Question

Hi there. I need my assignment checked please by an expert. Correct what is wrong. Please be sure of it. I will post the questions

Hi there. I need my assignment checked please by an expert. Correct what is wrong. Please be sure of it. I will post the questions in the photos. and the answers I'll list them below. I need it by Monday. Thank you!

Answers Below:

Question One: 1.1 B 1.2 C 1.3 C 1.4 A 1.5 D 1.6 D 1.7 B 1.8 B 1.9 A 1.10 C Question Two: 2.1 As provided in the question, J Small decided to purchase and sell goods. Goods purchased = R 54,000 Purchase price (One thirds goods) = R 18,000 Selling Price (One third goods) = 38,000 Profit = R 20,000 Less: Distribution and administrative Expenses (Fixed Expense) = R 3,000 Less: Electricity Expense (Fixed Expense) = R 800 Net Profit for the month of May 2019= R16 200 2.2 Bikes purchased (30,000 each) = R 60,000 Depreciation till 28th Feb 2018 (30% on each i.e., 9000 + 9000) = 18,,000 Value of both bikes as on 1st March 18 (21 000 + 21,000) = R 42,000 When one Bike written off: Written down Value of bike as on 1st March = 21,000 Less: Depreciation till 30th April ( 30% on 21000 for 2 months) = 1050 WDV of Bike as on 30th April = 19,950 Less: Amount Received from Insurance Company = R 9,500 Therefore, Loss (19,950 - 9500) = 10450 2.3 Calculation of Dividend for the shareholders registered on 31 December 2019 Shares registered on 31 Dec, 2019 = 4,00,000 - 1,00,000 = 3,00,000 shares at 100 per share Dividend 50 -cents means Investor with 100 shares would receive = R 50 Therefore, 3,00,000 shares = R 1,50,000 Therefore, Total dividend paid to ordinary shares will be = R 150,000

