Answered step by step

Verified Expert Solution

Question

1 Approved Answer

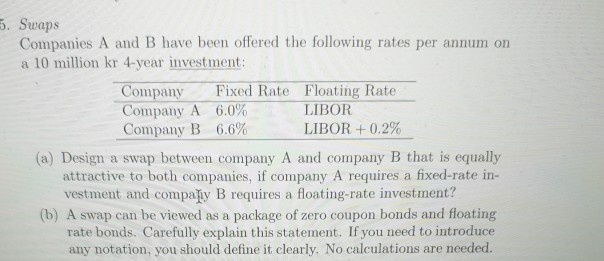

hi pls help 5. Swaps Companies A and B have been offered the following rates per annum on a 10 million kr 4-year investment: Company

hi pls help

5. Swaps Companies A and B have been offered the following rates per annum on a 10 million kr 4-year investment: Company Fixed Rate Floating Rate Company A 6.0% LIBOR Company B 6.6% LIBOR +0.2% (a) Design a swap between company A and company B that is equally attractive to both companies, if company A requires a fixed-rate in- vestment and compally B requires a floating-rate investment? (b) A swap can be viewed as a package of zero coupon bonds and floating rate bonds. Carefully explain this statement. If you need to introduce any notation, you should define it clearly. No calculations are neededStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Institutions Management

Authors: Anthony Saunders

1st Edition

0256110565, 9780256110562