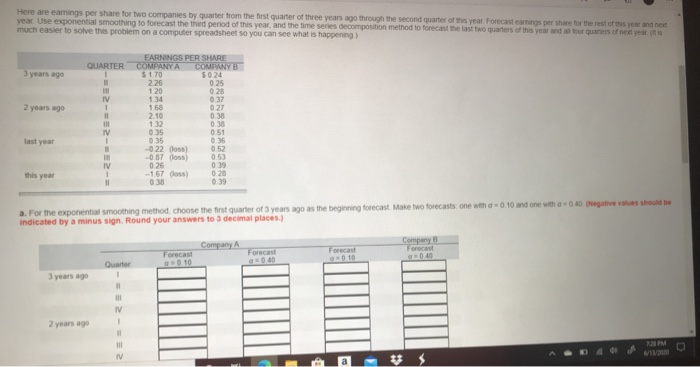

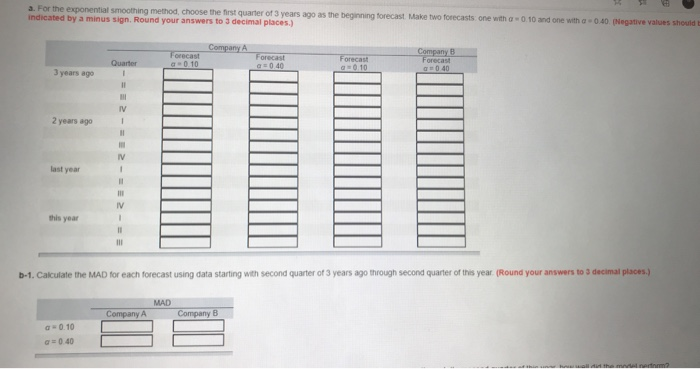

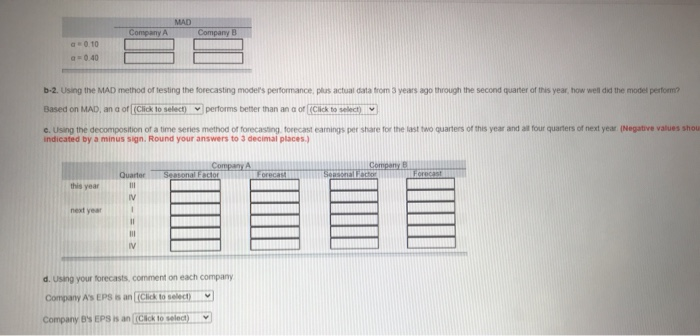

Here are eamings per share for two companies by quarter from the first quarter of three years ago through the second quarter of this year Forecast earnings per share for the rest of this year and next year. Use exponential smoothing to forecast the the period of this year, and the time series decomposition method to forecast the last two quarters of this year and a tour quarters of next year it is much easier to solve this problem on a computer spreadsheet so you can see what is happening 3 years ago 2 years ago - EARNINGS PER SHARE QUARTER COMPANYA COMPANY B 1 $ 170 5024 226 120 025 0.28 IV 134 0:37 168 027 11 2.10 0.38 MV 0.51 035 036 -0 22 (los) -0.87 oss IV 0.26 0.39 1 -167 doss) 020 038 039 0.38 132 last year this year a. For the exponential smoothing method choose the first quarter of 3 years ago as the beginning forecast Make two forecasts one with a = 0.10 and one with 0.40 Negative values should be indicated by a minus sign. Round your answers to 3 decimal places) Company A Company Forecast Forecast Forecast Forecast Quarter 3 years ago - IV - 2 years ago ul M a. For the exponential smoothing method, choose the first quarter of 3 years ago as the beginning forecast. Make two forecasts one with 0.10 and one with a 0.40 (Negative values should indicated by a minus sign. Round your answers to 3 decimal places.) Company A orecast Quarter 010 Forecast G=0.40 Forecast G=0.10 Company B Forecast 040 3 years ago 1 11 IV 2 years ago - MV last year - IV this year 1 11 ll! b-1. Calculate the MAD for each forecast using data starting with second quarter of 3 years ago through second quarter of this year (Round your answers to 3 decimal places.) MAD Company A Company B - 0.10 0.40 MAD Company A Company B q=0.10 q=0.40 b-2. Using the MAD method of testing the forecasting model's performance, plus actual data from 3 years ago through the second quarter of this year, how well did the model perform? Based on MAD, an aof (Click to select) v performs better than an aof (Click to select) e. Using the decomposition of a time series method of forecasting forecast earnings per share for the last two quarters of this year and all four quarters of next year (Negative values shou indicated by a minus sign. Round your answers to 3 decimal places.) Company Seasonal Factor Company Seasonal Factor Forecast Forecast this year Quarter 11 IV 1 next year d. Using your forecasts, comment on each company Company AS EPS is an (Click to select) Company B EPS is an (Click to select Here are earnings per share for two companies by quarter from the first quarter of three years ago through the second quarter of this year Forecast earnings per share for the rest of this year and next year. Use exponential smoothing to forecast the third period of this year, and the time senes decomposition method to forecast the last two quarters of this year and all our quarters of next year (it is much easier to solve this problem on a computer spreadsheet so you can see what is happening) 3 years ago 1 2 years ago EARNINGS PER SHARE QUARTER COMPANY A COMPANY B $ 170 50.24 11 2.26 0.25 111 1.20 0.28 IV 1.34 0.37 1 168 027 2.10 0.30 132 038 IV 035 0.51 1 0.35 0.36 1 022 ) 0.52 -087 (5) 0.53 0.26 0.39 -167 ) 028 0 38 0.39 last year this year a. For the exponential smoothing method choose the first quarter of 3 years ago as the beginning forecast. Make two forecasts one with = 0.10 and one with a 0.40 (Negative values shoul indicated by a minus sign. Round your answers to 3 decimal places.) Company A Quarter Forecast G=0.10 Forecast Company B Forecast Forecast G=0.10 3 years ago 1 il IV 2 years ago - IV 1 11 IV this year 11 b-1. Calculate the MAD for each forecast using data starting with second quarter of 3 years ago through second quarter of this year. (Round your answers to 3 decimal places.) MAD Company A Company B as 0.10 G=0.40 b-2. Using the MAD method of testing the forecasting model's performance, plus actual data from 3 years ago through the second quarter of this year, how well did the model perform? Based on MAD, an aof (Click to select) performs better than ana of Click to select c. Using the decomposition of a time series method of forecasting, forecast earnings per share for the last two quarters of this year and all four quarters of next year (Negative values should indicated by a minus sign. Round your answers to 3 decimal places.) Company A Seasonal Factor Forecast Company B Seasonal Factor this year Forecast Quarter III IV next year -- 11 IV d. Using your forecasts, comment on each company Company A's EPS