Hey, It's One Question which has a writing portion. I just need 500 words to answer the question. Everything is provided. Will give thumbs up. I need help with this, please even a little bit of the answer will help me start this.

What information do you need? I posted everything related to the question. Please let me know ASAP, i need this question answered by today please. i will give thumbs up!!

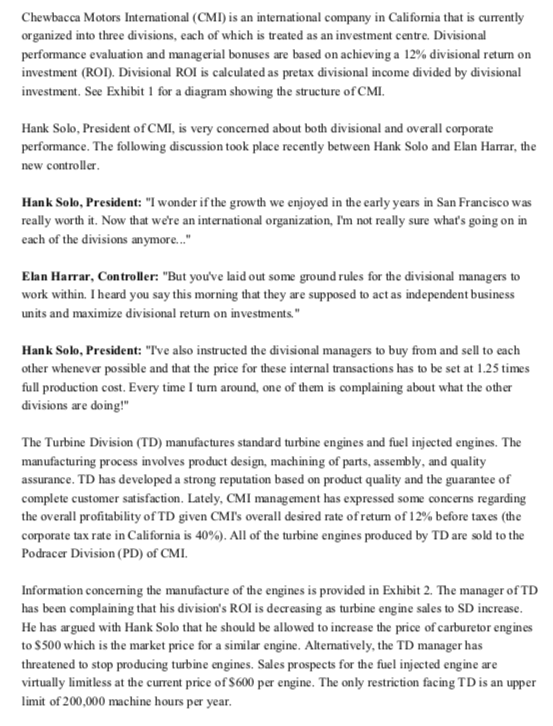

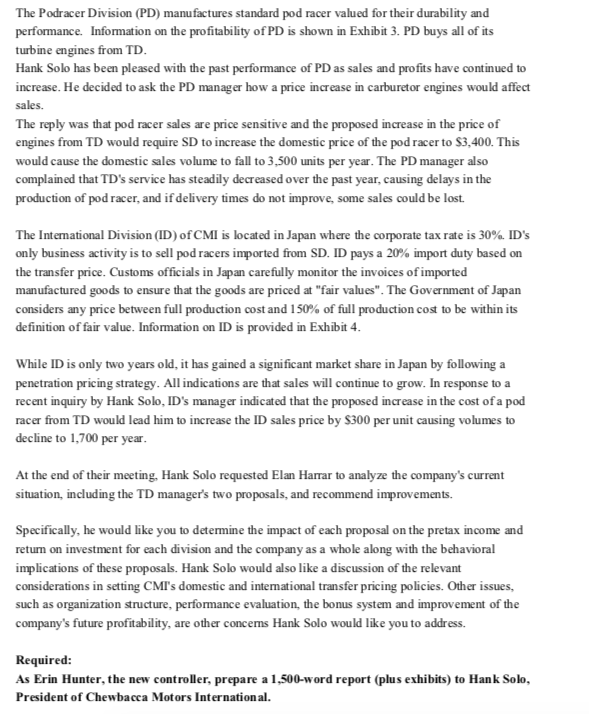

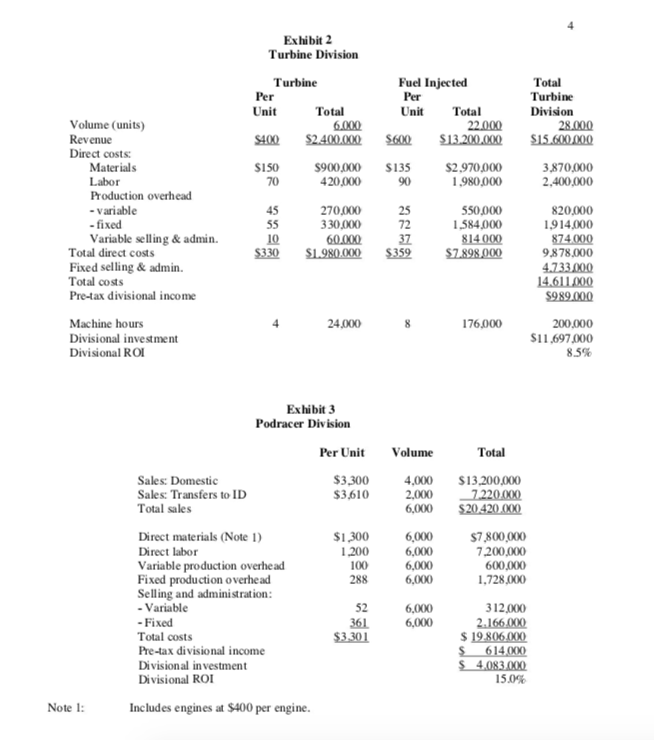

Chewbacca Motors International (CMI) is an international company in California that is currently organized into three divisions, each of which is treated as an investment centre. Divisional performance evaluation and managerial bonuses are based on achieving a 12% divisional retum on investment (ROI). Divisional ROI is calculated as pretax divisional income divided by divisional investment. See Exhibit 1 for a diagram showing the structure of CMI. Hank Solo, President of CMI, is very concemed about both divisional and overall corporate performance. The following discussion took place recently between Hank Solo and Elan Harrar, the new controller Hank Solo, President: "I wonder if the growth we enjoyed in the early years in San Francisco was really worth it. Now that we're an international organization, I'm not really sure what's going on in each of the divisions anymore..." Elan Harrar, Controller: "But you've laid out some ground rules for the divisional managers to work within. I heard you say this morning that they are supposed to act as independent business units and maximize divisional return on investments." Hank Solo, President: "T've also instructed the divisional managers to buy from and sell to each other whenever possible and that the price for these internal transactions has to be set at 1.25 times full production cost. Every time I turn around, one of them is complaining about what the other divisions are doing!" The Turbine Division (TD) manufactures standard turbine engines and fuel injected engines. The manufacturing process involves product design, machining of parts, assembly, and quality assurance. TD has developed a strong reputation based on product quality and the guarantee of complete customer satisfaction. Lately, CMI management has expressed some concerns regarding the overall profitability of TD given CMI's overall desired rate of return of 12% before taxes (the corporate tax rate in California is 40%). All of the turbine engines produced by TD are sold to the Podracer Division (PD) of CMI. Information concerning the manufacture of the engines is provided in Exhibit 2. The manager of TD has been complaining that his division's ROI is decreasing as turbine engine sales to SD increase. He has argued with Hank Solo that he should be allowed to increase the price of carburetor engines to $500 which is the market price for a similar engine. Alternatively, the TD manager has threatened to stop producing turbine engines. Sales prospects for the fuel injected engine are virtually limitless at the current price of $600 per engine. The only restriction facing TD is an upper limit of 200,000 machine hours per year. The Podracer Division (PD) manufactures standard pod racer valued for their durability and performance. Information on the profitability of PD is shown in Exhibit 3. PD buys all of its turbine engines from TD. Hank Solo has been pleased with the past performance of PD as sales and profits have continued to increase. He decided to ask the PD manager how a price increase in carburetor engines would affect sales. The reply was that pod racer sales are price sensitive and the proposed increase in the price of engines from TD would require SD to increase the domestic price of the pod racer to $3,400. This would cause the domestic sales volume to fall to 3,500 units per