Question

Hi, I don't understand the response, a) when we write down the optimal allocation function, gamma is supposed to by = 1 with the information

Hi,

I don't understand the response, a) when we write down the optimal allocation function, gamma is supposed to by = 1 with the information provided in the question. Why do we end up using 2 instead, can you explain me please ?

Thanks in advance,

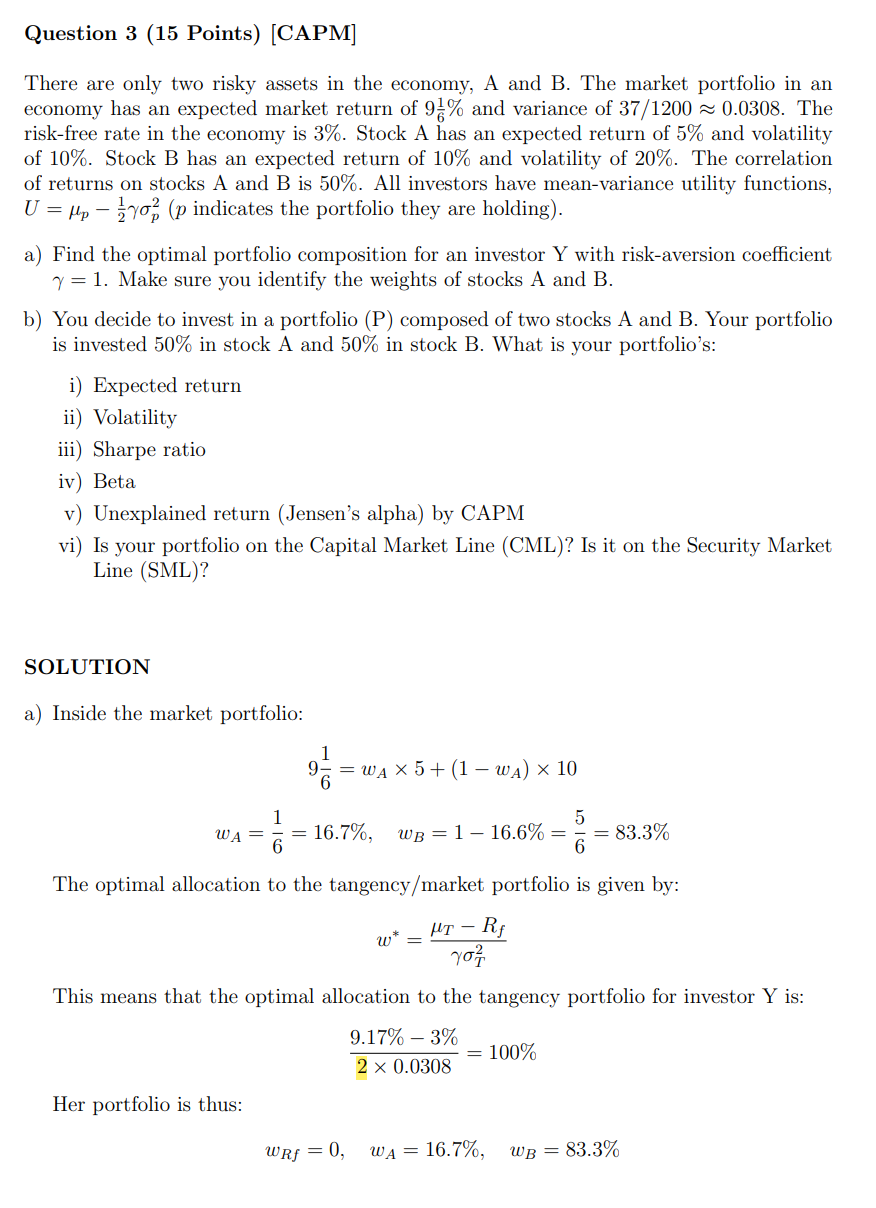

Question 3 (15 Points) [CAPM] There are only two risky assets in the economy, A and B. The market portfolio in an economy has an expected market return of 91% and variance of 37/1200 0.0308. The risk-free rate in the economy is 3%. Stock A has an expected return of 5% and volatility of 10%. Stock B has an expected return of 10% and volatility of 20%. The correlation of returns on stocks A and B is 50%. All investors have mean-variance utility functions, U=Hp (p indicates the portfolio they are holding). - a) Find the optimal portfolio composition for an investor Y with risk-aversion coefficient 1. Make sure you identify the weights of stocks A and B. b) You decide to invest in a portfolio (P) composed of two stocks A and B. Your portfolio is invested 50% in stock A and 50% in stock B. What is your portfolio's: i) Expected return ii) Volatility iii) Sharpe ratio iv) Beta v) Unexplained return (Jensen's alpha) by CAPM vi) Is your portfolio on the Capital Market Line (CML)? Is it on the Security Market Line (SML)? SOLUTION a) Inside the market portfolio: 6 = wA 5+ (1 WA) 10 - 1 5 WA = = 6 16.7%, WB 116.6% = = 83.3% 6 The optimal allocation to the tangency/market portfolio is given by: w* HT- Rf This means that the optimal allocation to the tangency portfolio for investor Y is: 9.17% -3% Her portfolio is thus: = 100% 2 x 0.0308 WRf = 0, WA = 16.7%, WB = 83.3%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance A Contemporary Application of Theory to Policy

Authors: David N Hyman

11th edition

9781305474253, 1285173953, 1305474252, 978-1285173955