Answered step by step

Verified Expert Solution

Question

1 Approved Answer

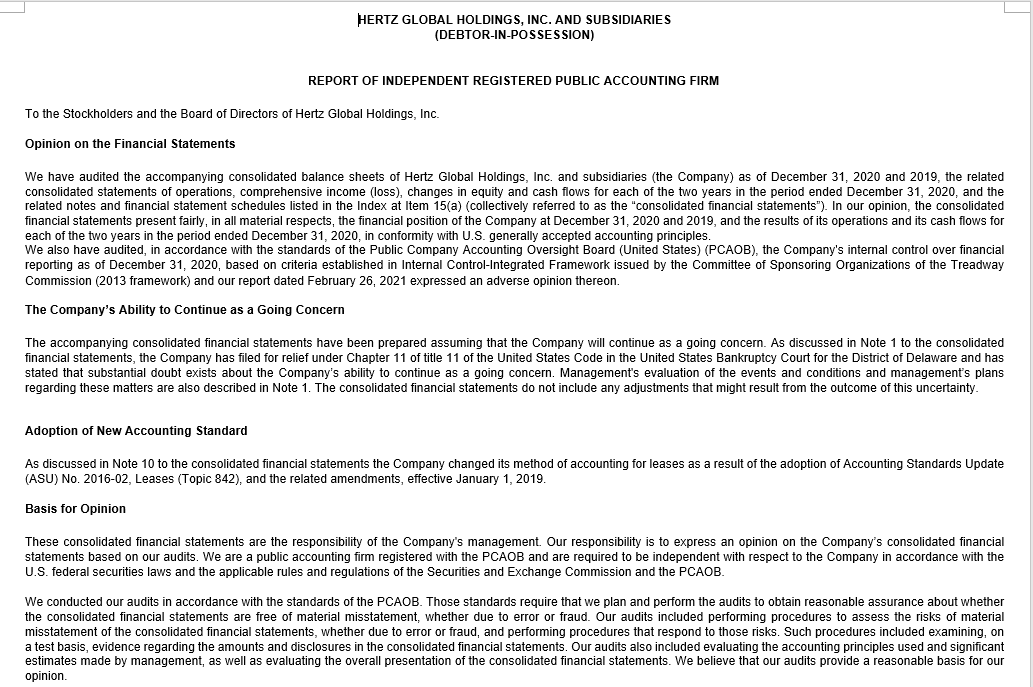

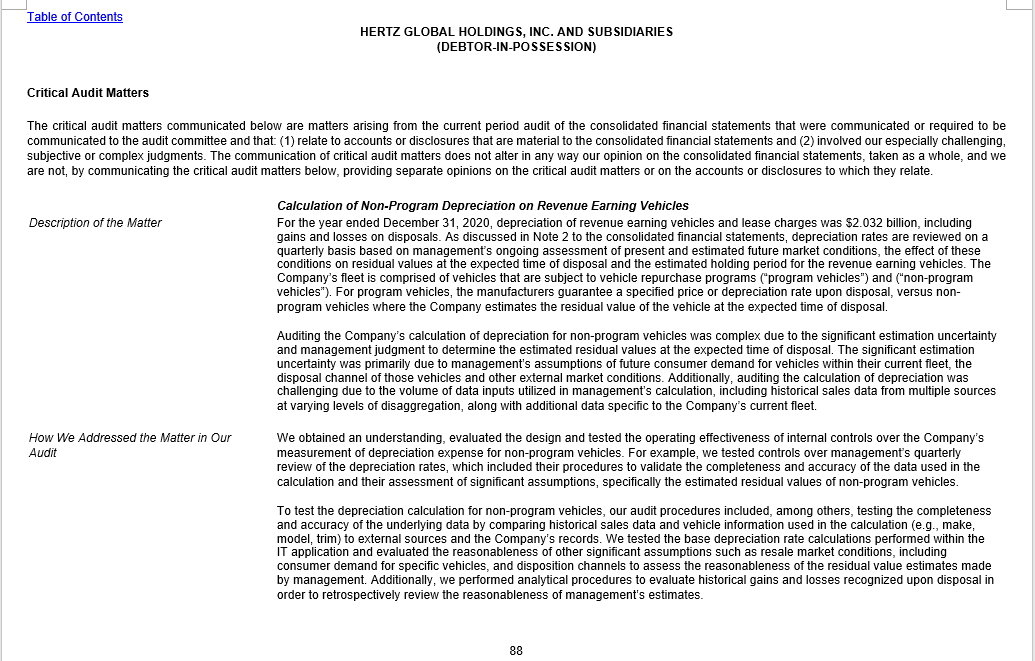

HERTZ GLOBAL HOLDINGS, INC. AND SUBSIDIARIES (DEBTOR-IN-POSSESSION) REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM To the Stockholders and the Board of Directors of Hertz Global

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Practice Of Modern Internal Auditing

Authors: Lawrence B Sawyer

1st Edition

B0006C58OA, 978-0894130120