is an (Click to select) Company B's EPS is an (Click to select) Here are eamings per share for two companies by quarter from the first quarter of three years ago through the second quarter of this year Forecast earnings per share for the rest of this year and next year. Use exponential smoothing to forecast the the period of this year, and the time series decomposition method to forecast the last two quarters of this year and a tour quarters of next year it is much easier to solve this problem on a computer spreadsheet so you can see what is happening 3 years ago 2 years ago - EARNINGS PER SHARE QUARTER COMPANYA COMPANY B 1 $ 170 5024 226 120 025 0.28 IV 134 0:37 168 027 11 2.10 0.38 MV 0.51 035 036 -0 22 (los) -0.87 oss IV 0.26 0.39 1 -167 doss) 020 038 039 0.38 132 last year this year a. For the exponential smoothing method choose the first quarter of 3 years ago as the beginning forecast Make two forecasts one with a = 0.10 and one with 0.40 Negative values should be indicated by a minus sign. Round your answers to 3 decimal places) Company A Company Forecast Forecast Forecast Forecast Quarter 3 years ago - IV - 2 years ago ul M a. For the exponential smoothing method, choose the first quarter of 3 years ago as the beginning forecast. Make two forecasts one with 0.10 and one with a 0.40 (Negative values should indicated by a minus sign. Round your answers to 3 decimal places.) Company A orecast Quarter 010 Forecast G=0.40 Forecast G=0.10 Company B Forecast 040 3 years ago 1 11 IV 2 years ago - MV last year - IV this year 1 11 ll! b-1. Calculate the MAD for each forecast using data starting with second quarter of 3 years ago through second quarter of this year (Round your answers to 3 decimal places.) MAD Company A Company B - 0.10 0.40 MAD Company A Company B q=0.10 q=0.40 b-2. Using the MAD method of testing the forecasting model's performance, plus actual data from 3 years ago through the second quarter of this year, how well did the model perform? Based on MAD, an aof (Click to select) v performs better than an aof (Click to select) e. Using the decomposition of a time series method of forecasting forecast earnings per share for the last two quarters of this year and all four quarters of next year (Negative values shou indicated by a minus sign. Round your answers to 3 decimal places.) Company Seasonal Factor Company Seasonal Factor Forecast Forecast this year Quarter 11 IV 1 next year d. Using your forecasts, comment on each company Company AS EPS is an (Click to select) Company B EPS is an (Click to select Here are earnings per share for two companies by quarter from the first quarter of three years ago through the second quarter of this year Forecast earnings per share for the rest of this year and next year. Use exponential smoothing to forecast the third period of this year, and the time senes decomposition method to forecast the last two quarters of this year and all our quarters of next year (it is much easier to solve this problem on a computer spreadsheet so you can see what is happening) 3 years ago 1 2 years ago EARNINGS PER SHARE QUARTER COMPANY A COMPANY B $ 170 50.24 11 2.26 0.25 111 1.20 0.28 IV 1.34 0.37 1 168 027 2.10 0.30 132 038 IV 035 0.51 1 0.35 0.36 1 022 ) 0.52 -087 (5) 0.53 0.26 0.39 -167 ) 028 0 38 0.39 last year this year a. For the exponential smoothing method choose the first quarter of 3 years ago as the beginning forecast. Make two forecasts one with = 0.10 and one with a 0.40 (Negative values shoul indicated by a minus sign. Round your answers to 3 decimal places.) Company A Quarter Forecast G=0.10 Forecast Company B Forecast Forecast G=0.10 3 years ago 1 il IV 2 years ago - IV 1 11 IV this year 11 b-1. Calculate the MAD for each forecast using data starting with second quarter of 3 years ago through second quarter of this year. (Round your answers to 3 decimal places.) MAD Company A Company B as 0.10 G=0.40 b-2. Using the MAD method of testing the forecasting model's performance, plus actual data from 3 years ago through the second quarter of this year, how well did the model perform? Based on MAD, an aof (Click to select) performs better than ana of Click to select c. Using the decomposition of a time series method of forecasting, forecast earnings per share for the last two quarters of this year and all four quarters of next year (Negative values should indicated by a minus sign. Round your answers to 3 decimal places.) Company A Seasonal Factor Forecast Company B Seasonal Factor this year Forecast Quarter III IV next year -- 11 IV d. Using your forecasts, comment on each company Company A's EPS is an (Click to select) Company B's EPS is an (Click to select)