Answered step by step

Verified Expert Solution

Question

1 Approved Answer

HELP PLEASEE! The beginning inventory for Dunne Co, and data on purchases and sales for a three-month period are as follows: requirea: 1. Rlecord the

HELP PLEASEE!

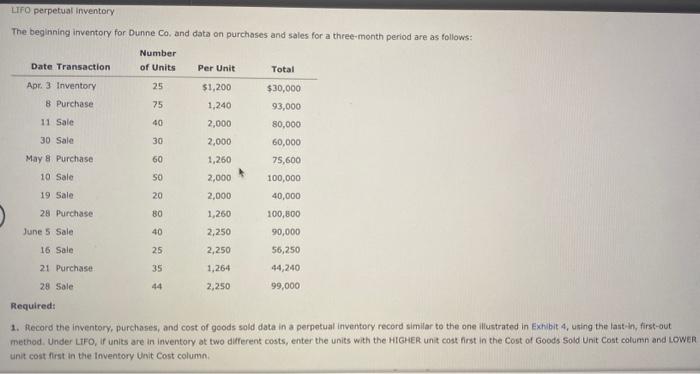

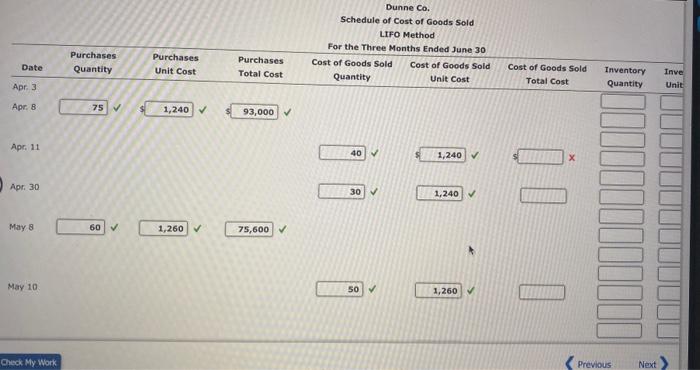

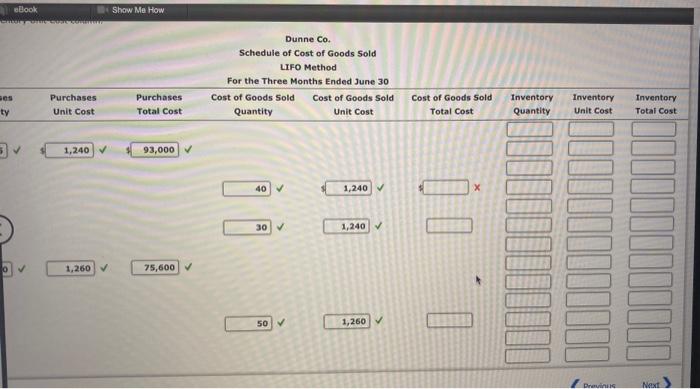

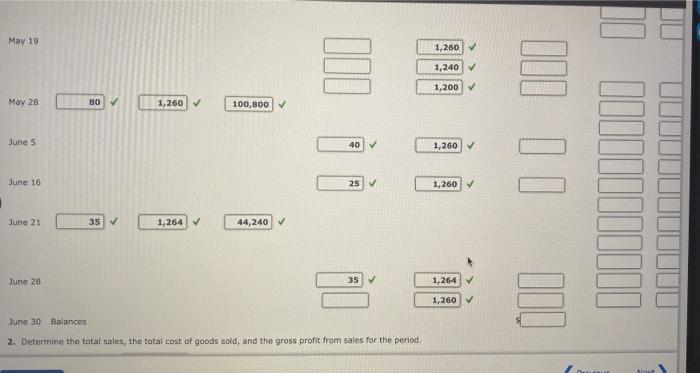

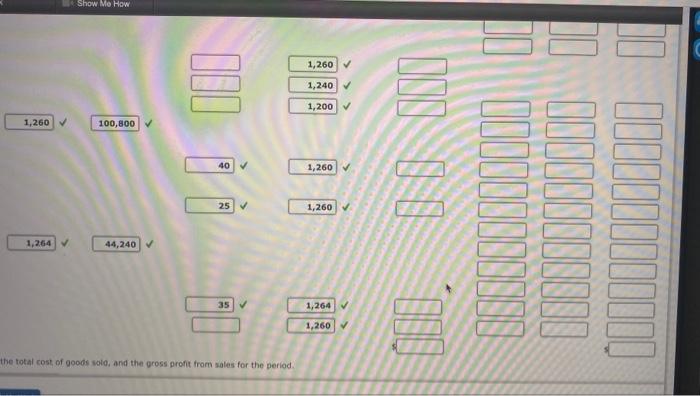

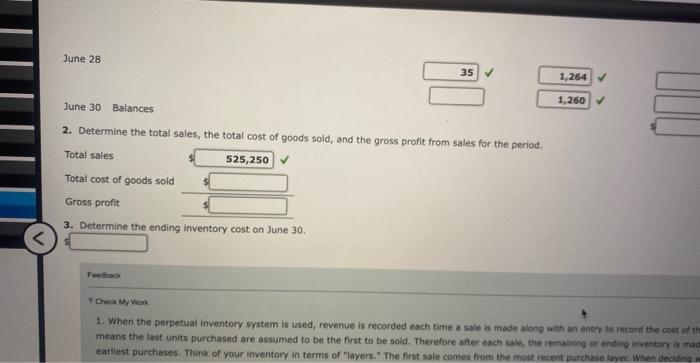

The beginning inventory for Dunne Co, and data on purchases and sales for a three-month period are as follows: requirea: 1. Rlecord the inventory, purchases, and cost of goods sold data in a perpotual inventory record similar to the one illustrated in Exhibit 4 , using the last-in, first-out method. Under LIFO, if units are in inventory at two different costs, enter the units with the HIGHER unit cost first in the Cost of Goods Sold Unit cost columin and LOWER unit cost first in the Inventory Unit Cost column. Dunne Co. Schedule of Cost of Goods Sold Dunne Co. Schedule of Cost of Goods Sold LIFO Method May 19 June 5 June 16 June 21 June 7.5 June 30 Balances: 2. Determine the total sales, the total cost of goods sold, and the gross profit from sales for the period. 1,260 100,800 2. Determine the total sales, the total cost of goods sold, and the gross profit from sales for the period. 3. Determine the ending inventory cost on June 30 . Feethack - Check My wore 1. When the perpetual inventory system is used, revenue is recorded each time a sale is made along with an entry to ricord the cort of 1 means the last units purchased are assumed to be the first to be sold. Therefore after each sale, the remaining or ending inventory is ma earliest purchases. Think of your inventory in terms of "layers." The first sale comes trom the most recent purchase layee When decidine Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamental accounting principle

Authors: John J. Wild, Ken W. Shaw, Barbara Chiappetta

21st edition

1259119831, 9781259311703, 978-1259119835, 1259311708, 978-0078025587