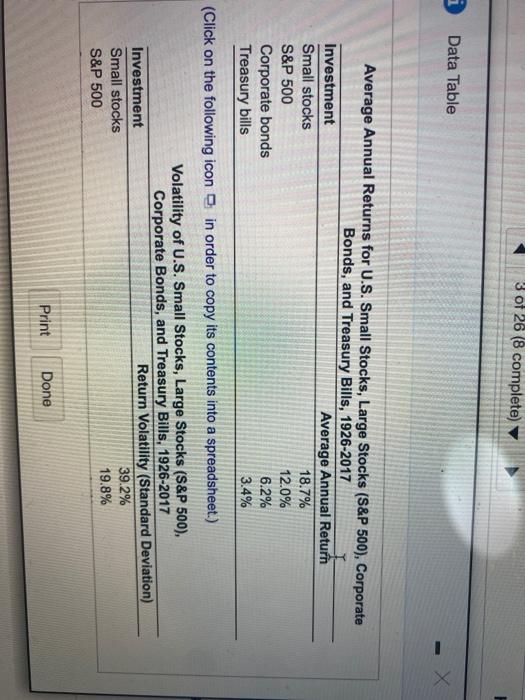

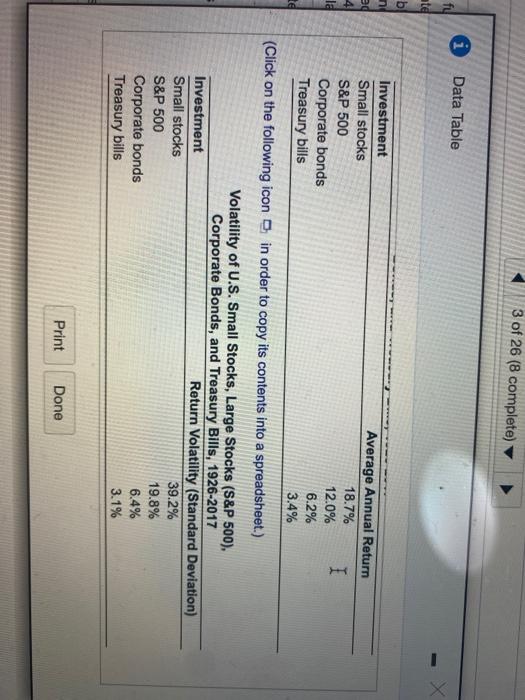

Homework: Module 9: Chapters 10 and 11 - Risk and Return, Po Save Score: 0 of 1 pt 3 of 26 (8 complete) HW Score: 23.0896, 6 of 26 pts P10-8 (similar to) Question Help Assume that historical returns and future returns are independently and identically distributed and drawn from the same distribution a. Calculate the 95% confidence intervals for the expected annual return of four different investments included in the tables the time period spans 92 years) b. Assume that the values in the tables are the true expected return and volatilty estimated without error) and that those retums are normally distributed. For eachinement, the probability that an investor will not lose more than 4% in the next year. (Hint For each investment, you can use the function norminimean, volatility:1) in Excel to compute the probability that a normally distributed variable with a given mean and volatility will exceed x whore x in this case is -4%. Then subtract that probability from 100% to find the probability that an investor will not lose more than 4%) c. Do all the probabilities you caloulated in part (b) make sense? If so, explain. If not, can you identify the reason? a. Calculate the 95% confidence intervals for the expected annual return of four different investments included in the table (the dates are inclusive, so the time period para 12 years) Lower Bound Upper Bound (Round to two decimal places) Confidence interval for small stocks is 3 of 26 (8 complete) Data Table X Average Annual Returns for U.S. Small Stocks, Large Stocks (S&P 500), Corporate Bonds, and Treasury Bills, 1926-2017 Investment Average Annual Return Small stocks 18.7% S&P 500 12.0% Corporate bonds 6.2% Treasury bills 3.4% (Click on the following icon in order to copy its contents into a spreadsheet.) Volatility of U.S. Small Stocks, Large Stocks (S&P 500), Corporate Bonds, and Treasury Bills, 1926-2017 Investment Return Volatility (Standard Deviation) Small stocks 39.2% S&P 500 19.8% Print Done 3 of 26 (8 complete) i Data Table fy ate b nd ad le Investment Average Annual Return Small stocks 18.7% S&P 500 I 12.0% Corporate bonds 6.2% Treasury bills 3.4% (Click on the following icon in order to copy its contents into a spreadsheet.) Volatility of U.S. Small Stocks, Large Stocks (S&P 500). Corporate Bonds, and Treasury Bills, 1926-2017 Investment Return Volatility (Standard Deviation) Small stocks 39.2% S&P 500 19.8% Corporate bonds 6.4% Treasury bills 3.1% Print Done Homework: Module 9: Chapters 10 and 11 - Risk and Return, Po Save Score: 0 of 1 pt 3 of 26 (8 complete) HW Score: 23.0896, 6 of 26 pts P10-8 (similar to) Question Help Assume that historical returns and future returns are independently and identically distributed and drawn from the same distribution a. Calculate the 95% confidence intervals for the expected annual return of four different investments included in the tables the time period spans 92 years) b. Assume that the values in the tables are the true expected return and volatilty estimated without error) and that those retums are normally distributed. For eachinement, the probability that an investor will not lose more than 4% in the next year. (Hint For each investment, you can use the function norminimean, volatility:1) in Excel to compute the probability that a normally distributed variable with a given mean and volatility will exceed x whore x in this case is -4%. Then subtract that probability from 100% to find the probability that an investor will not lose more than 4%) c. Do all the probabilities you caloulated in part (b) make sense? If so, explain. If not, can you identify the reason? a. Calculate the 95% confidence intervals for the expected annual return of four different investments included in the table (the dates are inclusive, so the time period para 12 years) Lower Bound Upper Bound (Round to two decimal places) Confidence interval for small stocks is 3 of 26 (8 complete) Data Table X Average Annual Returns for U.S. Small Stocks, Large Stocks (S&P 500), Corporate Bonds, and Treasury Bills, 1926-2017 Investment Average Annual Return Small stocks 18.7% S&P 500 12.0% Corporate bonds 6.2% Treasury bills 3.4% (Click on the following icon in order to copy its contents into a spreadsheet.) Volatility of U.S. Small Stocks, Large Stocks (S&P 500), Corporate Bonds, and Treasury Bills, 1926-2017 Investment Return Volatility (Standard Deviation) Small stocks 39.2% S&P 500 19.8% Print Done 3 of 26 (8 complete) i Data Table fy ate b nd ad le Investment Average Annual Return Small stocks 18.7% S&P 500 I 12.0% Corporate bonds 6.2% Treasury bills 3.4% (Click on the following icon in order to copy its contents into a spreadsheet.) Volatility of U.S. Small Stocks, Large Stocks (S&P 500). Corporate Bonds, and Treasury Bills, 1926-2017 Investment Return Volatility (Standard Deviation) Small stocks 39.2% S&P 500 19.8% Corporate bonds 6.4% Treasury bills 3.1% Print Done