Here is the data

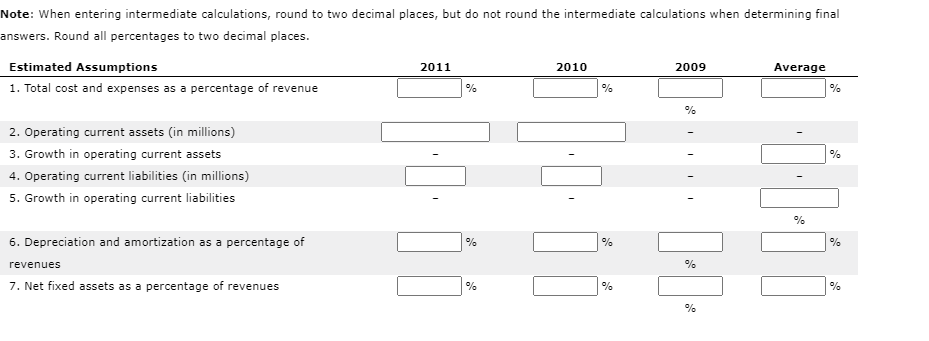

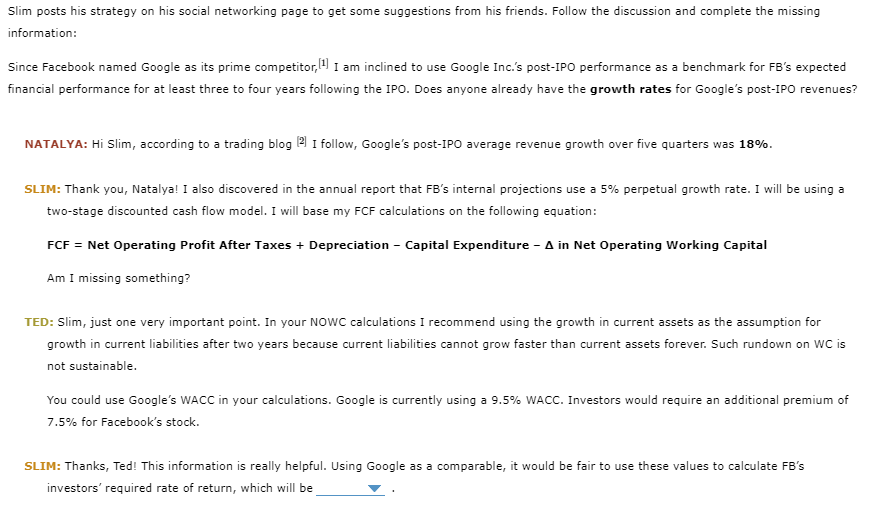

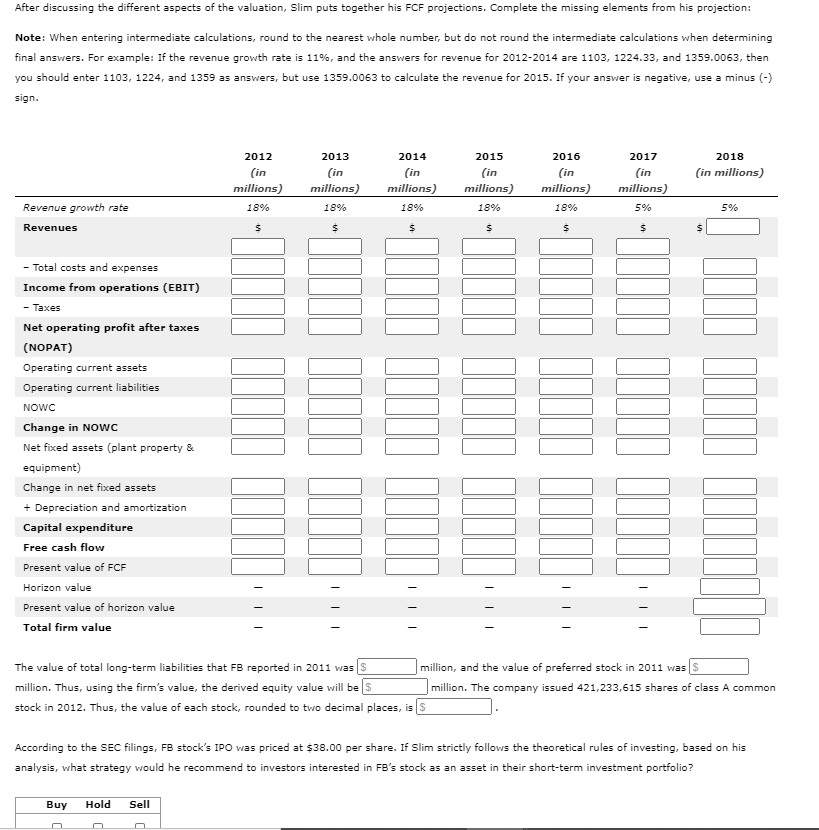

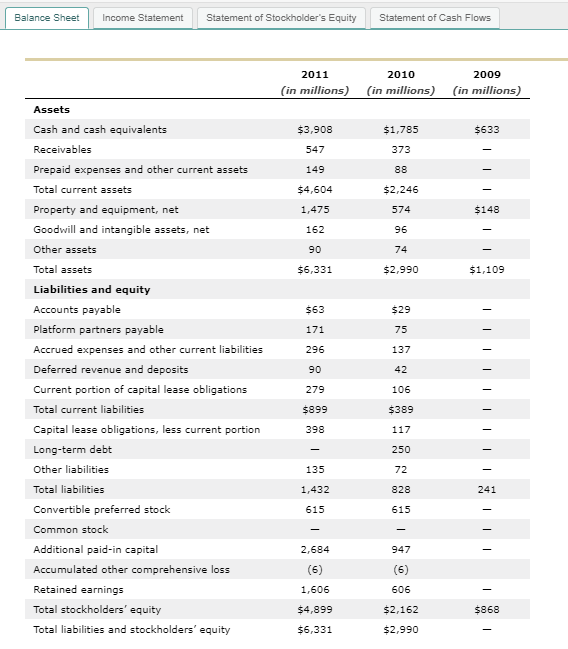

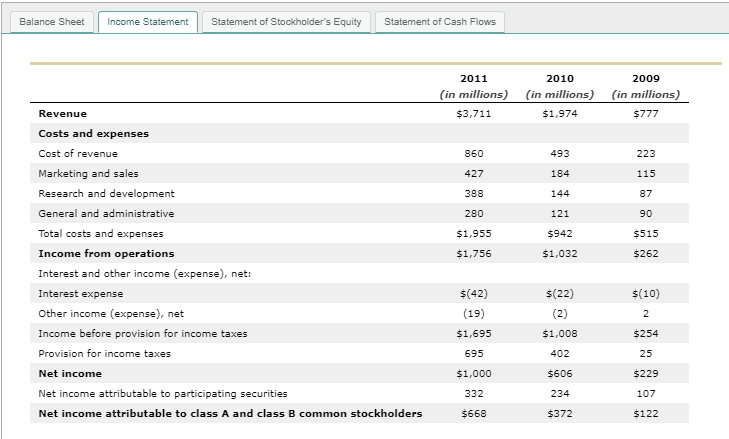

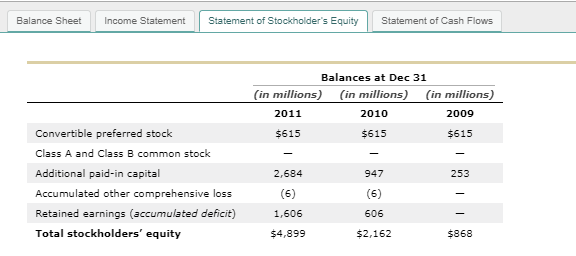

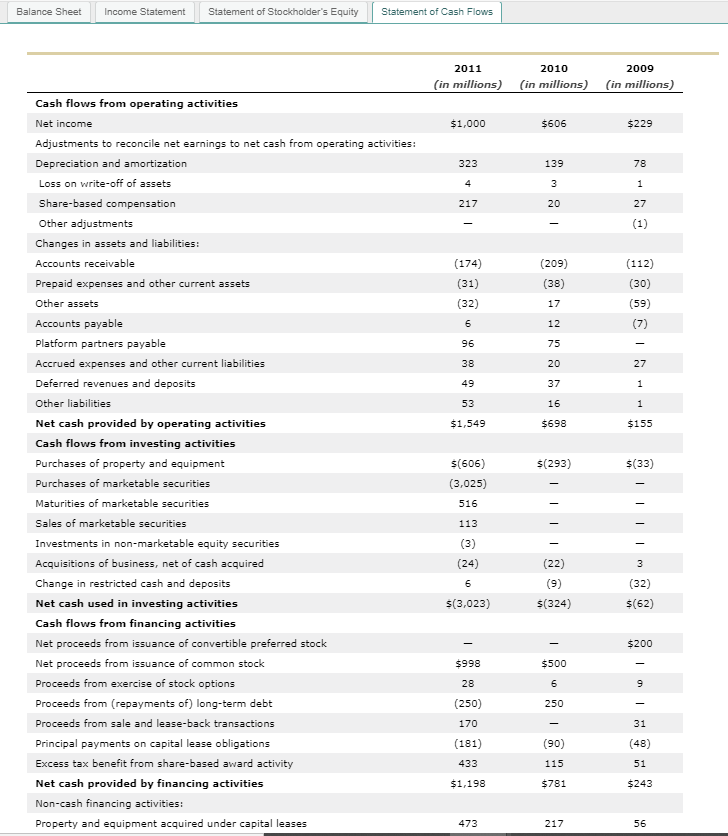

Attempts: Keep the Highest: /5 1. Stock valuation - A comparison of estimated values and marketprices Slim Perkins, a business journalist, is a recent hire at his firm. Since he joined the firm, he has been following Facebook Inc.'s (FB) initial public offering (IPO) and the stock's performance. His task is to estimate Facebook's fair market value, also referred to as "intrinsic" value, and compare value with the current stock price, and recommend a buy, sell, or hold rating to investors. Slim pulls the company's consolidated financial statements to collect relevant data on the company's historical financial performance. He notices that the company assumes a 45% marginal tax rate after the IPO, and mentions that the company projects that user rates and revenue growth will decline over time. Slim starts his evaluation by calculating ratios of costs and expenses to revenues, interest expense to revenues, and others that will form the set of assumptions in his analysis which will be used to calculate free cash flows. 421,233,615 Shares FACEBOOK CLASS A COMMON STOCK Note: When entering intermediate calculations, round to two decimal places, but do not round the intermediate calculations when determining final answers. Round all percentages to two decimal places. 2011 2010 2009 Average Estimated Assumptions 1. Total cost and expenses as a percentage of revenue % - 2. Operating current assets (in millions) 3. Growth in operating current assets 4. Operating current liabilities (in millions) 5. Growth in operating current liabilities 6. Depreciation and amortization as a percentage of % % % revenues % 7. Net fixed assets as a percentage of revenues % % Slim posts his strategy on his social networking page to get some suggestions from his friends. Follow the discussion and complete the missing information: Since Facebook named Google as its prime competitor, [1] I am inclined to use Google Inc.'s post-IPO performance as a benchmark for FB's expected financial performance for at least three to four years following the IPO. Does anyone already have the growth rates for Google's post-IPO revenues? NATALYA: Hi Slim, according to a trading blog 2) I follow, Google's post-IPO average revenue growth over five quarters was 18%. SLIM: Thank you, Natalya! I also discovered in the annual report that FB's internal projections use a 5% perpetual growth rate. I will be using a two-stage discounted cash flow model. I will base my FCF calculations on the following equation: FCF = Net Operating Profit After Taxes + Depreciation - Capital Expenditure - A in Net Operating Working Capital Am I missing something? TED: Slim, just one very important point. In your NOWC calculations I recommend using the growth in current assets as the assumption for growth in current liabilities after two years because