year. The PD manager also complained that TD's service has steadily decreased over the past year, causing delays in the production of pod racer, and if delivery times do not improve, some sales could be lost. The International Division (ID) of CMI is located in Japan where the corporate tax rate is 30%. ID's only business activity is to sell pod racers imported from SD. ID pays a 20% import duty based on the transfer price. Customs officials in Japan carefully monitor the invoices of imported manufactured goods to ensure that the goods are priced at "fair values". The Government of Japan considers any price between full production cost and 150% of full production cost to be within its definition of fair value. Information on ID is provided in Exhibit 4. While ID is only two years old, it has gained a significant market share in Japan by following a penetration pricing strategy. All indications are that sales will continue to grow. In response to a recent inquiry by Hank Solo, ID's manager indicated that the proposed increase in the cost of a pod racer from TD would lead him to increase the ID sales price by $300 per unit causing volumes to decline to 1,700 per year. At the end of their meeting, Hank Solo requested Elan Harrar to analyze the company's current situation, including the TD manager's two proposals, and recommend improvements. Specifically, he would like you to determine the impact of each proposal on the pretax income and return on investment for each division and the company as a whole along with the behavioral implications of these proposals. Hank Solo would also like a discussion of the relevant considerations in setting CMI's domestic and international transfer pricing policies. Other issues, such as organization structure, performance evaluation, the bonus system and improvement of the company's future profitability, are other concems Hank Solo would like you to address. Required: As Erin Hunter, the new controller, prepare a 1,500-word report (plus exhibits) to Hank Solo, President of Chewbacca Motors International. 3 Exhibit 1 Chewbacca Motors International Wert Chewbacca Motors International (CMI) Turbine engine Pod racers For export Turbine Department (CA) TD Podracer Division (CA) PD International Division (Japan) ID Fuel Injected Engines in California Pod racers In CA Pod racers In Japan Exhibit 2 Turbine Division Turbine Per Unit Total 6,000 $400 $2.400.000 S150 $900,000 70 420,000 Fuel Injected Per Unit Total $600 $13.200.000 $135 $2.970,000 90 1,980,000 22.000 Total Turbine Division 28.000 $15.600.000 3,870,000 2,400,000 Volume (units) Revenue Direct costs Materials Labor Production overhead - Variable - fixed Variable selling & admin. Total direct costs Fixed selling & admin. Total costs Pre-tax divisional income Machine hours Divisional investment Divisional ROI 45 55 10 $330 270,000 330,000 60.000 $1.980.000 25 72 37 $359 550,000 1,584,000 814000 $7.898.000 820,000 1,914,000 874.000 9,878,000 4.733.000 14.611.000 $989.000 200,000 $11.697,000 8.5% 24,000 176,000 Exhibit 3 Podracer Division Per Unit Sales: Domestic $3,300 Sales Transfers to ID $3,610 Total sales Direct materials (Note 1) $1,300 Direct labor 1,200 Variable production overhead 100 Fixed production overhead 288 Selling and administration: - Variable 52 - Fixed 361 Total costs $3.301 Pre-tax divisional income Division al investment Divisional ROI Volume 4,000 2,000 6,000 6,000 6,000 6,000 6,000 6,000 6,000 Total $13,200,000 7.220,000 $20.420.000 $7.800.000 7,200,000 600,000 1,728.000 312,000 2.166.000 $ 19.806.000 614.000 $ 4,083.000 15.0% Note 1: Includes engines at $400 per engine. 