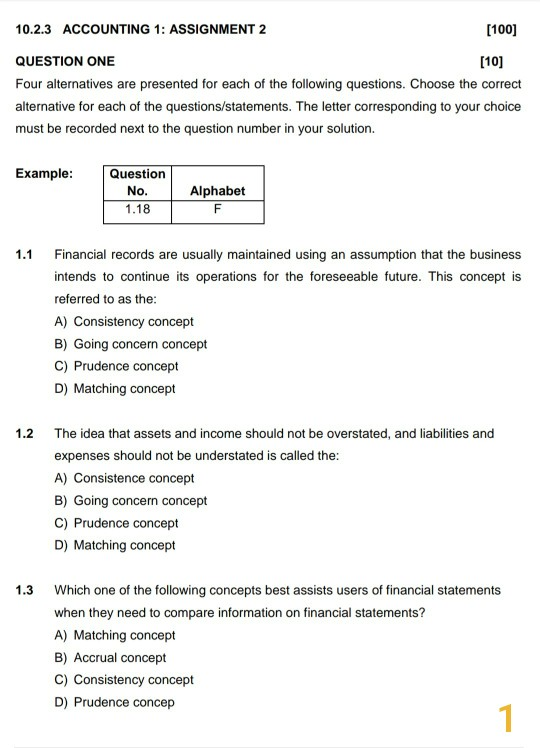

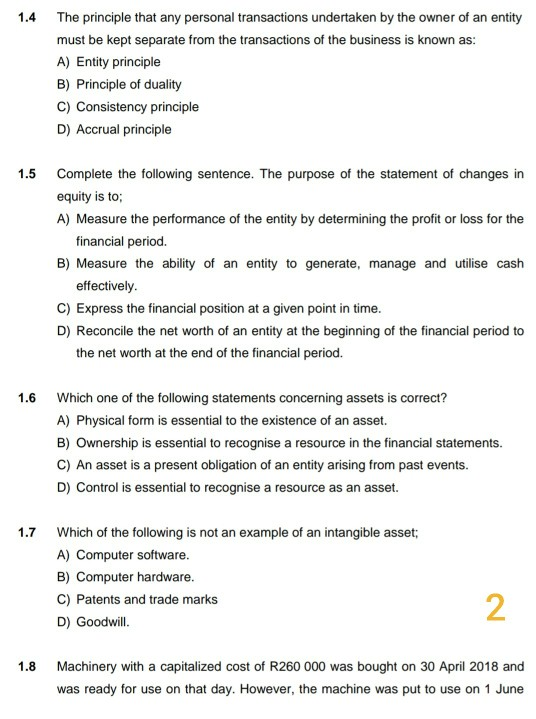

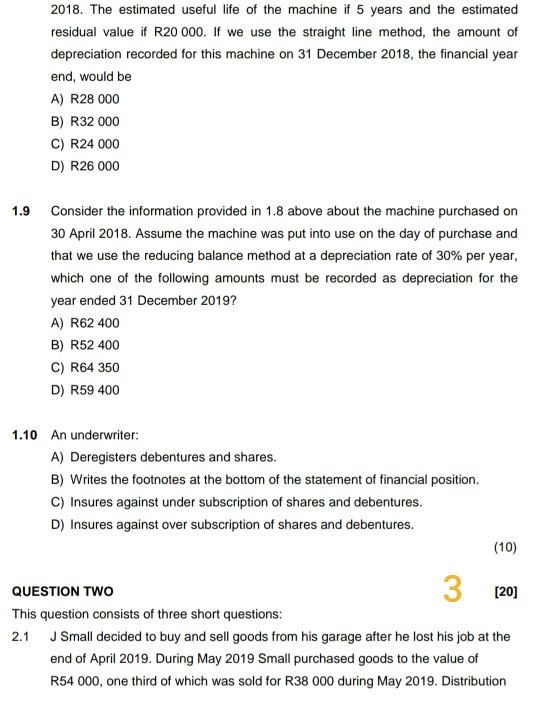

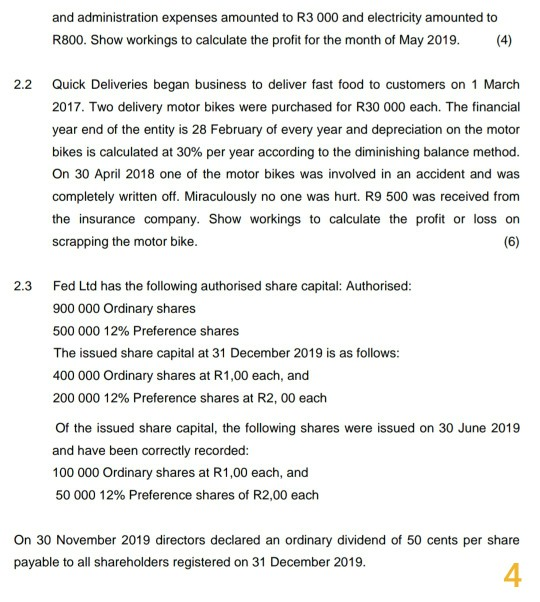

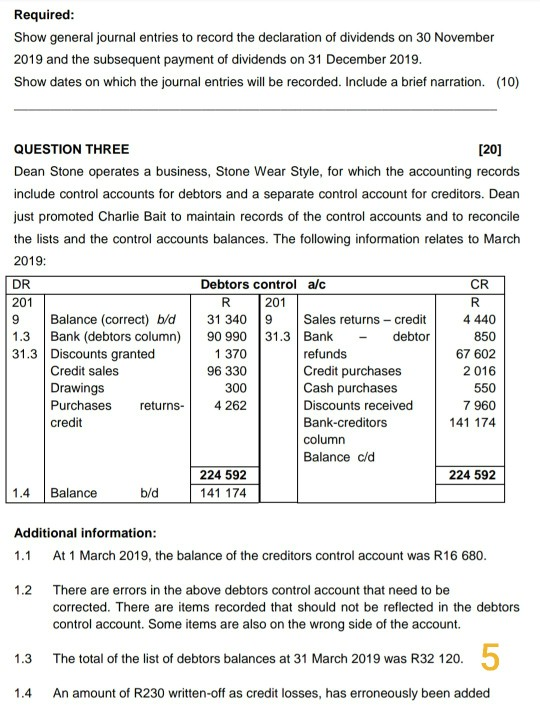

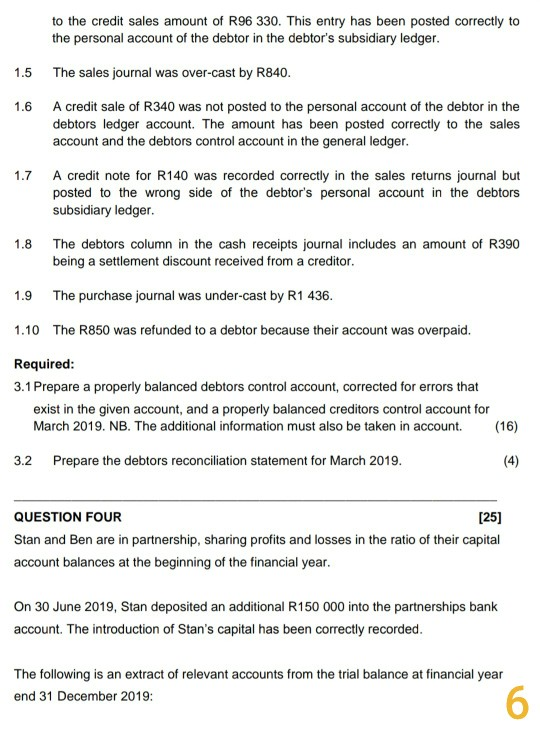

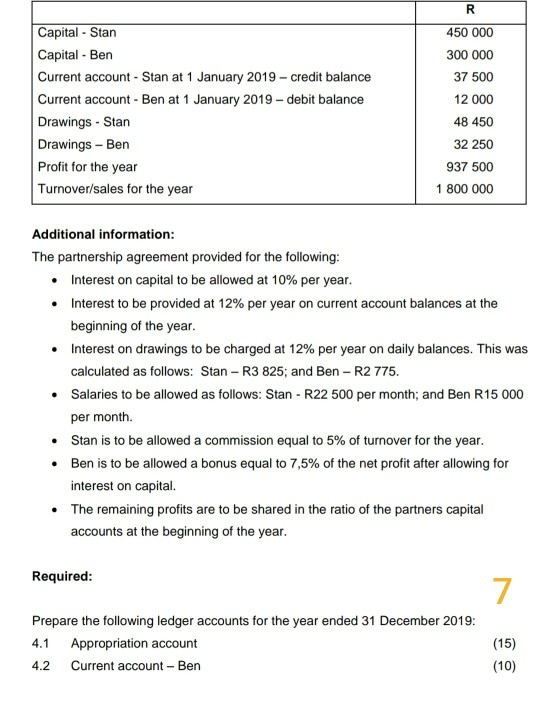

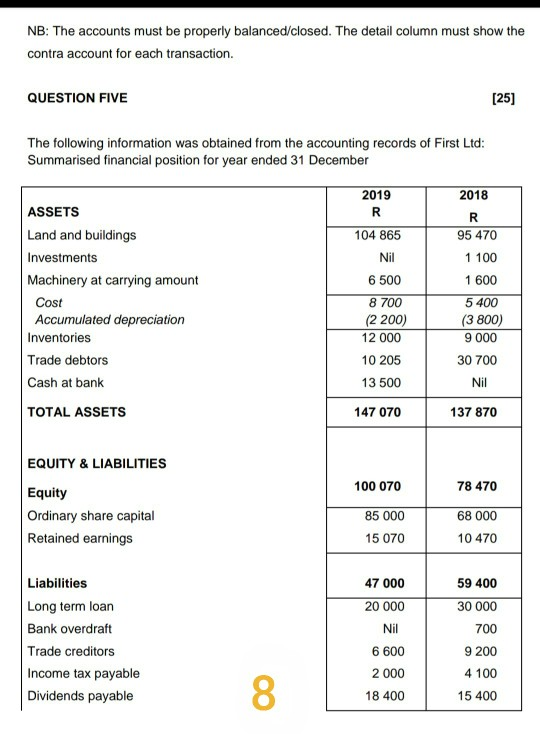

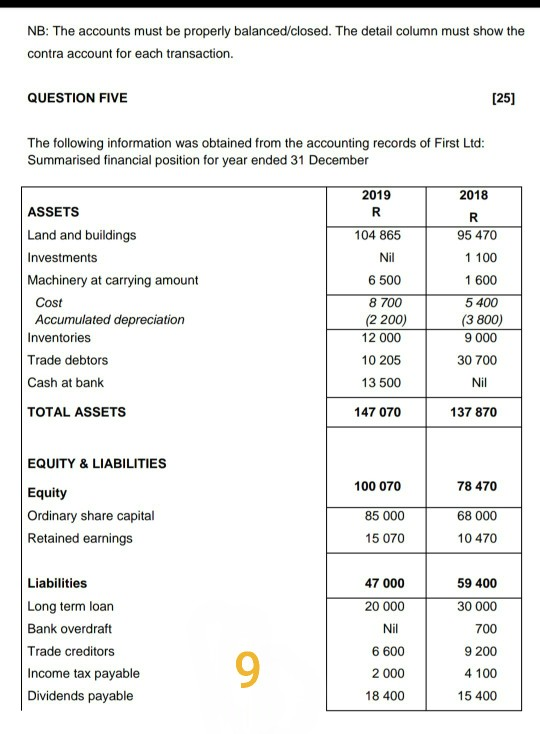

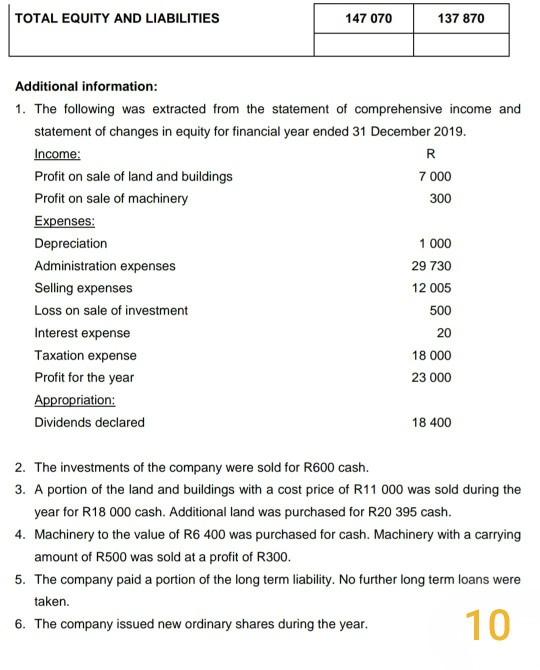

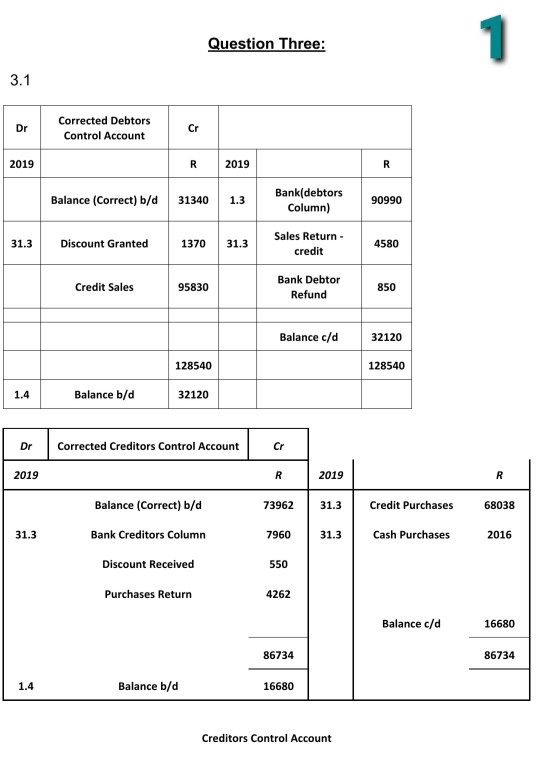

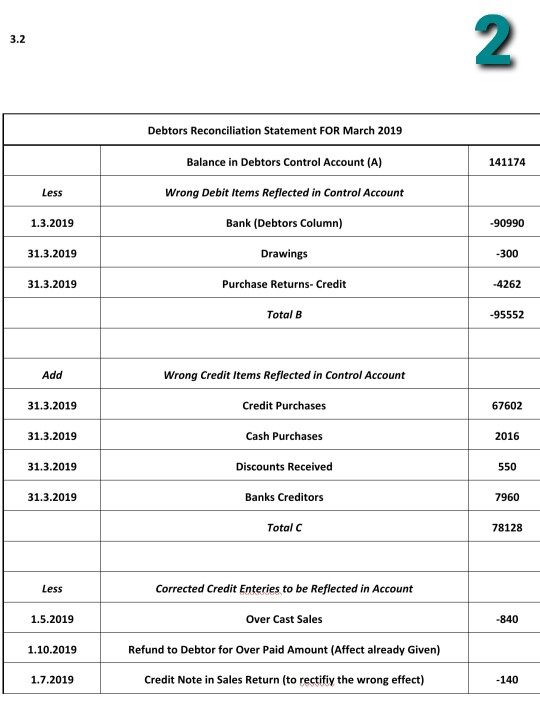

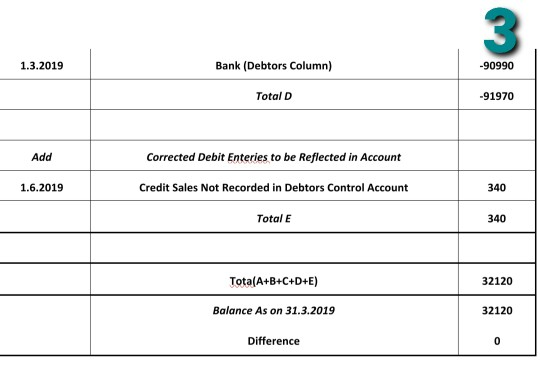

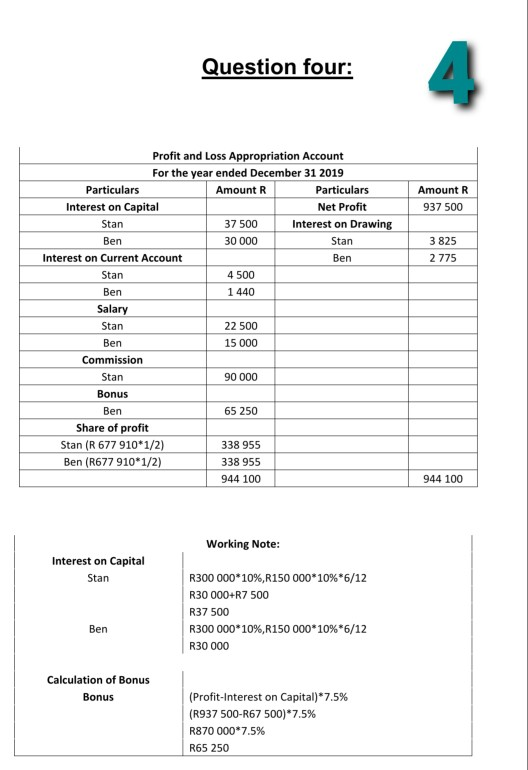

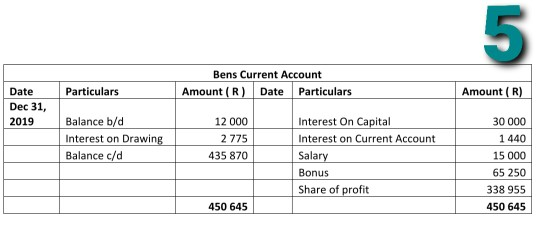

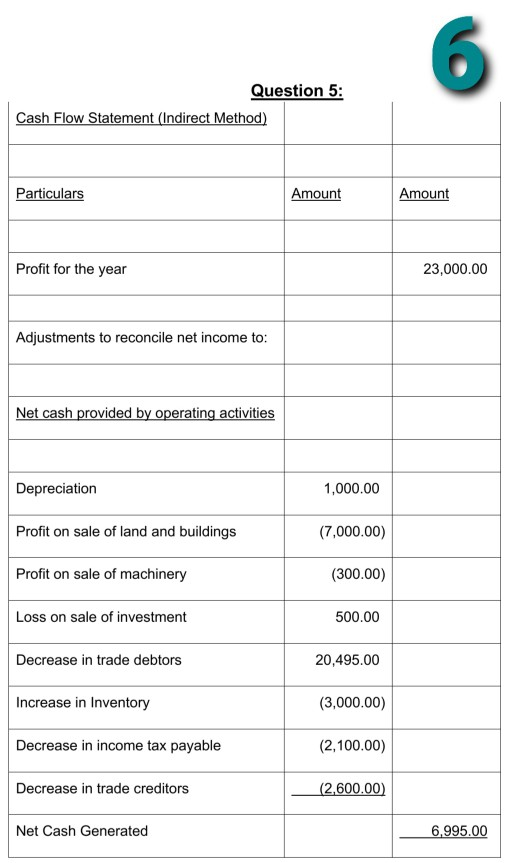

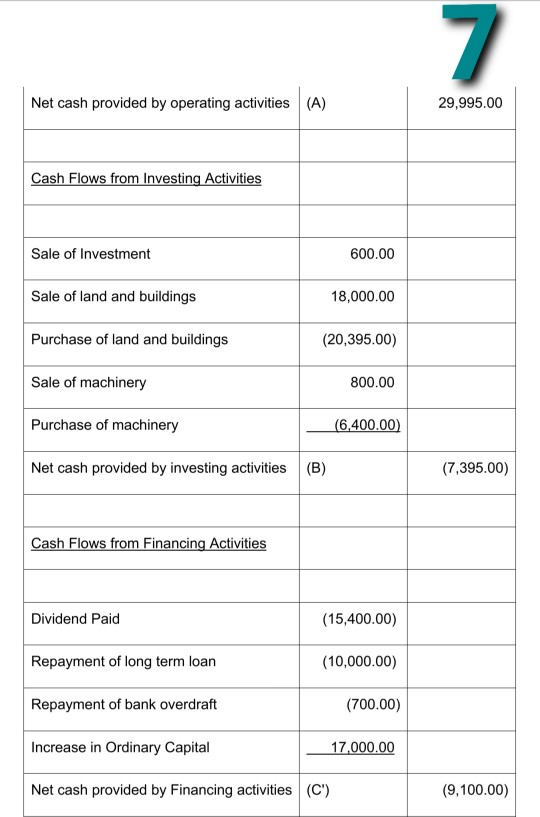

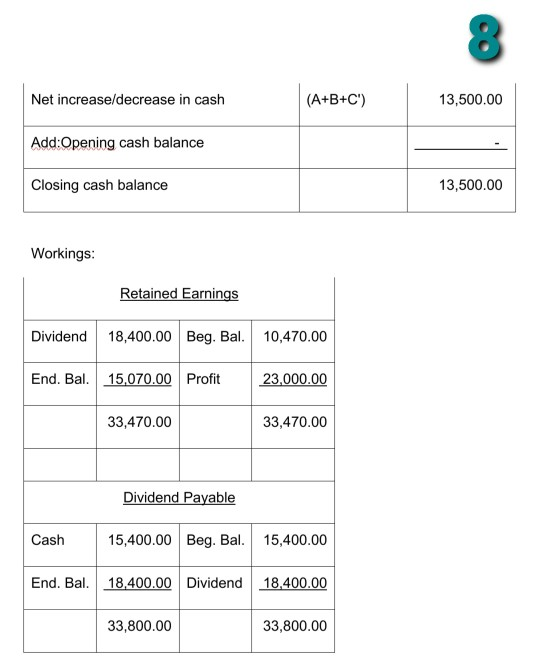

10.2.3 ACCOUNTING 1: ASSIGNMENT 2 [100] QUESTION ONE [10] Four alternatives are presented for each of the following questions. Choose the correct alternative for each of the questions/statements. The letter corresponding to your choice must be recorded next to the question number in your solution. Example: Question No. 1.18 Alphabet F 1.1 Financial records are usually maintained using an assumption that the business intends to continue its operations for the foreseeable future. This concept is referred to as the: A) Consistency concept B) Going concern concept C) Prudence concept D) Matching concept 1.2 The idea that assets and income should not be overstated, and liabilities and expenses should not be understated is called the: A) Consistence concept B) Going concern concept C) Prudence concept D) Matching concept 1.3 Which one of the following concepts best assists users of financial statements when they need to compare information on financial statements? A) Matching concept B) Accrual concept c) Consistency concept D) Prudence concep 1 1.4 The principle that any personal transactions undertaken by the owner of an entity must be kept separate from the transactions of the business is known as: A) Entity principle B) Principle of duality C) Consistency principle D) Accrual principle 1.5 Complete the following sentence. The purpose of the statement of changes in equity is to: A) Measure the performance of the entity by determining the profit or loss for the financial period. B) Measure the ability of an entity to generate, manage and utilise cash effectively. C) Express the financial position at a given point in time. D) Reconcile the net worth of an entity at the beginning of the financial period to the net worth at the end of the financial period. 