Homework #8 -Perfect Competition Part 1: Perfect Competition: Why It Matters Firms are said to be in perfect competition when the following conditions occur: Many

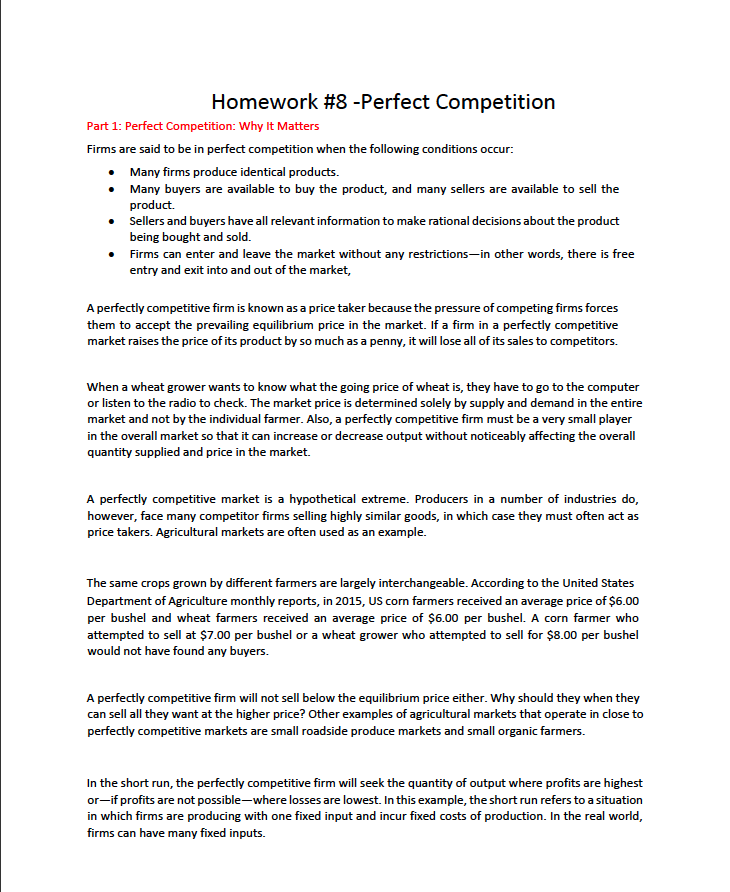

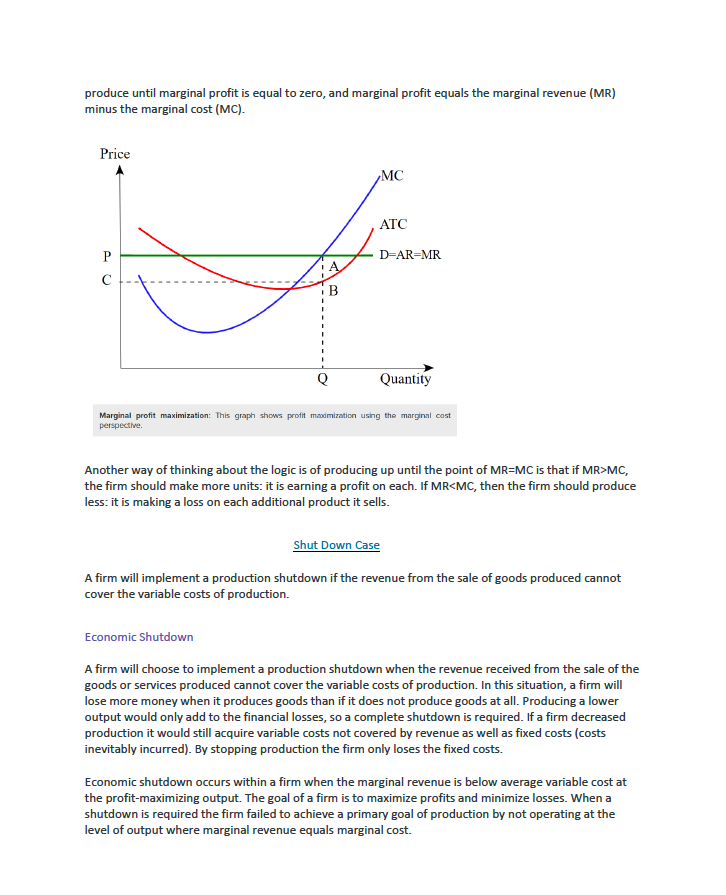

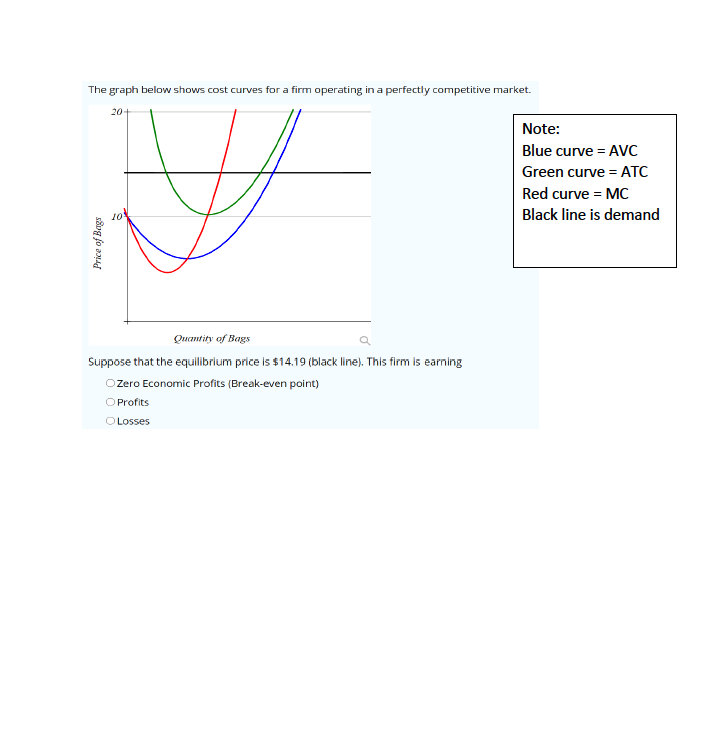

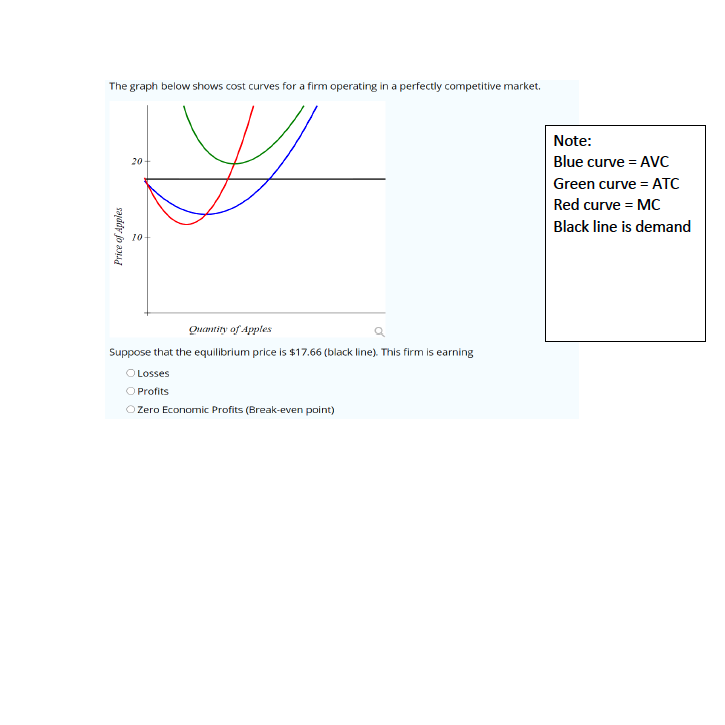

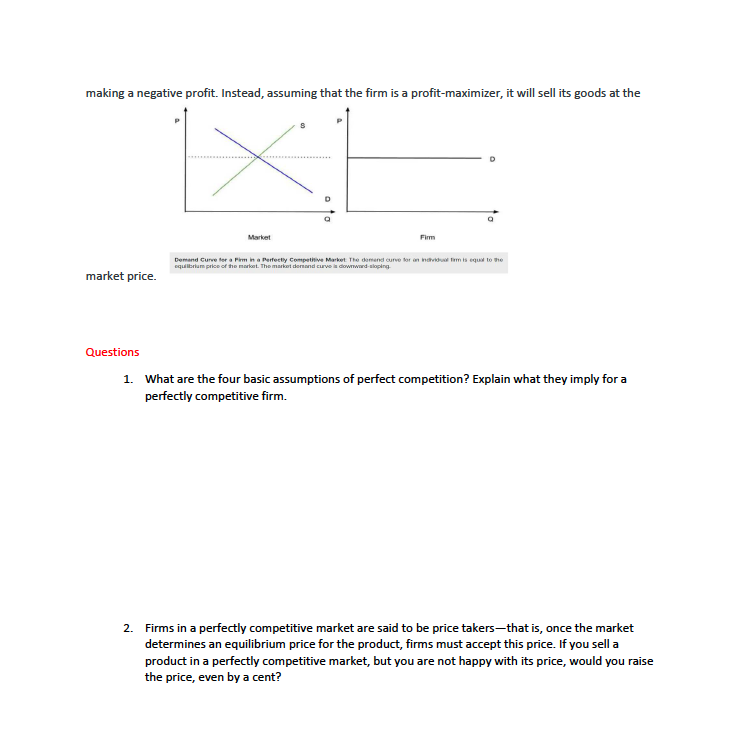

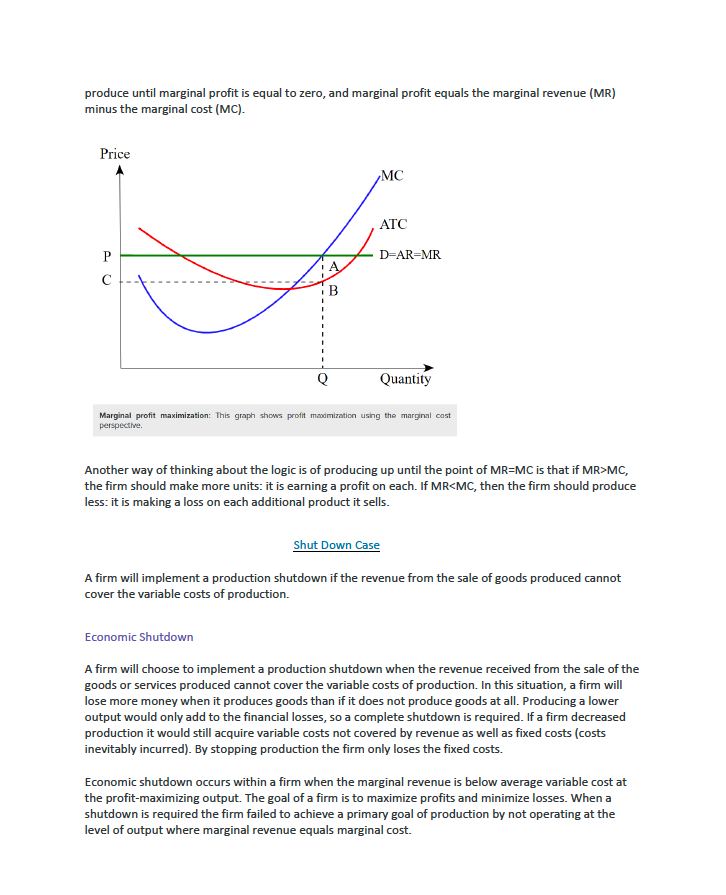

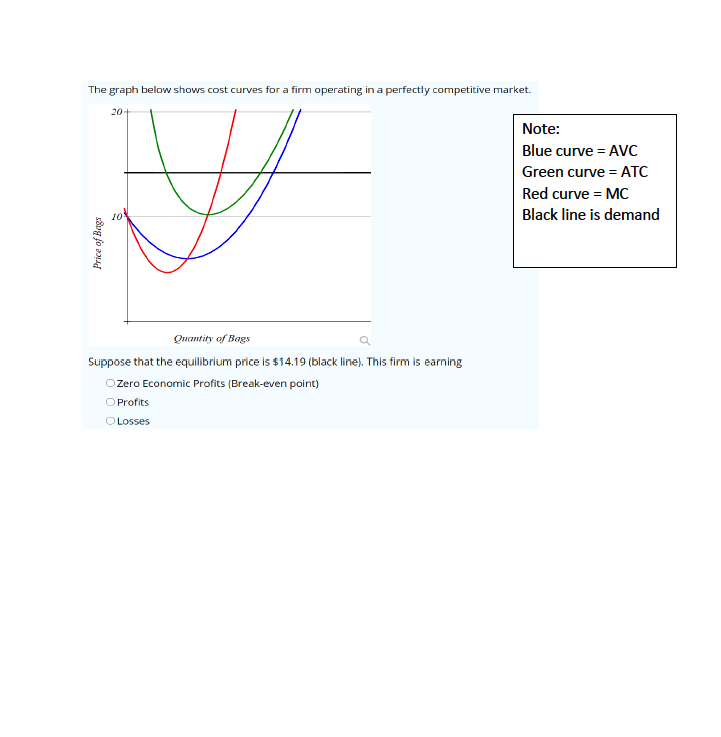

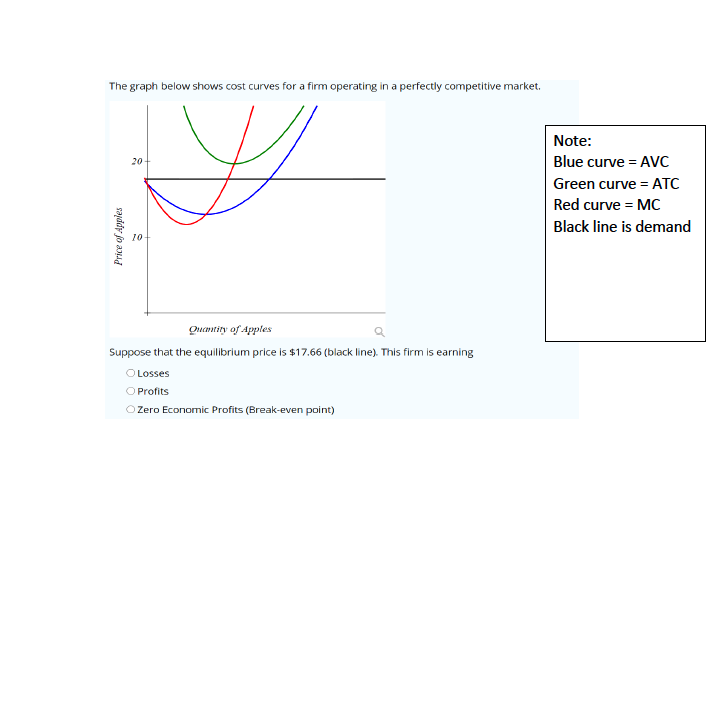

Homework #8 -Perfect Competition Part 1: Perfect Competition: Why It Matters Firms are said to be in perfect competition when the following conditions occur: Many firms produce identical products. Many buyers are available to buy the product, and many sellers are available to sell the product. Sellers and buyers have all relevant information to make rational decisions about the product being bought and sold. Firms can enter and leave the market without any restrictions-in other words, there is free entry and exit into and out of the market, A perfectly competitive firm is known as a price taker because the pressure of competing firms forces them to accept the prevailing equilibrium price in the market. If a firm in a perfectly competitive market raises the price of its product by so much as a penny, it will lose all of its sales to competitors. When a wheat grower wants to know what the going price of wheat is, they have to go to the computer or listen to the radio to check. The market price is determined solely by supply and demand in the entire market and not by the individual farmer. Also, a perfectly competitive firm must be a very small player in the overall market so that it can increase or decrease output without noticeably affecting the overall quantity supplied and price in the market. A perfectly competitive market is a hypothetical extreme. Producers in a number of industries do, however, face many competitor firms selling highly similar goods, in which case they must often act as price