5 Exhibit 4 International Division (In US Dollars) Per Unit Total Volume 2.000 Revenue $4,700 $9,400,000 Cost of Pod Racers (Note 1) 4.332 8.664.000 Gross margin 368 736.000 Selling and administration: - Variable 47 94,000 - fixed 86 172,000 133 266.000 Pre-tax divisional income S235 $470.000 Divisional investment $2.379.000 Divisional ROI 19.8% As acquired from the Podracer Division at 125% of full production cost (rounded to the nearest dollar) plus 20% import duty on goods imported into Japan. Note: 1. Chewbacca Motors International (CMI) is an international company in California that is currently organized into three divisions, each of which is treated as an investment centre. Divisional performance evaluation and managerial bonuses are based on achieving a 12% divisional retum on investment (ROI). Divisional ROI is calculated as pretax divisional income divided by divisional investment. See Exhibit 1 for a diagram showing the structure of CMI. Hank Solo, President of CMI, is very concemed about both divisional and overall corporate performance. The following discussion took place recently between Hank Solo and Elan Harrar, the new controller Hank Solo, President: "I wonder if the growth we enjoyed in the early years in San Francisco was really worth it. Now that we're an international organization, I'm not really sure what's going on in each of the divisions anymore..." Elan Harrar, Controller: "But you've laid out some ground rules for the divisional managers to work within. I heard you say this morning that they are supposed to act as independent business units and maximize divisional return on investments." Hank Solo, President: "T've also instructed the divisional managers to buy from and sell to each other whenever possible and that the price for these internal transactions has to be set at 1.25 times full production cost. Every time I turn around, one of them is complaining about what the other divisions are doing!" The Turbine Division (TD) manufactures standard turbine engines and fuel injected engines. The manufacturing process involves product design, machining of parts, assembly, and quality assurance. TD has developed a strong reputation based on product quality and the guarantee of complete customer satisfaction. Lately, CMI management has expressed some concerns regarding the overall profitability of TD given CMI's overall desired rate of return of 12% before taxes (the corporate tax rate in California is 40%). All of the turbine engines produced by TD are sold to the Podracer Division (PD) of CMI. Information concerning the manufacture of the engines is provided in Exhibit 2. The manager of TD has been complaining that his division's ROI is decreasing as turbine engine sales to SD increase. He has argued with Hank Solo that he should be allowed to increase the price of carburetor engines to $500 which is the market price for a similar engine. Alternatively, the TD manager has threatened to stop producing turbine engines. Sales prospects for the fuel injected engine are virtually limitless at the current price of $600 per engine. The only restriction facing TD is an upper limit of 200,000 machine hours per year. The Podracer Division (PD) manufactures standard pod racer valued for their durability and performance. Information on the profitability of PD is shown in Exhibit 3. PD buys all of its turbine engines from TD. Hank Solo has been pleased with the past performance of PD as sales and profits have continued to increase. He decided to ask the PD manager how a price increase in carburetor engines would affect sales. The reply was that pod racer sales are price sensitive and the proposed increase in the price of engines from TD would require SD to increase the domestic price of the pod racer to $3,400. This would cause the domestic sales volume to fall to 3,500 units per year. The PD manager also complained that TD's service has steadily decreased over the past year, causing delays in the production of pod racer, and if delivery times do not improve, some sales could be lost. The International Division (ID) of CMI is located in Japan