1.6 Which one of the following statements concerning assets is correct? A) Physical form is essential to the existence of an asset. B) Ownership is essential to recognise a resource in the financial statements. C) An asset is a present obligation of an entity arising from past events. D) Control is essential to recognise a resource as an asset. 1.7 Which of the following is not an example of an intangible asset; A) Computer software. B) Computer hardware. C) Patents and trade marks D) Goodwill. 2. 1.8 Machinery with a capitalized cost of R260 000 was bought on 30 April 2018 and was ready for use on that day. However, the machine was put to use on 1 June 2018. The estimated useful life of the machine if 5 years and the estimated residual value if R20 000. If we use the straight line method, the amount of depreciation recorded for this machine on 31 December 2018, the financial year end, would be A) R28 000 B) R32 000 C) R24 000 D) R26 000 1.9 Consider the information provided in 1.8 above about the machine purchased on 30 April 2018. Assume the machine was put into use on the day of purchase and that we use the reducing balance method at a depreciation rate of 30% per year, which one of the following amounts must be recorded as depreciation for the year ended 31 December 2019? A) R62 400 B) R52 400 C) R64 350 D) R59 400 1.10 An underwriter: A) Deregisters debentures and shares. B) Writes the footnotes at the bottom of the statement of financial position. C) Insures against under subscription of shares and debentures. D) Insures against over subscription of shares and debentures. (10) 3 [20] QUESTION TWO This question consists of three short questions: 2.1 J Small decided to buy and sell goods from his garage after he lost his job at the end of April 2019. During May 2019 Small purchased goods to the value of R54 000, one third of which was sold for R38 000 during May 2019. Distribution and administration expenses amounted to R3 000 and electricity amounted to R800. Show workings to calculate the profit for the month of May 2019. (4) 2.2 Quick Deliveries began business to deliver fast food to customers on 1 March 2017. Two delivery motor bikes were purchased for R30 000 each. The financial year end of the entity is 28 February of every year and depreciation on the motor bikes is calculated at 30% per year according to the diminishing balance