Question

home / study / business / finance / finance questions and answers / gregory is an analyst at a wealth management firm. one of his

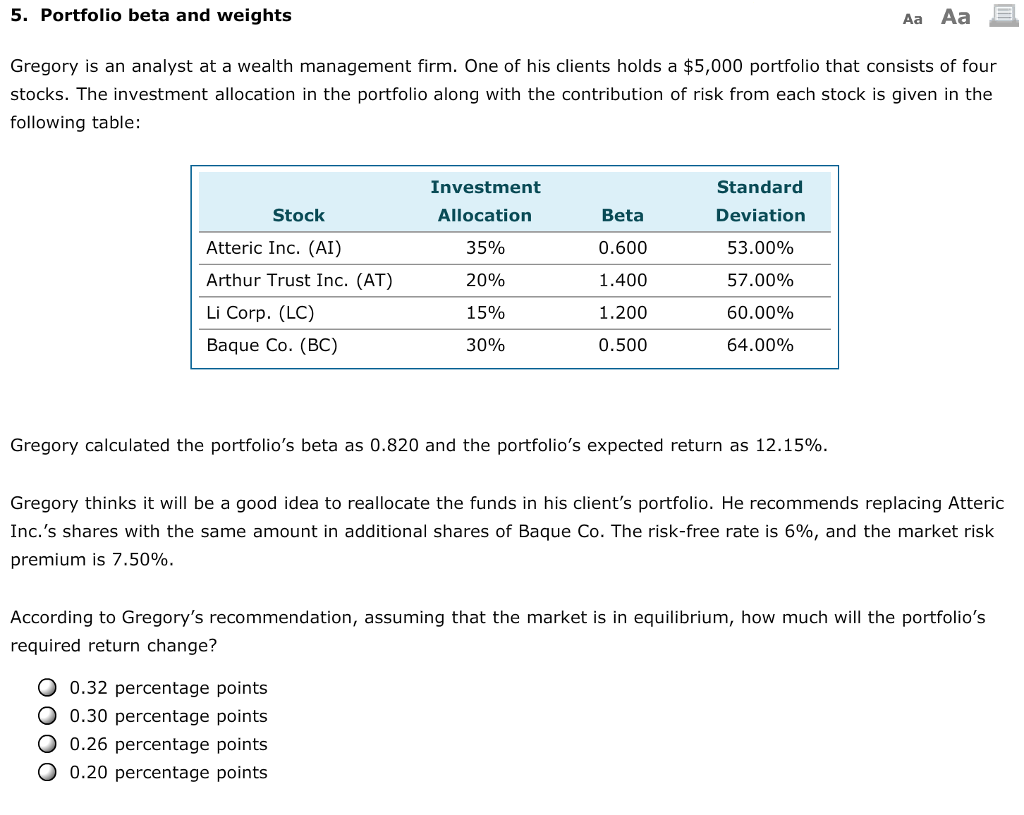

home / study / business / finance / finance questions and answers / gregory is an analyst at a wealth management firm. one of his clients holds a $5,000 portfolio ... Question: Gregory is an analyst at a wealth management firm. One of his clients holds a $5,000 portfolio th... Gregory is an analyst at a wealth management firm. One of his clients holds a $5,000 portfolio that consists of four stocks.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Finance Theories

Authors: Ser-Huang Poon

1st Edition

9814460370, 978-9814460378