where the corporate tax rate is 30%. ID's only business activity is to sell pod racers imported from SD. ID pays a 20% import duty based on the transfer price. Customs officials in Japan carefully monitor the invoices of imported manufactured goods to ensure that the goods are priced at "fair values". The Government of Japan considers any price between full production cost and 150% of full production cost to be within its definition of fair value. Information on ID is provided in Exhibit 4. While ID is only two years old, it has gained a significant market share in Japan by following a penetration pricing strategy. All indications are that sales will continue to grow. In response to a recent inquiry by Hank Solo, ID's manager indicated that the proposed increase in the cost of a pod racer from TD would lead him to increase the ID sales price by $300 per unit causing volumes to decline to 1,700 per year. At the end of their meeting, Hank Solo requested Elan Harrar to analyze the company's current situation, including the TD manager's two proposals, and recommend improvements. Specifically, he would like you to determine the impact of each proposal on the pretax income and return on investment for each division and the company as a whole along with the behavioral implications of these proposals. Hank Solo would also like a discussion of the relevant considerations in setting CMI's domestic and international transfer pricing policies. Other issues, such as organization structure, performance evaluation, the bonus system and improvement of the company's future profitability, are other concems Hank Solo would like you to address. Required: As Erin Hunter, the new controller, prepare a 1,500-word report (plus exhibits) to Hank Solo, President of Chewbacca Motors International. 3 Exhibit 1 Chewbacca Motors International Wert Chewbacca Motors International (CMI) Turbine engine Pod racers For export Turbine Department (CA) TD Podracer Division (CA) PD International Division (Japan) ID Fuel Injected Engines in California Pod racers In CA Pod racers In Japan Exhibit 2 Turbine Division Turbine Per Unit Total 6,000 $400 $2.400.000 S150 $900,000 70 420,000 Fuel Injected Per Unit Total $600 $13.200.000 $135 $2.970,000 90 1,980,000 22.000 Total Turbine Division 28.000 $15.600.000 3,870,000 2,400,000 Volume (units) Revenue Direct costs Materials Labor Production overhead - Variable - fixed Variable selling & admin. Total direct costs Fixed selling & admin. Total costs Pre-tax divisional income Machine hours Divisional investment Divisional ROI 45 55 10 $330 270,000 330,000 60.000 $1.980.000 25 72 37 $359 550,000 1,584,000 814000 $7.898.000 820,000 1,914,000 874.000 9,878,000 4.733.000 14.611.000 $989.000 200,000 $11.697,000 8.5% 24,000 176,000 Exhibit 3 Podracer Division Per Unit Sales: Domestic $3,300 Sales Transfers to ID $3,610 Total sales Direct materials (Note 1) $1,300 Direct labor 1,200 Variable production overhead 100 Fixed production overhead 288 Selling and administration: - Variable 52 - Fixed 361 Total costs $3.301 Pre-tax divisional income Division al investment Divisional ROI Volume 4,000 2,000 6,000 6,000 6,000 6,000 6,000 6,000 6,000 Total $13,200,000 7.220,000 $20.420.000 $7.800.000 7,200,000 600,000 1,728.000 312,000 2.166.000 $ 19.806.000 614.000 $ 4,083.000 15.0% Note 1: Includes engines at $400 per engine. 5 Exhibit 4 International Division (In US Dollars) Per Unit Total Volume 2.000 Revenue $4,700 $9,400,000 Cost of Pod Racers (Note 1) 4.332 8.664.000 Gross margin 368 736.000 Selling and administration: - Variable 47 94,000 - fixed 86 172,000 133 266.000 Pre-tax divisional income S235 $470.000 Divisional investment $2.379.000 Divisional ROI 19.8% As acquired from the Podracer Division at 125% of full production cost (rounded to the nearest dollar) plus 20% import duty on goods imported into Japan. Note: 1