OOOOOOO + OOOOOOOO ololololololo + 26 + 27. + + 28 29. 30. OO +Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Analytical Finance Volume I

Authors: Jan R. M. Röman

1st Edition

3319340263, 978-3319340265