Answered step by step

Verified Expert Solution

Question

1 Approved Answer

help thanks Most changes in accounting principle require a disclosure justifying the change in the first set of financial statements after the change is made.

help thanks

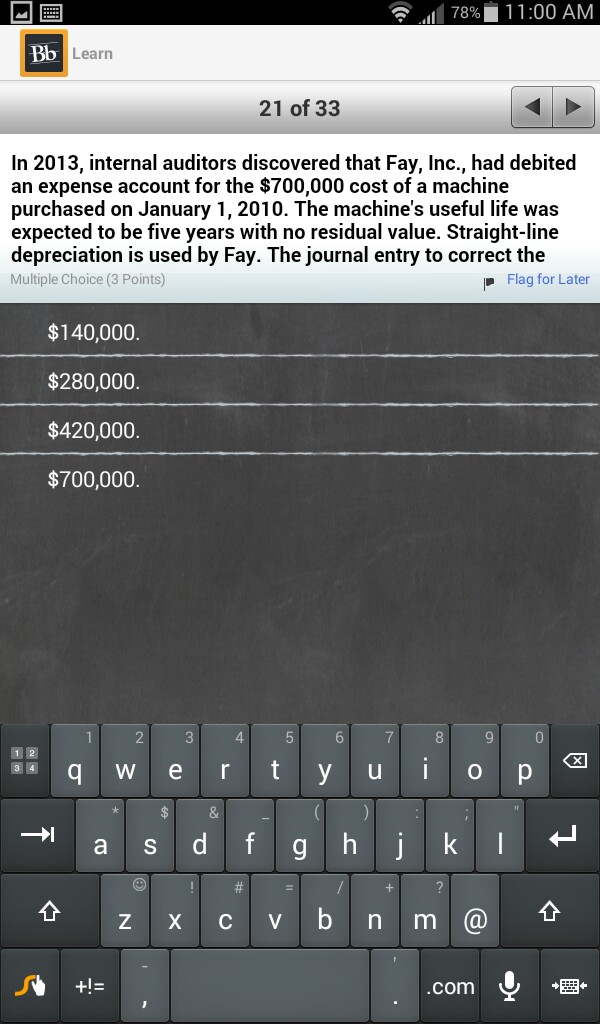

Most changes in accounting principle require a disclosure justifying the change in the first set of financial statements after the change is made. All changes reported using the retrospective approach require prior period adjustments. A change in reporting entity requires note disclosure in all subsequent financial statements prepared for the new entity. In 2013, internal auditors discovered that Fay, Inc. had debited an expense account for the $700,000 cost of a machine purchased on January 1, 2010. The machine's useful life was expected to be five years with no residual value. Straight-line depreciation is used by Fay. The journal entry to correct theStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Research Methods And Audit For General Practice

Authors: David Armstrong, John Grace

3rd Edition

0192631918, 978-0192631916