current liabilities cannot grow faster than current assets forever. Such rundown on WC is not sustainable. You could use Google's WACC in your calculations. Google is currently using a 9.5% WACC. Investors would require an additional premium of 7.5% for Facebook's stock. SLIM: Thanks, Ted! This information is really helpful. Using Google as a comparable, it would be fair to use these values to calculate FB's investors' required rate of return, which will be After discussing the different aspects of the valuation, Slim puts together his FCF projections. Complete the missing elements from his projection: Note: When entering intermediate calculations, round to the nearest whole number, but do not round the intermediate calculations when determining final answers. For example: If the revenue growth rate is 11%, and the answers for revenue for 2012-2014 are 1103, 1224.33, and 1359.0063, then you should enter 1103, 1224, and 1359 as answers, but use 1359.0063 to calculate the revenue for 2015. If your answer is negative, use a minus (-) sign. 2015 2012 (in millions) 18% 2018 (in millions) 2013 (in millions) 18% 2014 (in millions) 18% 2017 (in millions) 5% 2016 (in millions) 18% millions) 18% 5% Revenue growth rate Revenues $ $ $ $ $ $ - Total costs and expenses Income from operations (EBIT) - Taxes Net operating profit after taxes (NOPAT) Operating current assets Operating current liabilities NOWC Change in NOWC Net fixed assets (plant property & equipment) Change in net fixed assets + Depreciation and amortization Capital expenditure Free cash flow Present value of FCF Horizon value Present value of horizon value Total firm value The value of total long-term liabilities that FB reported in 2011 was $ million. Thus, using the firm's value, the derived equity value will be s stock in 2012. Thus, the value of each stock, rounded to two decimal places, is million, and the value of preferred stock in 2011 was $ million. The company issued 421,233,615 shares of class A common According to the SEC filings, FB stock's IPO was priced at $38.00 per share. If Slim strictly follows the theoretical rules of investing, based on his analysis, what strategy would he recommend to investors interested in FB's stock as an asset in their short-term investment portfolio? Buy Hold Sell Balance Sheet Income Statement Statement of Stockholder's Equity Statement of Cash Flows 2011 (in millions) 2010 (in millions) 2009 (in millions) $3.908 $1,785 $633 547 373 149 88 $4,604 $2,246 1,475 574 $148 162 96 90 74 $6,331 $2.990 $1,109 $63 $29 171 75 296 137 Assets Cash and cash equivalents Receivables Prepaid expenses and other current assets Total current assets Property and equipment, net Goodwill and intangible assets, net Other assets Total assets Liabilities and equity Accounts payable Platform partners payable Accrued expenses and other current liabilities Deferred revenue and deposits Current portion of capital lease obligations Total current liabilities Capital lease obligations, less current portion Long-term debt Other liabilities Total liabilities Convertible preferred stock Common stock Additional paid-in capital