method. On 30 April 2018 one of the motor bikes was involved in an accident and was completely written off. Miraculously no one was hurt. R9 500 was received from the insurance company. Show workings to calculate the profit or loss on scrapping the motor bike. (6) 2.3 Fed Ltd has the following authorised share capital: Authorised: 900 000 Ordinary shares 500 000 12% Preference shares The issued share capital at 31 December 2019 is as follows: 400 000 Ordinary shares at R1,00 each, and 200 000 12% Preference shares at R2,00 each of the issued share capital, the following shares were issued on 30 June 2019 and have been correctly recorded: 100 000 Ordinary shares at R1,00 each, and 50 000 12% Preference shares of R2,00 each On 30 November 2019 directors declared an ordinary dividend of 50 cents per share payable to all shareholders registered on 31 December 2019. 4 Required: Show general journal entries to record the declaration of dividends on 30 November 2019 and the subsequent payment of dividends on 31 December 2019. Show dates on which the journal entries will be recorded. Include a brief narration. (10) QUESTION THREE [20] Dean Stone operates a business, Stone Wear Style, for which the accounting records include control accounts for debtors and a separate control account for creditors. Dean just promoted Charlie Bait to maintain records of the control accounts and to reconcile the lists and the control accounts balances. The following information relates to March 2019: DR Debtors control alc CR 201 R 201 R 9 Balance (correct) b/d 31 340 9 Sales returns - Credit 4 440 1.3 Bank (debtors column) 90 990 31.3 Bank debtor 850 31.3 Discounts granted 1 370 refunds 67 602 Credit sales 96 330 Credit purchases 2016 Drawings 300 Cash purchases 550 Purchases returns 4 262 Discounts received 7 960 credit Bank-creditors 141 174 column Balance c/d 224 592 224 592 1.4 Balance b/d 141 174 Additional information: At 1 March 2019, the balance of the creditors control account was R16 680. 1.1 1.2 There are errors in the above debtors control account that need to be corrected. There are items recorded that should not be reflected in the debtors control account. Some items are also on the wrong side of the account. The total of the list of debtors balances at 31 March 2019 was R32 120. 5 1.3 1.4 An amount of R230 written-off as credit losses, has erroneously been added to the credit sales amount of R96 330. This entry has been posted correctly to the personal account of the debtor in the debtor's subsidiary ledger. 