Answered step by step

Verified Expert Solution

Question

1 Approved Answer

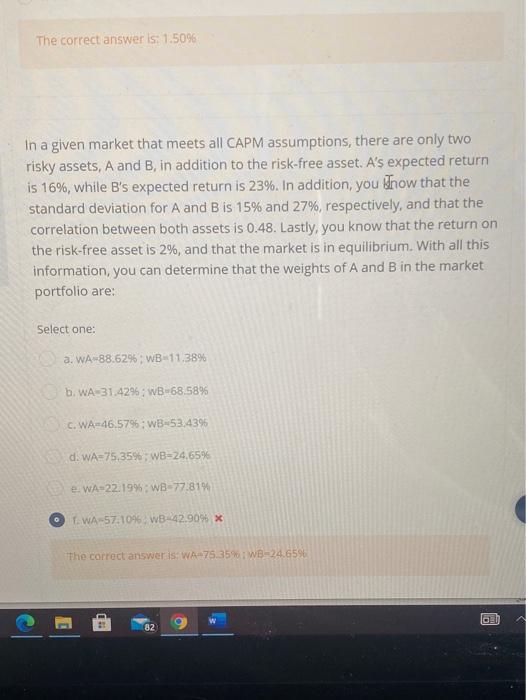

how could I argue that wA=57.1 ; wB=42.9 is the correct answer? The correct answer is: 1.5096 In a given market that meets all CAPM

how could I argue that wA=57.1 ; wB=42.9 is the correct answer?

how could I argue that wA=57.1 ; wB=42.9 is the correct answer?Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investment The Study Of An Economic Aggregate

Authors: Philip J. Lund

1st Edition

0444851380,1483256901