Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Hints: The following formula are needed for your calculation. E(rP)=wBE(rB)+wSE(rS)P2=(wBB)2+(wSS)2+2(wBB)(wSS)BS B. Based on your calculations, draw a graph (click insert) for the efficient frontier of

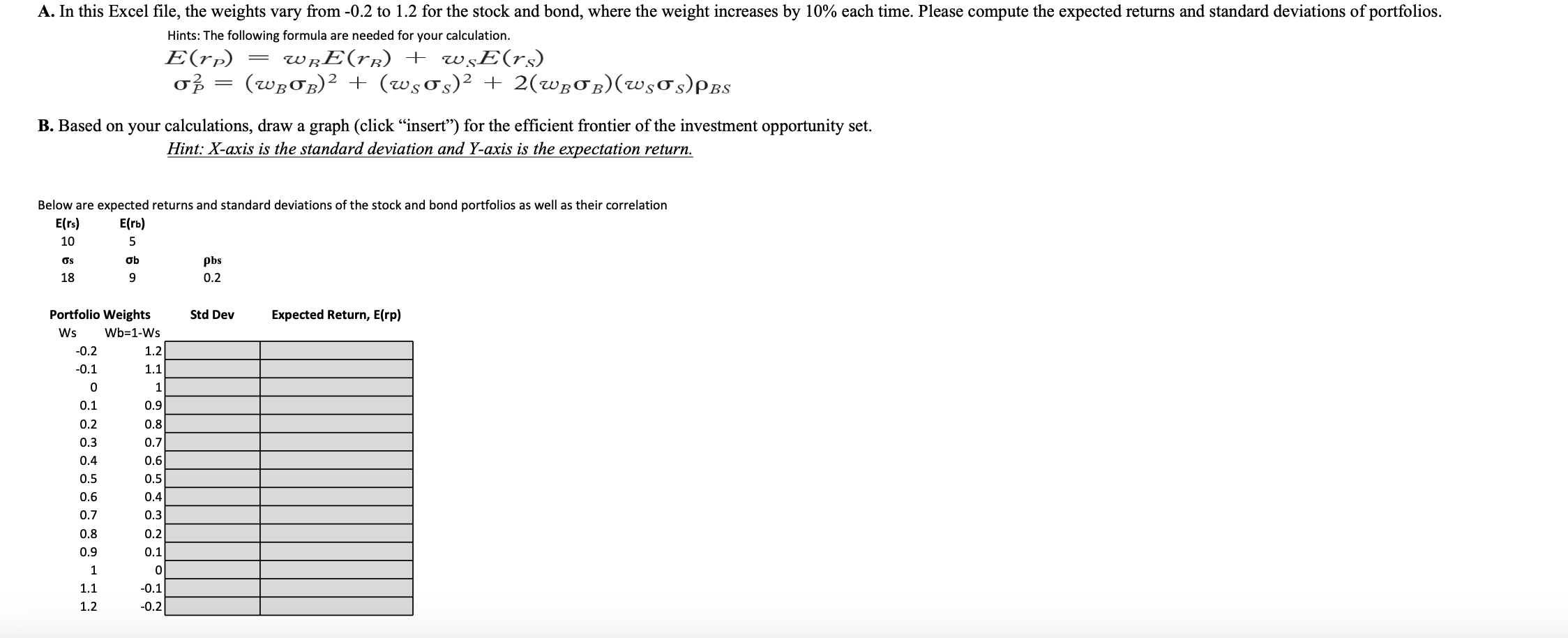

Hints: The following formula are needed for your calculation. E(rP)=wBE(rB)+wSE(rS)P2=(wBB)2+(wSS)2+2(wBB)(wSS)BS B. Based on your calculations, draw a graph (click "insert") for the efficient frontier of the investment opportunity set. Hint: X-axis is the standard deviation and Y-axis is the expectation return. Below are expected returns and standard deviations of the stock and bond portfolios as well as their correlation E(rs)10s18E(rb)5b9bs0.2

Hints: The following formula are needed for your calculation. E(rP)=wBE(rB)+wSE(rS)P2=(wBB)2+(wSS)2+2(wBB)(wSS)BS B. Based on your calculations, draw a graph (click "insert") for the efficient frontier of the investment opportunity set. Hint: X-axis is the standard deviation and Y-axis is the expectation return. Below are expected returns and standard deviations of the stock and bond portfolios as well as their correlation E(rs)10s18E(rb)5b9bs0.2 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Geert Bekaert, Robert Hodrick

3rd edition

1107111820, 110711182X, 978-1107111820