1.5 The sales journal was over-cast by R840. 1.6 A credit sale of R340 was not posted to the personal account of the debtor in the debtors ledger account. The amount has been posted correctly to the sales account and the debtors control account in the general ledger. 1.7 A credit note for R140 was recorded correctly in the sales returns journal but posted to the wrong side of the debtor's personal account in the debtors subsidiary ledger 1.8 The debtors column in the cash receipts journal includes an amount of R390 being a settlement discount received from a creditor. The purchase journal was under-cast by R1 436. 1.9 1.10 The R850 was refunded to a debtor because their account was overpaid. Required: 3.1 Prepare a properly balanced debtors control account, corrected for errors that exist in the given account, and a properly balanced creditors control account for March 2019. NB. The additional information must also be taken in account. (16) 3.2 Prepare the debtors reconciliation statement for March 2019. (4) QUESTION FOUR [25] Stan and Ben are in partnership, sharing profits and losses in the ratio of their capital account balances at the beginning of the financial year. On 30 June 2019, Stan deposited an additional R150 000 into the partnerships bank account. The introduction of Stan's capital has been correctly recorded. The following is an extract of relevant accounts from the trial balance at financial year end 31 December 2019: 6 R Capital - Stan Capital - Ben Current account - Stan at 1 January 2019-credit balance Current account - Ben at 1 January 2019 - debit balance Drawings - Stan Drawings - Ben Profit for the year Turnover/sales for the year 450 000 300 000 37 500 12 000 48 450 32 250 937 500 1 800 000 Additional information: The partnership agreement provided for the following: Interest on capital to be allowed at 10% per year. Interest to be provided at 12% per year on current account balances at the beginning of the year. Interest on drawings to be charged at 12% per year on daily balances. This was calculated as follows: Stan - R3 825; and Ben - R2 775. Salaries to be allowed as follows: Stan - R22 500 per month; and Ben R15 000 per month Stan is to be allowed a commission equal to 5% of turnover for the year. Ben is to be allowed a bonus equal to 7,5% of the net profit after allowing for interest on capital The remaining