How do I make a balance sheet & income statement for 12/31/22 at the end of the year using this information. I included a balance sheet from 03/31/22.

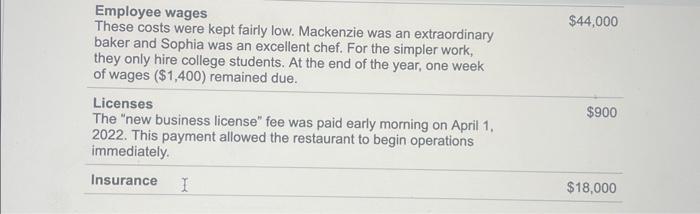

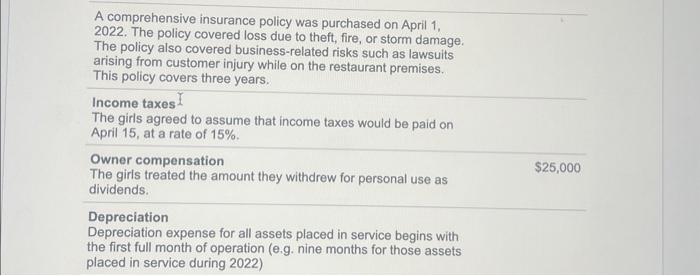

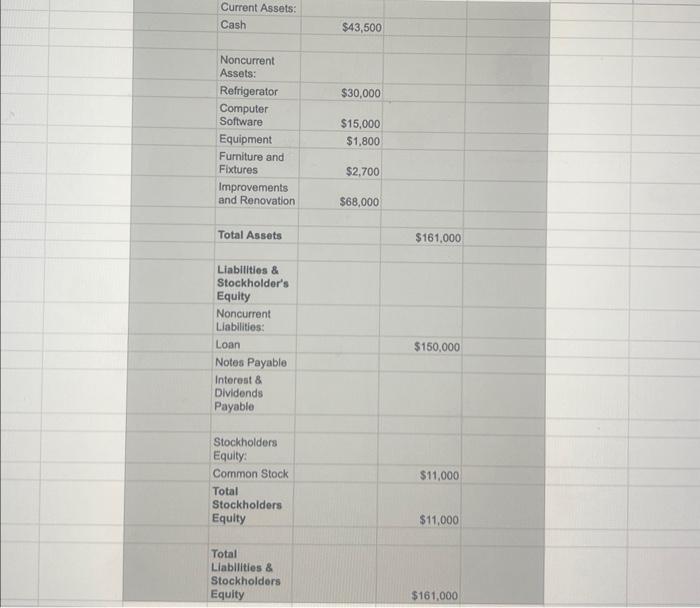

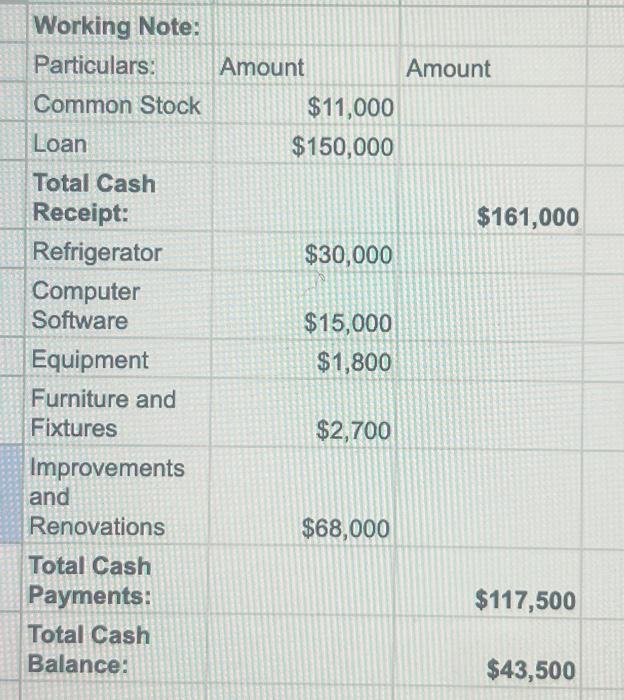

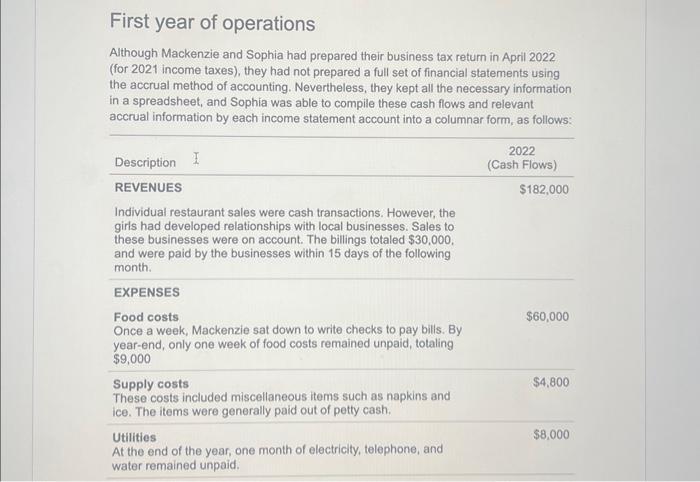

First year of operations Although Mackenzie and Sophia had prepared their business tax return in April 2022 (for 2021 income taxes), they had not prepared a full set of financial statements using the accrual method of accounting. Nevertheless, they kept all the necessary information in a spreadsheet, and Sophia was able to compile these cash flows and relevant accrual information by each income statement account into a columnar form, as follows: Employee wages These costs were kept fairly low. Mackenzie was an extraordinary baker and Sophia was an excellent chef. For the simpler work, they only hire college students. At the end of the year, one week of wages ($1,400) remained due. Licenses The "new business license" fee was paid early morning on April 1. 2022. This payment allowed the restaurant to begin operations immediately. \begin{tabular}{llr} Insurance & $18,000 \\ \hline \end{tabular} A comprehensive insurance policy was purchased on April 1 , 2022. The policy covered loss due to theft, fire, or storm damage. The policy also covered business-related risks such as lawsuits arising from customer injury while on the restaurant premises. This policy covers three years. Income taxes I The girls agreed to assume that income taxes would be paid on April 15 , at a rate of 15%. Owner compensation The girls treated the amount they withdrew for personal use as dividends. Depreciation Depreciation expense for all assets placed in service begins with the first full month of operation (e.g. nine months for those assets placed in service during 2022) Current Assets: \begin{tabular}{|l|r|} \hline Cash & $43,500 \\ \hline NoncurrentAssets: \\ \hline Refrigerator & $30,000 \\ \hline ComputerSoftware & $15,000 \\ \hline Equipment & $1,800 \\ \hline Furniture and & $2,700 \\ \hline Fixtures \end{tabular} \begin{tabular}{|l|l|} \hline Total Assets & $161,000 \\ \hline \end{tabular} Liabilitios \& Stockholder's Equity Noncurrent Liabilities: \begin{tabular}{|l|r|} \hline Loan & $150,000 \\ \hline Notes Payable & \\ \hline \end{tabular} Interest 8 Dividends Payable Stockholders Equity: Common Stock $11,000 Total Stockholders Equity $11,000 Total Llablities \& Stockholders Equity $161,000 Working Note: First year of operations Although Mackenzie and Sophia had prepared their business tax return in April 2022 (for 2021 income taxes), they had not prepared a full set of financial statements using the accrual method of accounting. Nevertheless, they kept all the necessary information in a spreadsheet, and Sophia was able to compile these cash flows and relevant accrual information by each income statement account into a columnar form, as follows: Employee wages These costs were kept fairly low. Mackenzie was an extraordinary baker and Sophia was an excellent chef. For the simpler work, they only hire college students. At the end of the year, one week of wages ($1,400) remained due. Licenses The "new business license" fee was paid early morning on April 1. 2022. This payment allowed the restaurant to begin operations immediately. \begin{tabular}{llr} Insurance & $18,000 \\ \hline \end{tabular} A comprehensive insurance policy was purchased on April 1 , 2022. The policy covered loss due to theft, fire, or storm damage. The policy also covered business-related risks such as lawsuits arising from customer injury while on the restaurant premises. This policy covers three years. Income taxes I The girls agreed to assume that income taxes would be paid on April 15 , at a rate of 15%. Owner compensation The girls treated the amount they withdrew for personal use as dividends. Depreciation Depreciation expense for all assets placed in service begins with the first full month of operation (e.g. nine months for those assets placed in service during 2022) Current Assets: \begin{tabular}{|l|r|} \hline Cash & $43,500 \\ \hline NoncurrentAssets: \\ \hline Refrigerator & $30,000 \\ \hline ComputerSoftware & $15,000 \\ \hline Equipment & $1,800 \\ \hline Furniture and & $2,700 \\ \hline Fixtures \end{tabular} \begin{tabular}{|l|l|} \hline Total Assets & $161,000 \\ \hline \end{tabular} Liabilitios \& Stockholder's Equity Noncurrent Liabilities: \begin{tabular}{|l|r|} \hline Loan & $150,000 \\ \hline Notes Payable & \\ \hline \end{tabular} Interest 8 Dividends Payable Stockholders Equity: Common Stock $11,000 Total Stockholders Equity $11,000 Total Llablities \& Stockholders Equity $161,000 Working