takers. Agricultural markets are often used as an example. The same crops grown by different farmers are largely interchangeable. According to the United States Department of Agriculture monthly reports, in 2015, US corn farmers received an average price of $6.00 per bushel and wheat farmers received an average price of $6.00 per bushel. A corn farmer who attempted to sell at $7.00 per bushel or a wheat grower who attempted to sell for $8.00 per bushel would not have found any buyers. A perfectly competitive firm will not sell below the equilibrium price either. Why should they when they can sell all they want at the higher price? Other examples of agricultural markets that operate in close to perfectly competitive markets are small roadside produce markets and small organic farmers. In the short run, the perfectly competitive firm will seek the quantity of output where profits are highest or-if profits are not possible-where losses are lowest. In this example, the short run refers to a situation in which firms are producing with one fixed input and incur fixed costs of production. In the real world, firms can have many fixed inputs.In the long run, perfectly competitive firms will react to profits by increasing production. They will respond to losses by reducing production or exiting the market. Ultimately, a long-run equilibrium will be attained when no new firms want to enter the market and existing firms do not want to leave the market since economic profits have been driven down to zero. Key points " A perfectly competitive firm is a price taker, which means that it must accept the equilibrium price at which it sells goods. If a perfectly competitive firm attempts to charge even a tiny amount more than the market price, it will be unable to make any sales. Perfect competition occurs when there are many sellers, there is easy entry and exiting of firms, products are identical from one seller to another, and sellers are price takers. The market structure is the conditions in an industry, such as number