Hi can you assist with the advantages ?

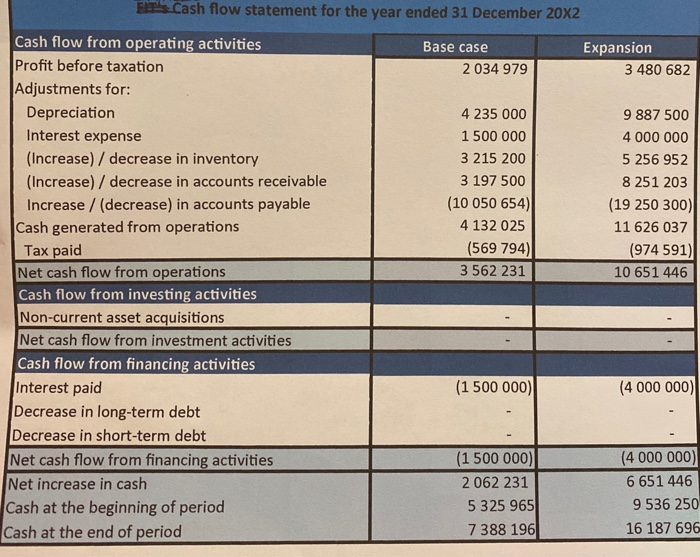

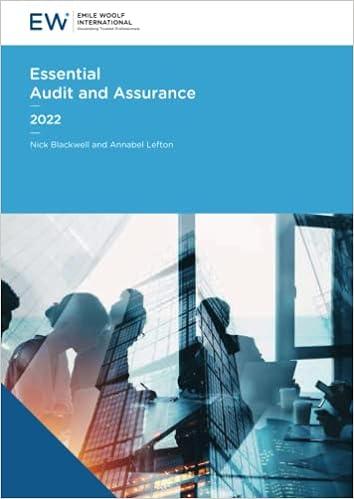

Chineke Technologies, a tech company that produces virtual reality (VR) experiences and products for consumers, is considering whether to expand their operations. Chineke produces three products: 1. Product 1: A VR headset. 2. Product 2: The software to enhance the VR experiences. 3. Product 3: The agility platform, a multidirectional treadmill-like product, which allows simulated movement in the VR space from the comfort of your living room. Chineke have developed forecasts for two scenarios (represented in their financial statements): 1. In scenario one, the "Base case", they do not expand and continue with operations as normal. In scenario two, "Expansion", they expand their operations locally The expansion involves an increase in all operational expenses. However, Chineke is expected to benefit from economies of scale as they ramp up production. Increasing production means that Chineke will have to take on debt in the form of a long-term loan, in order to purchase production line machinery to increase production of Product 3. The loan payments will end in five years. Expanding their operations also means Chineke will have more funds available for research and development initiatives. Based on their supplied projections for the income statement for the next three years, and the cash flow statements for the third year, draft a letter to the Chineke board, describing: Three advantages of each case: base and expansion. Consider the impact on gross margin, operating expenses, net margin, interest expense, tax, overall profit, working capital, and cash flow in each case, and explain how this informed the advantages you have identified Chineke Income statement for 20x0 Base case Expansion Base case 20X1 Expansion Revenue Base case 20x2 Expansion 84 700 000 141 250 000 88 935 000 155 120 000 93 381 750 169 017 856 Revenue from Product A Revenue from Product B Revenue from Product C 44 000 000 23 000 000 17 700 000 64 500 000 33 000 000 43 750 000 46 200 000 24 150 000 18 585 000 71 400 000 35 280 000 48 440 000 48 510 000 25 357 500 19 514 250 78 086 400 37 622 592 53 308 864 Cost of goods sold 65 625 000 107 675 000 68 906 250 116 849 600 72 351 563 125 739 237 COGS Product A COGS Product B COGS Product C 37 400 000 14 950 000 13 275 000 54 180 000 21 120 000 32 375 000 39 270 000 15 697 500 13 938 750 59 262 000 22 226 400 35 361 200 41 233 500 16 482 375 14 635 688 64 030 848 23 326 007 38 382 382 Gross profit Gross profit margin 19 075 000 22,5% 33 575 000 23,8% 20 028 750 22,5% 38 270 400 24,796 21 030 188 22,5% 43 278 619 25,6% 16 855 300 Operating expenses 31 117 375 17 148 362 33 512 276 17 495 209 35 797 937 Salaries and wages Administrative costs Research and development Sales and marketing Depreciation 4 235 000 847 000 4 235 000 3 303 300 4 235 000 6 921 250 1 271 250 7 062 500 S 974 875 9 887 500 4 464 537 800 415 4 002 075 3 646 335 4 235 000 8 066 240 1 240 960 7 756 000 6 561 576 9 887 500 4 669 088 747 054 3 922 034 3 922 034 4 235 000 8 957 946 1 352 143 8 450 893 7 149 455 9 887 500 Operating profit (EBIT) EBIT margin 2 219 700 2,6% 2.457 625 1,796 2 880 388 3,296 4 758 124 3,1% 3 534 979 3,8% 7480 682 4,4% 1 500 000 4 000 000 1 500 000 4 000 000 Interest expense 1 500 000 4 000 000 719 700 (1 542 375) 1 380 388 758 124 Profit/loss before tax 2 034 979 3 480 682 201 516 386 509 212 275 Tax pald 569 794 974 591 518 184 0,6% (1 542 375) -1,1% Profit/loss after tax Net margin 993 879 1.1% 545 849 0,4% 1 465 185 1,6% 2 506 091 1,5% Fris-Cash flow statement for the year ended 31 December 20X2 Base case 2 034 979 Expansion 3 480 682 4 235 000 1 500 000 3 215 200 3 197 500 (10 050 654) 4 132 025 (569 794) 3 562 231 9 887 500 4 000 000 5 256 952 8 251 203 (19 250 300) 11 626 037 (974 591) 10 651 446 Cash flow from operating activities Profit before taxation Adjustments for: Depreciation Interest expense (Increase) / decrease in inventory (Increase) / decrease in accounts receivable Increase / (decrease) in accounts payable Cash generated from operations Tax paid Net cash flow from operations Cash flow from investing activities Non-current asset acquisitions Net cash flow from investment activities Cash flow from financing activities Interest paid Decrease in long-term debt Decrease in short-term debt Net cash flow from financing activities Net increase in cash Cash at the beginning of period Cash at the end of period (1 500 000) (4 000 000) (1 500 000) 2 062 231 5 325 965 7 388 196 (4 000 000) 6 651 446 9 536 250 16 187 696