Accumulated other comprehensive loss Retained earnings Total stockholders' equity Total liabilities and stockholders' equity 90 42 279 106 $899 $389 398 117 250 135 72 1,432 828 241 615 615 2,684 947 (6) 1,606 606 $4,899 $2,162 $868 $6,331 $2,990 Balance Sheet Income Statement Statement of Stockholder's Equity Statement of Cash Flows 2011 (in millions) $3,711 2010 (in millions) $1,974 2009 (in millions) $777 Revenue Costs and expenses 860 493 223 427 184 115 388 144 87 280 121 90 $1,955 $942 $515 $1,756 $1,032 $262 Cost of revenue Marketing and sales Research and development General and administrative Total costs and expenses Income from operations Interest and other income (expense), net: Interest expense Other income (expense), net Income before provision for income taxes Provision for income taxes Net income Net income attributable to participating securities Net income attributable to class A and class B common stockholders $(42) (19) $(22) (2) $1,008 $(10) 2 $1,695 $254 695 402 25 $1,000 $606 $229 332 234 107 $668 $372 $122 Balance Sheet Income Statement Statement of Stockholder's Equity Statement of Cash Flows Balances at Dec 31 (in millions) (in millions) (in millions) 2011 2010 2009 $615 $615 $615 2,684 947 253 Convertible preferred stock Class A and Class B common stock Additional paid-in capital Accumulated other comprehensive loss Retained earnings (accumulated deficit) Total stockholders' equity (6) 1,606 606 $4,899 $2,162 $868 Balance Sheet Income Statement Statement of Stockholder's Equity Statement of Cash Flows 2011 2010 (in millions) (in millions) 2009 (in millions) Cash flows from operating activities Net income $1,000 $606 $229 323 139 78 4 3 1 217 20 27 Adjustments to reconcile net earnings to net cash from operating activities: Depreciation and amortization Loss on write-off of assets Share-based compensation Other adjustments Changes in assets and liabilities: Accounts receivable Prepaid expenses and other current assets (1) (209) (38) (174) (31) (32) 6 (112) (30) (59) (7) Other assets 17 12 96 75 38 20 27 49 37 1 53 16 1 $1,549 $698 $155 s(293) $(33) $(606) (3,025) 516 113 (3) (24) (22) 3 Accounts payable Platform partners payable Accrued expenses and other current liabilities Deferred revenues and deposits Other liabilities Net cash provided by operating activities Cash flows from investing activities Purchases of property and equipment Purchases of marketable securities Maturities of marketable securities Sales of marketable securities Investments in non-marketable equity securities Acquisitions of business, net of cash acquired Change in restricted cash and deposits Net cash used in investing activities Cash flows from financing activities Net proceeds from issuance of convertible preferred Net proceeds from issuance of common stock Proceeds from exercise of stock options Proceeds from (repayments of) long-term debt Proceeds from sale and lease-back transactions Principal payments on capital lease obligations Excess tax benefit from share-based award activity Net cash provided by financing activities Non-cash financing activities: Property and equipment