of sellers, how easy or difficult it is for a new firm to enter, and the type of products that are sold. The Demand Curve in Perfect Competition A perfectly competitive firm faces a demand curve is a horizontal line equal to the equilibrium price of the entire market. In a perfectly competitive market the market demand curve is a downward sloping line, reflecting the fact that as the price of an ordinary good increases, the quantity demanded of that good decreases. Price is determined by the intersection of market demand and market supply; individual firms do not have any influence on the market price in perfect competition. Once the market price has been determined by market supply and demand forces, individual firms become price takers. Individual firms are forced to charge the equilibrium price of the market or consumers will purchase the product from the numerous other firms in the market charging a lower price (keep in mind the key conditions of perfect competition). The demand curve for an individual firm is thus equal to the equilibrium price of the market. The demand curve for a firm in a perfectly competitive market varies significantly from that of the entire market. The market demand curve slopes downward, while the perfectly competitive firm's demand curve is a horizontal line equal to the equilibrium price of the entire market. The horizontal demand curve indicates that the elasticity of demand for the good is perfectly elastic. This means that if any individual firm charged a price slightly above market price, it would not sell any products. A strategy often used to increase market share is to offer a firm's product at a lower price than the competitors. In a perfectly competitive market, firms cannot decrease their product price withoutmaking a negative profit. Instead, assuming that the firm is a profit-maximizer, it will sell its goods at the Market Firms Demand Curve for a Firm In a Perfectly Competitvs Market The demand curve for in hatredand form is equal to the equilibrium