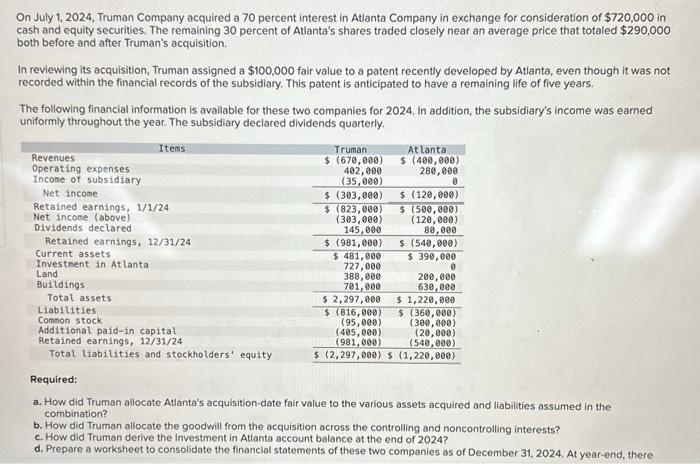

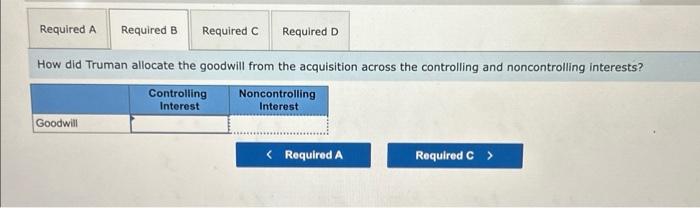

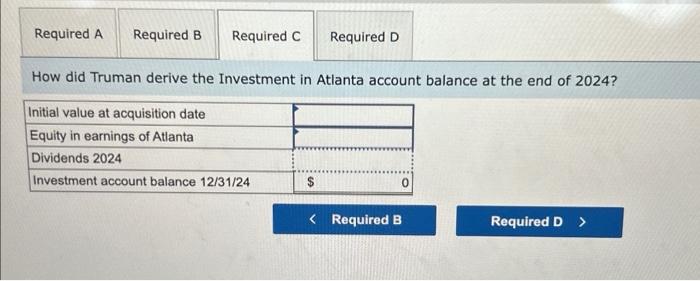

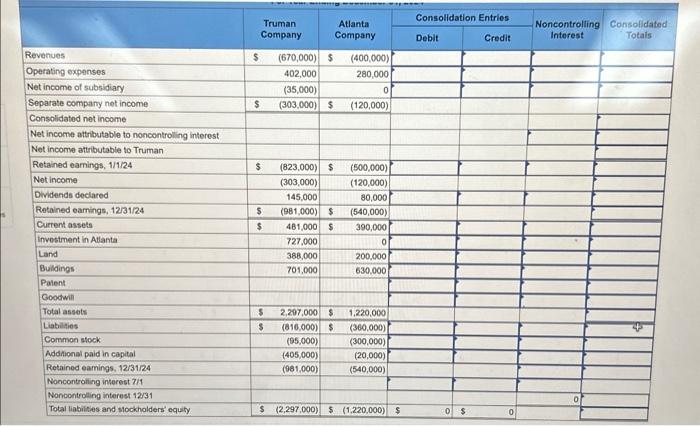

How did Truman derive the Investment in Atlanta account balance at the end of 2024? On July 1, 2024, Truman Company acquired a 70 percent interest in Atlanta Company in exchange for consideration of $720,000 in cash and equity securities. The remaining 30 percent of Atlanta's shares traded closely near an average price that totaled $290,000 both before and after Truman's acquisition. In reviewing its acquisition, Truman assigned a $100,000 fair value to a patent recently developed by Atlanta, even though it was not recorded within the financial records of the subsidiary. This patent is anticipated to have a remaining life of five years. The following financial information is avallable for these two companies for 2024. In addition, the subsidiary's income was earned uniformly throughout the year. The subsidiary declared dividends quarterly. Required: a. How did Truman allocate Atlanta's acquisition-date fair value to the various assets acquired and liabilities assumed in the combination? b. How did Truman allocate the goodwill from the acquisition across the controlling and noncontrolling interests? c. How did Truman derive the investment in Atlanta account balance at the end of 2024 ? d. Prepare a worksheet to consolidate the financial statements of these two companies as of December 31, 2024. At year-end, there \begin{tabular}{|l|l|l|} \hline Required A & Required B & Requi \\ \hline & \\ \hline & \\ \hline & \\ \hline \end{tabular} Requirod A Required B \begin{tabular}{|c|c|c|c|c|c|c|c|c|} \hline \multirow[b]{3}{*}{ Revenues } & \multirow{2}{*}{\multicolumn{2}{|c|}{\begin{tabular}{l} Truman \\ Company \end{tabular}}} & \multirow{2}{*}{\multicolumn{2}{|c|}{\begin{tabular}{l} Atlanta \\ Company \end{tabular}}} & \multicolumn{2}{|c|}{ Consolidation Entries } & \multirow{3}{*}{\begin{tabular}{c} Noncontrolling \\ Interest \end{tabular}} & \multirow{3}{*}{\begin{tabular}{c} Consolidated \\ Totals \end{tabular}} \\ \hline & & & & & \multirow[t]{2}{*}{ Debit } & \multirow[t]{2}{*}{ Credit } & & \\ \hline & $ & (670,000) & $ & (400,000) & & & & \\ \hline Operating expenses & & 402,000 & & 280,000 & & & & \\ \hline Net income of subsidiary & & (35,000) & & 0 & & & & \\ \hline Separate company net income & $ & (303,000) & $ & (120,000) & & & & \\ \hline \multicolumn{9}{|l|}{ Consolidated net income } \\ \hline \multicolumn{9}{|c|}{ Net income attributable to noncontrolling interest } \\ \hline \multicolumn{9}{|l|}{ Net income attributable to Truman } \\ \hline Retained earnings, 1/1/24 & s & (823,000) & $ & (500,000)} & & & & \\ \hline Net income & & (303,000) & & (120,000) & & & & \\ \hline Dividends declared & & 145,000 & & 80,000 & & & & \\ \hline Retained earnings, 12/31/24 & 5 & (981,000) & $ & (540,000) & & & & \\ \hline Current assets & $ & 481,000 & $ & 390,000 & & & & \\ \hline Invostment in Attanta & & 727,000 & & 0 & & & & \\ \hline Land & & 388,000 & & 200,000 & & & & \\ \hline Buldings: & & 701,000 & & 630,000 & & & & \\ \hline \multicolumn{9}{|l|}{ Patent } \\ \hline \multicolumn{9}{|l|}{ Goodwili } \\ \hline Total assets & 5 & 2,207,000 & $ & 1,220,000 & & & & \\ \hline Liabilties & s & (816.000) & $ & (360,000) & & & & 4 \\ \hline Common stock & & (05,000) & & (300,000) & & & & \\ \hline Additional paid in capital & & (405,000) & & (20,000) & & & & \\ \hline Retained earnings, 12/31/24 & & (081,000) & & (540,000) & & = & & \\ \hline \multicolumn{9}{|l|}{ Noncontrolling interest 7/1} \\ \hline Nonocntrolling interest 12/31 & & & & & & & of & \\ \hline Total liabilisies and slockholders equity. & $ & (2,297,000) & 5 & (1,220,000) & 0 & 0 & & \\ \hline \end{tabular} How did Truman allocate the goodwill from the acquisition across the controlling and noncontrolling interests