acquired under capital leases 6 (9) (32) $(62) $(3,023) $(324) $200 $998 $500 28 6 250 (250) 170 31 (181) (90) (48) 433 115 51 $1,198 $781 $243 473 217 56 Attempts: Keep the Highest: /5 1. Stock valuation - A comparison of estimated values and marketprices Slim Perkins, a business journalist, is a recent hire at his firm. Since he joined the firm, he has been following Facebook Inc.'s (FB) initial public offering (IPO) and the stock's performance. His task is to estimate Facebook's fair market value, also referred to as "intrinsic" value, and compare value with the current stock price, and recommend a buy, sell, or hold rating to investors. Slim pulls the company's consolidated financial statements to collect relevant data on the company's historical financial performance. He notices that the company assumes a 45% marginal tax rate after the IPO, and mentions that the company projects that user rates and revenue growth will decline over time. Slim starts his evaluation by calculating ratios of costs and expenses to revenues, interest expense to revenues, and others that will form the set of assumptions in his analysis which will be used to calculate free cash flows. 421,233,615 Shares FACEBOOK CLASS A COMMON STOCK Note: When entering intermediate calculations, round to two decimal places, but do not round the intermediate calculations when determining final answers. Round all percentages to two decimal places. 2011 2010 2009 Average Estimated Assumptions 1. Total cost and expenses as a percentage of revenue % - 2. Operating current assets (in millions) 3. Growth in operating current assets 4. Operating current liabilities (in millions) 5. Growth in operating current liabilities 6. Depreciation and amortization as a percentage of % % % revenues % 7. Net fixed assets as a percentage of revenues % % Slim posts his strategy on his social networking page to get some suggestions from his friends. Follow the discussion and complete the missing information: Since Facebook named Google as its prime competitor, [1] I am inclined to use Google Inc.'s post-IPO performance as a benchmark for FB's expected financial performance for at least three to four years following the IPO. Does anyone already have the growth rates for Google's post-IPO revenues? NATALYA: Hi Slim, according to a trading blog 2) I follow, Google's post-IPO average revenue growth over five quarters was 18%. SLIM: Thank you, Natalya! I also discovered in the annual report that FB's internal projections use a 5% perpetual growth rate. I will be using a two-stage discounted cash flow model. I will base my FCF calculations on the following equation: FCF = Net Operating Profit After Taxes + Depreciation - Capital Expenditure - A in Net Operating Working Capital Am I missing something? TED: Slim, just one very important point. In your NOWC calculations I recommend using the growth in current assets as the assumption for growth in current liabilities after two years because current liabilities cannot grow faster than current assets forever. Such rundown on WC is not sustainable. You could use Google's WACC in your calculations. Google