..Help me answer the following questions.,,

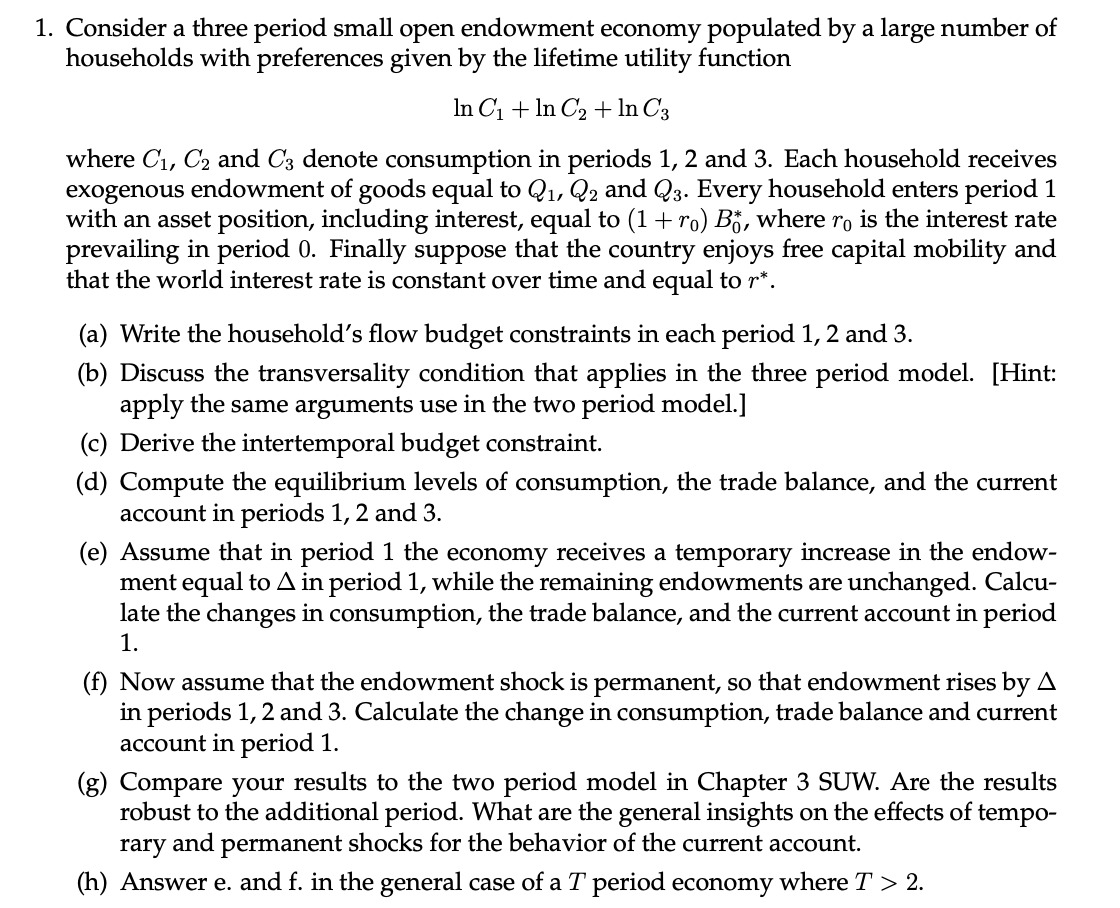

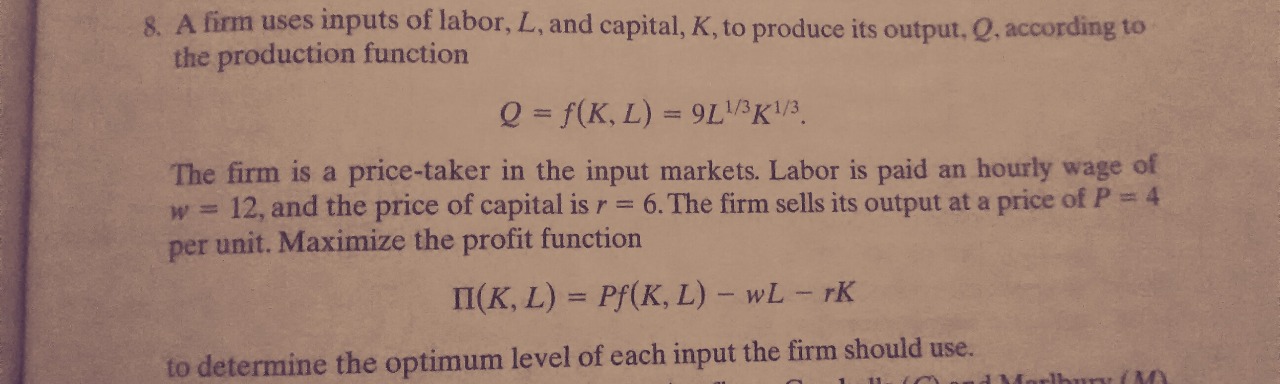

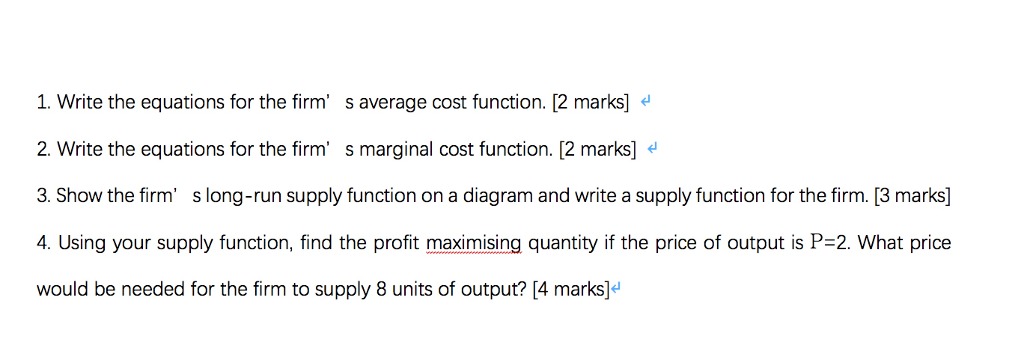

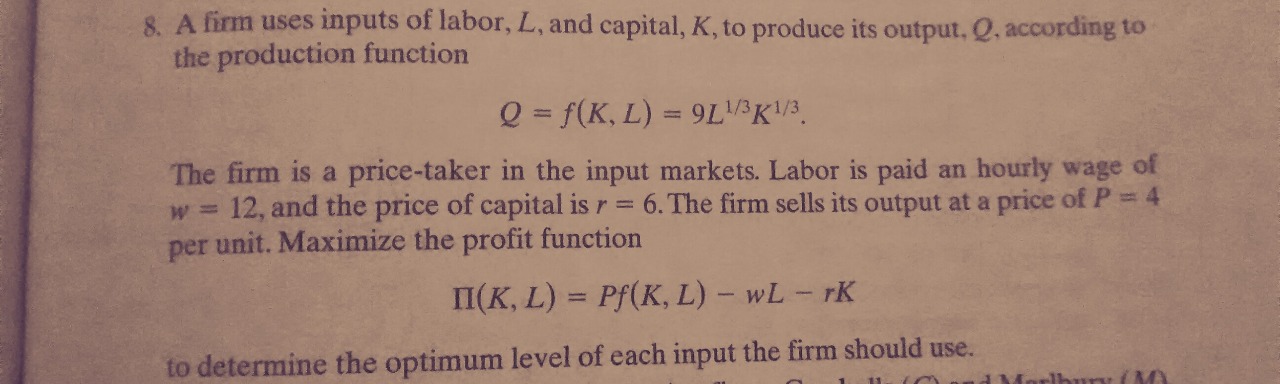

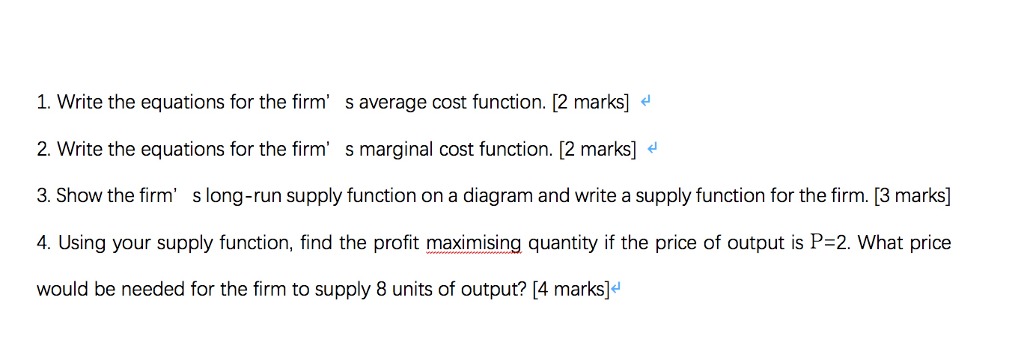

1. Consider a three period small open endowment economy populated by a large number of households with preferences given by the lifetime utility function 11101 +11102 +1DC3 where 01, 02 and 03 denote consumption in periods 1, 2 and 3. Each household receives exogenous endowment of goods equal to Q1, Q2 and Q3. Every household enters period 1 with an asset position, including interest, equal to (1 + r0) 33, where m is the interest rate prevailing in period 0. Finally suppose that the country enjoys free capital mobility and that the world interest rate is constant over time and equal to r". (a) Write the household's ow budget constraints in each period 1, 2 and 3. (b) Discuss the transversality condition that applies in the three period model. [I-Iint: apply the same arguments use in the two period model.] (C) Derive the