price of the market. The market demand curve is downward sloping. market price. Questions 1. What are the four basic assumptions of perfect competition? Explain what they imply for a perfectly competitive firm. 2. Firms in a perfectly competitive market are said to be price takers-that is, once the market determines an equilibrium price for the product, firms must accept this price. If you sell a product in a perfectly competitive market, but you are not happy with its price, would you raise the price, even by a cent?3. Would independent trucking fit the characteristics of a perfectly competitive industry? Why? (Independent contractor truck drivers are freelance owner-operators of their own commercial truck. In this role, you can choose which assignments to accept, set your own hours, and negotiate payment and contract conditions. Your specific job duties vary, depending on the company that hires you, the size of your truck, and the type of goods or cargo you choose to carry - think the TV show "Shipping Wars.") 4. A single firm in a perfectly competitive market is relatively small compared to the rest of the market. What does this mean? How small is small? 5. What is a price taker firm? 6. Draw it: How does this look on a demand curve? Please draw the demand curve for a firm in a perfectly competitive market --- NOT THE MARKET DEMAND CURVE.Perfect Competition Continued: Firm Revenues A firm in a competitive market wants to maximize profits just like any other firm. The profit is the difference between a firm's total revenue and its total cost. For a firm operating in a perfectly competitive market, the revenue is calculated as follows: Total Revenue = Price * Quantity AR (Average Revenue) = Total Revenue / Quantity MR (Marginal Revenue) = Change in Total Revenue / Change in Quantity The average revenue (AR) is the amount of revenue a firm receives for each unit of output. The marginal revenue (MR) is the change in total revenue from an additional unit of output sold. For all firms in a competitive