Answered step by step

Verified Expert Solution

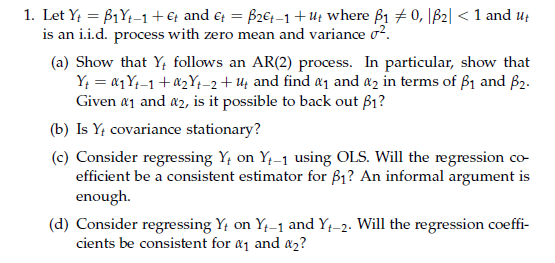

Question

1 Approved Answer

Hello, I'm stuck with point C and D of this exercise. Is anyone who can help me? An explanation would be great. If it's easier

Hello, I'm stuck with point C and D of this exercise. Is anyone who can help me? An explanation would be great.

If it's easier for you, reply with an image of your notes, no need to write with LaTex

Thanks in advance

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

College Algebra

Authors: Margaret L. Lial, John Hornsby, David I. Schneider, Callie Daniels

12th edition