intertemporal budget constraint. (d) Compute the equilibrium levels of consumption, the trade balance, and the current account in periods 1, 2 and 3. (e) Assume that in period 1 the economy receives a temporary increase in the endow- ment equal to A in period 1, while the remaining endowments are unchanged. Calcu- late the changes in consumption, the trade balance, and the current account in period 1. (1') Now assume that the endowment shock is permanent, so that endowment rises by A in periods 1, 2 and 3. Calculate the change in consumption, trade balance and current account in period 1. (g) Compare your results to the two period model in Chapter 3 SUW. Are the results robust to the additional period. What are the general insights on the effects of tempo- rary and permanent shocks for the behavior of the current account. (11) Answer e. and f. in the general case of a T period economy where T > 2. 8. A firm uses inputs of labor, L, and capital, K, to produce its output, Q, according to the production function Q = f(K, L) = 91 1/3K1/3. The firm is a price-taker in the input markets. Labor is paid an hourly wage of w = 12, and the price of capital is r = 6. The firm sells its output at a price of P = 4 per unit. Maximize the profit function I(K, L) = Pf(K, L) - WL - rK to determine the optimum level of each input the firm should use.A competitive firm uses two inputs, capital (k) and labour (), to produce one output, (y). The price of capital, Wk, is $1 per unit and the price of labor, WI, is $1 per unit. The firm operates in competitive markets for outputs and inputs, so takes the prices as given. The production function is f (k, [) = k0.25 10.5. The maximum amount of output produced for a given amount of inputs is y = f (k, 1) units.1. Write the equations for the firm' 5 average cost function. [2 marks] 6' 2. Write the equations for the firm' 5 marginal cost function. [2 marks] (4 3. Show the rm\" 5 long-run supply function on a diagram and write a supply function for the firm. [3 marks] 4. Using your supply function, nd the prot maximising quantity if the price of output is P=2. What price would be needed for the firm to supply 8 units of output? [4 marks]