profits are to be shared in the ratio of the partners capital accounts at the beginning of the year. Required: 7 Prepare the following ledger accounts for the year ended 31 December 2019: 4.1 Appropriation account 4.2 Current account - Ben (15) (10) NB: The accounts must be properly balanced/closed. The detail column must show the contra account for each transaction. QUESTION FIVE [25] The following information was obtained from the accounting records of First Ltd: Summarised financial position for year ended 31 December 2018 ASSETS Land and buildings Investments Machinery at carrying amount Cost Accumulated depreciation Inventories Trade debtors Cash at bank TOTAL ASSETS 2019 R 104 865 Nil 6 500 8 700 (2 200) 12 000 10 205 13 500 R 95 470 1 100 1 600 5 400 (3 800) 9 000 30 700 Nil 147 070 137 870 100 070 78 470 EQUITY & LIABILITIES Equity Ordinary share capital Retained earnings 85 000 15 070 68 000 10 470 59 400 30 000 700 Liabilities Long term loan Bank overdraft Trade creditors Income tax payable Dividends payable 47 000 20 000 Nil 6 600 2 000 18 400 9 200 4 100 8. 15 400 NB: The accounts must be properly balanced/closed. The detail column must show the contra account for each transaction. QUESTION FIVE [25] The following information was obtained from the accounting records of First Ltd: Summarised financial position for year ended 31 December 2018 2019 R 104 865 R 95 470 Nil 1 100 ASSETS Land and buildings Investments Machinery at carrying amount Cost Accumulated depreciation Inventories Trade debtors Cash at bank TOTAL ASSETS 6 500 8 700 (2 200) 12 000 10 205 13 500 1 600 5 400 (3 800) 9 000 30 700 Nil 147 070 137 870 100 070 78 470 EQUITY & LIABILITIES Equity Ordinary share capital Retained earnings 85 000 15070 68 000 10 470 Liabilities Long term loan Bank overdraft Trade creditors Income tax payable Dividends payable 47 000 20 000 Nil 6 600 2 000 18 400 59 400 30 000 700 9 200 9 4 100 15 400 TOTAL EQUITY AND LIABILITIES 147 070 137 870 Additional information: 1. The following was extracted from the statement of comprehensive income and statement of changes in equity for financial year ended 31 December 2019. Income: R Profit on sale of land and buildings 7 000 Profit on sale of machinery 300 Expenses: Depreciation 1 000 Administration expenses 29 730 Selling expenses 12 005 Loss on sale of investment 500 Interest expense 20 Taxation expense 18 000 Profit for the year 23 000 Appropriation: Dividends declared 18 400 2. The investments of the company were sold for R600 cash. 3. A portion of the land and buildings with a cost price of R11 000 was sold during the year for R18 000 cash. Additional land was purchased for R20 395 cash. 4. Machinery to the value of R6 400 was purchased for cash. Machinery with a carrying amount of R500 was sold at a profit of R300. 