Answered step by step

Verified Expert Solution

Question

1 Approved Answer

hint. The forward rate is 3.95% + 100bps Scenario: You are the CFO of a large financial institution and your firm has agreed that in

hint. The forward rate is 3.95% + 100bps

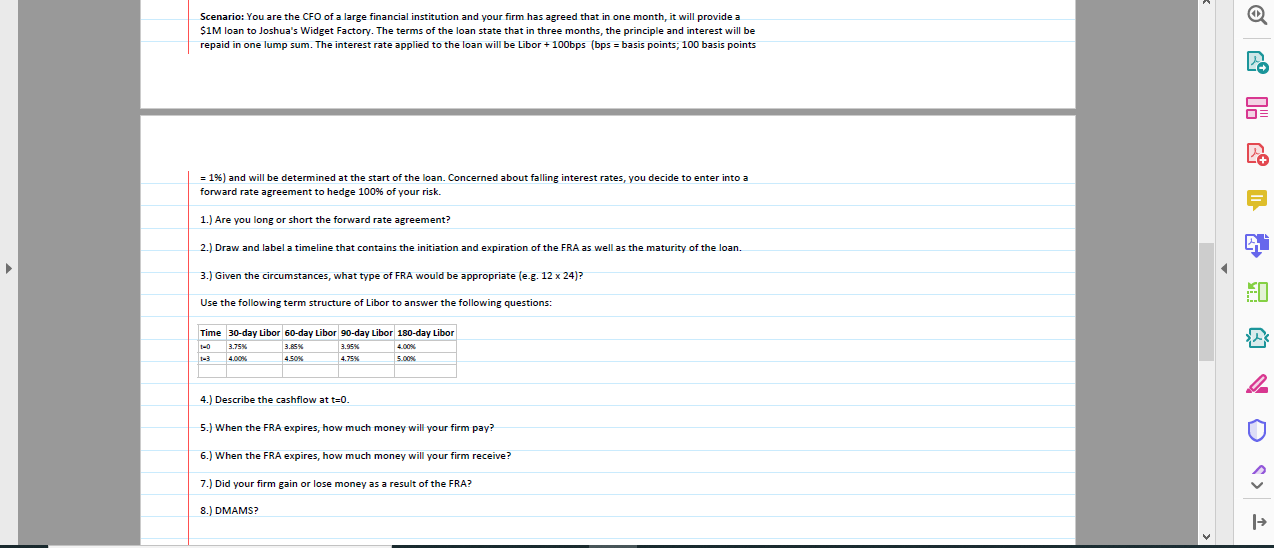

Scenario: You are the CFO of a large financial institution and your firm has agreed that in one month, it will provide a $1M loan to Joshua's Widget Factory. The terms of the loan state that in three months, the principle and interest will be repaid in one lump sum. The interest rate applied to the loan will be Libor + 100bps (bps = basis points; 100 basis points = 1%) and will be determined at the start of the loan. Concerned about falling interest rates, you decide to enter into a forward rate agreement to hedge 100% of your risk. 1.) Are you long or short the forward rate agreement? 2.) Draw and label a timeline that contains the initiation and expiration of the FRA as well as the maturity of the loan. 3.) Given the circumstances, what type of FRA would be appropriate (e.g. 12 x 24)? ED Use the following term structure of Libor to answer the following questions: Time 30-day Libor 60-day Libor 90-day Libor 180-day Libor 1-0 4.00% 450% 4.) Describe the cashflow at t=0. 5.) When the FRA expires, how much money will your firm pay? 6.) When the FRA expires, how much money will your firm receive? 7.) Did your firm gain or lose money as a result of the FRA? 8.) DMAMS? Scenario: You are the CFO of a large financial institution and your firm has agreed that in one month, it will provide a $1M loan to Joshua's Widget Factory. The terms of the loan state that in three months, the principle and interest will be repaid in one lump sum. The interest rate applied to the loan will be Libor + 100bps (bps = basis points; 100 basis points = 1%) and will be determined at the start of the loan. Concerned about falling interest rates, you decide to enter into a forward rate agreement to hedge 100% of your risk. 1.) Are you long or short the forward rate agreement? 2.) Draw and label a timeline that contains the initiation and expiration of the FRA as well as the maturity of the loan. 3.) Given the circumstances, what type of FRA would be appropriate (e.g. 12 x 24)? ED Use the following term structure of Libor to answer the following questions: Time 30-day Libor 60-day Libor 90-day Libor 180-day Libor 1-0 4.00% 450% 4.) Describe the cashflow at t=0. 5.) When the FRA expires, how much money will your firm pay? 6.) When the FRA expires, how much money will your firm receive? 7.) Did your firm gain or lose money as a result of the FRA? 8.) DMAMSStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Asset And Liability Management Volume 2

Authors: S. A. Zenios, W. T. Ziemba

1st Edition

0444528024, 978-0444528025