Answered step by step

Verified Expert Solution

Question

1 Approved Answer

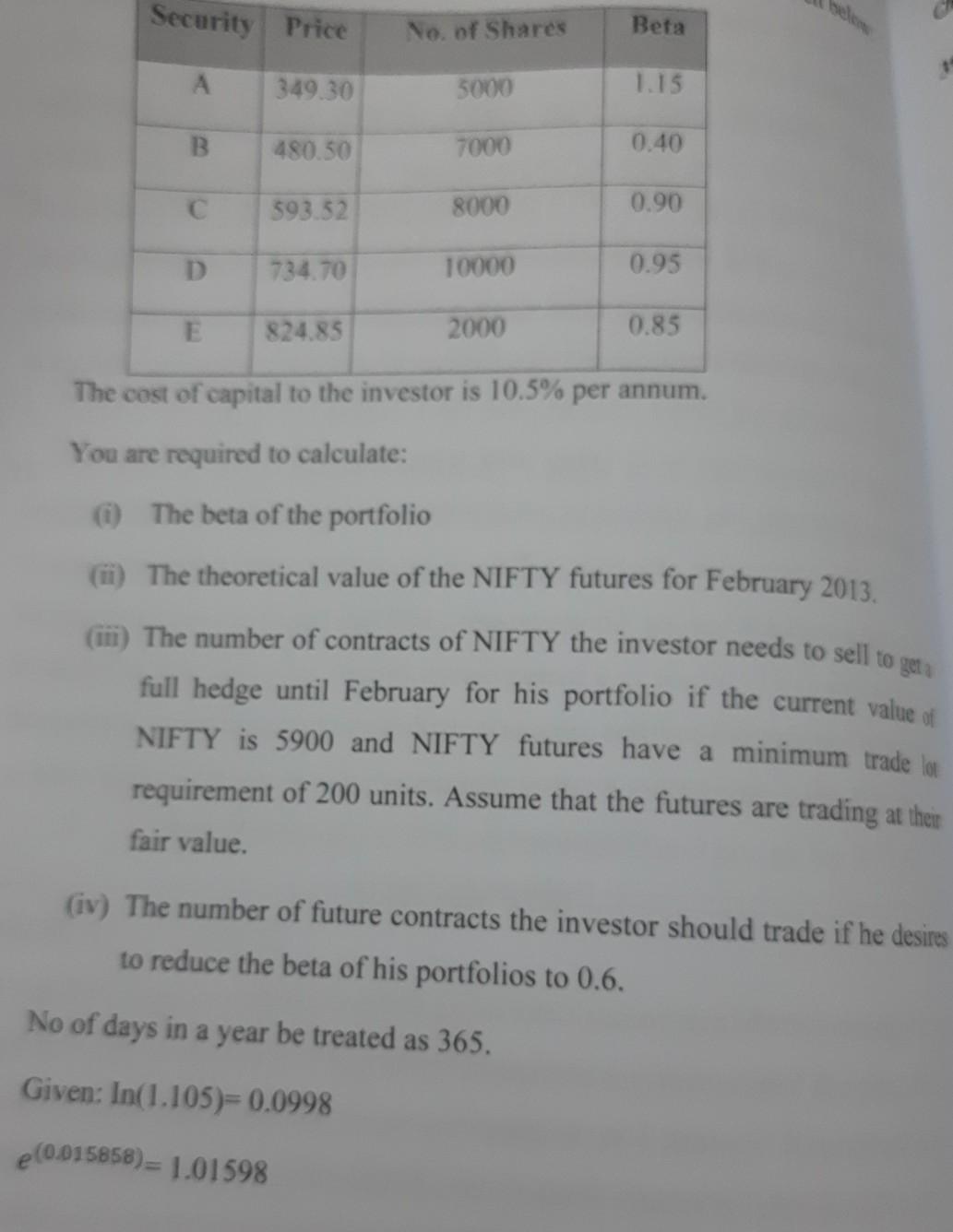

help Security Price No. of Shares Beta A 349.30 5000 1.15 B 480.50 7000 0.40 C $93.52 8000 0.90 D 734.70 10000 0.95 824.85 2000

help

Security Price No. of Shares Beta A 349.30 5000 1.15 B 480.50 7000 0.40 C $93.52 8000 0.90 D 734.70 10000 0.95 824.85 2000 0.85 The cost of capital to the investor is 10.5% per annum. You are required to calculate: (i) The beta of the portfolio (1) The theoretical value of the NIFTY futures for February 2013 (ii) The number of contracts of NIFTY the investor needs to sell to gera full hedge until February for his portfolio if the current value of NIFTY is 5900 and NIFTY futures have a minimum trade lo requirement of 200 units. Assume that the futures are trading at their fair value. (iv) The number of future contracts the investor should trade if he desires to reduce the beta of his portfolios to 0.6. No of days in a year be treated as 365. Given: In(1.105)=0.0998 (0.015858) = 1.01598Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Findings Of RAC MAC HAC And PSI Review Process

Authors: Mrs. Jyoti Sharma

1st Edition

1511689609, 978-1511689601