5. The company paid a portion of the long term liability. No further long term loans were taken. 6. The company issued new ordinary shares during the year. 10 Required: Draft the statement of cash flows for the year ended 31 December 2019 method in compliance with international financial reporting standards in as much as the given information allows. The indirect method is in use. Show all workings. (25) END OF ACCOUNTING 1: ASSIGNMENT 2 11 Question Three: 1 3.1 Dr Corrected Debtors Control Account Cr 2019 R 2019 R Balance (Correct) b/d 31340 1.3 Bank(debtors Column) 90990 31.3 Discount Granted 1370 31.3 Sales Return credit 4580 Credit Sales 95830 Bank Debtor Refund 850 Balance c/d 32120 128540 128540 1.4 Balance b/d 32120 Dr Corrected Creditors Control Account Cr 2019 R 2019 R Balance (Correct) b/d 73962 31.3 Credit Purchases 68038 31.3 Bank Creditors Column 7960 31.3 Cash Purchases 2016 Discount Received 550 Purchases Return 4262 Balance c/d 16680 86734 86734 1.4 Balance b/d 16680 Creditors Control Account 3.2 2 Debtors Reconciliation Statement FOR March 2019 Balance in Debtors Control Account (A) 141174 Less Wrong Debit Items Reflected in Control Account 1.3.2019 -90990 Bank (Debtors Column) Drawings 31.3.2019 -300 31.3.2019 Purchase Returns- Credit -4262 Total B -95552 Add Wrong Credit Items Reflected in Control Account 31.3.2019 Credit Purchases 67602 31.3.2019 Cash Purchases 2016 31.3.2019 Discounts Received 550 31.3.2019 Banks Creditors 7960 Total 78128 Less 1.5.2019 Corrected Credit Enteries to be Reflected in Account Over Cast Sales Refund to Debtor for Over Paid Amount (Affect already Given) -840 1.10.2019 1.7.2019 Credit Note in Sales Return (to rectifiy the wrong effect) -140 3 1.3.2019 Bank (Debtors Column) -90990 Total D -91970 Add Corrected Debit Enteries to be reflected in Account Credit Sales Not Recorded in Debtors Control Account 1.6.2019 340 Total E 340 Tota(A+B+C+D+E) 32120 Balance As on 31.3.2019 32120 Difference 0 Question four: 4 Amount R 937 500 3 825 2 775 Profit and Loss Appropriation Account For the year ended December 31 2019 Particulars Amount R Particulars Interest on Capital Net Profit Stan 37 500 Interest on Drawing Ben 30 000 Stan Interest on Current Account Ben Stan 4 500 Ben 1 440 Salary Stan 22 500 Ben 15 000 Commission Stan 90 000 Bonus Ben 65 250 Share of profit Stan (R 677 910*1/2) 338 955 Ben (R677 910*1/2) 338 955 944 100 944 100 Working Note: Interest on Capital Stan R300 000*10%,R150 000*10%*6/12 R30 000+R7 500 R37 500 R300 000*10%,R150 000*10%*6/12 R30 000 Ben Calculation of Bonus Bonus (Profit-Interest on Capital)*7.5% (R937 500-R67 500)*7.5% R870 000*7.5% R65 250 5 Bens Current Account Amount (R) Date Particulars Particulars Amount (R) Date Dec 31, 2019 Balance b/d Interest on Drawing Balance c/d 12 000 2 775 435 870 Interest On Capital Interest on Current Account Salary Bonus Share of profit 30 000 1 440 15 000 65 250 338 955 450 645 450 645 6 Question 5: Cash Flow Statement (Indirect Method) Particulars Amount Amount Profit for the year 23,000.00 Adjustments to reconcile net income to: Net cash provided by operating activities Depreciation 1,000.00 Profit on sale of land and buildings (7,000.00) Profit on sale of machinery (300.00) Loss on sale of investment 500.00 Decrease in trade debtors 20,495.00 Increase in Inventory (3,000.00) Decrease in income tax payable (2,100.00) Decrease in trade creditors (2,600.00) Net Cash Generated 6,995.00 7 Net cash provided by operating activities (A) 29,995.00 Cash Flows from Investing Activities Sale of Investment 600.00 Sale of land and buildings 18,000.00 Purchase of land and buildings (20,395.00) Sale of machinery 800.00 Purchase of machinery (6,400.00) Net cash provided by investing activities (B) (7,395.00) Cash Flows from Financing Activities Dividend Paid (15,400.00) Repayment of long term loan (10,000.00) Repayment of bank overdraft (700.00) Increase in Ordinary Capital 17,000.00 Net cash provided by Financing activities (C") (9,100.00) 8 Net increase/decrease in cash (A+B+C) 13,500.00 Add:Opening cash balance Closing cash balance 13,500.00 Workings: Retained Earnings Dividend 18,400.00 Beg. Bal. 10,470.00 End. Bal. 15.070.00 Profit 23,000.00 33,470.00 33,470.00 Dividend Payable Cash 15,400.00 Beg. Bal. 15,400.00 End. Bal. 18,400.00 Dividend 18,400.00 33,800.00 33,800.00

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Cases An Interactive Learning Approach

Authors: Mark S. Beasley, Frank A. Buckless, Steven M. Glover, Douglas F. Prawitt

4th Edition

0132423502, 978-0132423502