market, both AR and MR will be equal to the price. Profit Maximization In order to maximize profits in a perfectly competitive market, firms set marginal revenue equal to marginal cost (MR=MC). MR is the slope of the revenue curve, which is also equal to the demand curve (D) and price (P). In the short-term, it is possible for economic profits to be positive, zero, or negative. When price is greater than average total cost, the firm is making a profit. When price is less than average total cost, the firm is making a loss in the market. Over the long-run, if firms in a perfectly competitive market are earning positive economic profits, more firms will enter the market, which will shift the supply curve to the right. As the supply curve shifts to the right, the equilibrium price will go down. As the price goes down, economic profits will decrease until they become zero. When price is less than average total cost, firms are making a loss. Over the long-run, if firms in a perfectly competitive market are earning negative economic profits, more firms will leave the market, which will shift the supply curve left. As the supply curve shifts left, the price will go up. As the price goes up, economic profits will increase until they become zero. In sum, in the long-run, companies that are engaged in a perfectly competitive market earn zero economic profits. The long-run equilibrium point for a perfectly competitive market occurs where the demand curve (price) intersects the marginal cost (MC) curve and the minimum point of the average cost (AC) curve. Marginal Cost-Marginal Revenue Perspective Profit maximization is the short run or long run process by which a firm determines the price and output level that will result in the largest profit. Firms will produce up until the point that marginal cost equals marginal revenue. This strategy is based on the fact that the total profit reaches its maximum point where marginal revenue equals marginal profit. This is the case because the firm will continue