is currently using a 9.5% WACC. Investors would require an additional premium of 7.5% for Facebook's stock. SLIM: Thanks, Ted! This information is really helpful. Using Google as a comparable, it would be fair to use these values to calculate FB's investors' required rate of return, which will be After discussing the different aspects of the valuation, Slim puts together his FCF projections. Complete the missing elements from his projection: Note: When entering intermediate calculations, round to the nearest whole number, but do not round the intermediate calculations when determining final answers. For example: If the revenue growth rate is 11%, and the answers for revenue for 2012-2014 are 1103, 1224.33, and 1359.0063, then you should enter 1103, 1224, and 1359 as answers, but use 1359.0063 to calculate the revenue for 2015. If your answer is negative, use a minus (-) sign. 2015 2012 (in millions) 18% 2018 (in millions) 2013 (in millions) 18% 2014 (in millions) 18% 2017 (in millions) 5% 2016 (in millions) 18% millions) 18% 5% Revenue growth rate Revenues $ $ $ $ $ $ - Total costs and expenses Income from operations (EBIT) - Taxes Net operating profit after taxes (NOPAT) Operating current assets Operating current liabilities NOWC Change in NOWC Net fixed assets (plant property & equipment) Change in net fixed assets + Depreciation and amortization Capital expenditure Free cash flow Present value of FCF Horizon value Present value of horizon value Total firm value The value of total long-term liabilities that FB reported in 2011 was $ million. Thus, using the firm's value, the derived equity value will be s stock in 2012. Thus, the value of each stock, rounded to two decimal places, is million, and the value of preferred stock in 2011 was $ million. The company issued 421,233,615 shares of class A common According to the SEC filings, FB stock's IPO was priced at $38.00 per share. If Slim strictly follows the theoretical rules of investing, based on his analysis, what strategy would he recommend to investors interested in FB's stock as an asset in their short-term investment portfolio? Buy Hold Sell Balance Sheet Income Statement Statement of Stockholder's Equity Statement of Cash Flows 2011 (in millions) 2010 (in millions) 2009 (in millions) $3.908 $1,785 $633 547 373 149 88 $4,604 $2,246 1,475 574 $148 162 96 90 74 $6,331 $2.990 $1,109 $63 $29 171 75 296 137 Assets Cash and cash equivalents Receivables Prepaid expenses and other current assets Total current assets Property and equipment, net Goodwill and intangible assets, net Other assets Total assets Liabilities and equity Accounts payable Platform partners payable Accrued expenses and other current liabilities Deferred revenue and deposits Current portion of capital lease obligations Total current liabilities Capital lease obligations, less current portion Long-term debt Other liabilities Total liabilities Convertible preferred stock Common stock Additional paid-in capital Accumulated other comprehensive loss Retained earnings Total stockholders' equity Total liabilities and stockholders' equity 90 42 279 106 $899 $389 398 117 250 135 72 1,432 828 241 615 615 2,684 947 (6) 1,606 606 $4,899 $2,162 $868 $6,331 $2,990 Balance Sheet Income Statement Statement of Stockholder's Equity Statement of Cash Flows 2011 (in millions) $3,711 2010 (in millions) $1,974 2009 (in millions) $777 Revenue Costs and expenses 860 493 223 427 184 115 388 144 87 280 121 90 $1,955 $942 $515 $1,756 $1,032 $262 Cost of revenue Marketing and sales Research and development General and administrative Total costs and expenses Income from operations Interest and other income (expense), net: Interest expense Other income (expense), net Income before provision for income taxes Provision for income taxes Net income Net income attributable to participating securities Net income attributable to class A and class B common stockholders $(42) (19) $(22) (2) $1,008 $(10) 2 $1,695 $254 695 402 25 $1,000 $606 $229 332 234 107 $668 $372 $122 Balance Sheet Income Statement Statement of Stockholder's Equity Statement of Cash Flows Balances at Dec 31 (in millions) (in millions) (in millions) 2011 2010 2009 $615 $615 $615 2,684 947 253 Convertible preferred stock Class A and Class B common stock Additional paid-in capital Accumulated other comprehensive loss Retained earnings (accumulated deficit) Total stockholders' equity (6) 1,606 606 $4,899 $2,162 $868 Balance Sheet Income Statement Statement of Stockholder's Equity Statement of Cash Flows 2011 2010 (in millions) (in millions) 2009 (in millions) Cash flows from operating activities Net income $1,000 $606 $229 323 139 78 4 3 1 217 20 27 Adjustments to reconcile net earnings to net cash from operating activities: Depreciation and amortization Loss on write-off of assets Share-based compensation Other adjustments Changes in assets and liabilities: Accounts receivable Prepaid expenses and other current assets (1) (209) (38) (174) (31) (32) 6 (112) (30) (59) (7) Other assets 17 12 96 75 38 20 27 49 37 1 53 16 1 $1,549 $698 $155 s(293) $(33) $(606) (3,025) 516 113 (3) (24) (22) 3 Accounts payable Platform partners payable Accrued expenses and other current liabilities Deferred revenues and deposits Other liabilities Net cash provided by operating activities Cash flows from investing activities Purchases of property and equipment Purchases of marketable securities Maturities of marketable securities Sales of marketable securities Investments in non-marketable equity securities Acquisitions of business, net of cash acquired Change in restricted cash and deposits Net cash used in investing activities Cash flows from financing activities Net proceeds from issuance of convertible preferred Net proceeds from issuance of common stock Proceeds from exercise of stock options Proceeds from (repayments of) long-term debt Proceeds from sale and lease-back transactions Principal payments on capital lease obligations Excess tax benefit from share-based award activity Net cash provided by financing activities Non-cash financing activities: Property and equipment acquired under capital leases 6 (9) (32) $(62) $(3,023) $(324) $200 $998 $500 28 6 250 (250) 170 31 (181) (90) (48) 433 115 51 $1,198 $781 $243 473 217 56