toproduce until marginal profit is equal to zero, and marginal profit equals the marginal revenue (MR) minus the marginal cost (MC). Price MC ATC DEAR=MR A P Q Quantity Marginal profit maximization: This graph shows profit maximization using the marginal cost perspective. Another way of thinking about the logic is of producing up until the point of MR=MC is that if MR>MC, the firm should make more units: it is earning a profit on each. If MRVC) then the firm is covering it's variable costs and there is additional revenue to partially or entirely cover the fixed costs. One the other hand, if the variable cost is greater than the revenue being made (VC>R) then the firm is not even covering production costs and it should be shutdown immediately. Implications of a Shutdown The decision to shutdown production is usually temporary. It does not automatically mean that a firm is going out of business. If the market conditions improve, due to prices increasing or production costs falling, then the firm can resume production. Shutdowns are short run decisions. When a firm shuts down it still retains capital assets, but cannot leave the industry or avoid paying its fixed costs. A firm cannot incur losses indefinitely which impacts long run decisions. When a shutdown last for an extended period of time, a firm has to decide whether to continue to business or leave the industry. The decision to exit is made over a period of time. A firm that exits an industry does not earn any revenue, but is also does not incur fixed or variable costs. Part II: Graphing Perfect Competition 7. A company's profit maximization is equal to the output rule. This is MR = 8. A firm's decision on how much to produce and whether to stay is business is based on profit. (Choose economic or accounting) 9. Profit can be determined in two ways: Profit = Total Revenue - Total Costs ATR (this is price) - ATC = price/quantity Profitable: Price (pick one: >, =, , =, , =, , =, , =, , =,

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance